Apple’s Big September Moment Is Almost Here — What’s Priced In?

TradingKey - Apple (AAPL) has staged a strong rebound lately, with shares up 14% in August as investors breathed a sigh of relief over easing tariff risks. But whether the rally can keep going may depend on one thing: this week’s product launch.

New iPhones Are Coming

Apple is set to host its “Awe Dropping” fall event on September 9. As usual, the headline act is expected to be the iPhone — in this case, the new iPhone 17 lineup.

If reports are accurate, this year’s model will be thinner than ever and ship alongside iOS 26, which is rumored to bring Apple’s most significant design revamp since iOS 7 ditched skeuomorphism a decade ago. That visual overhaul could be the main catalyst behind a new upgrade cycle — not hardware specs, but aesthetics.

Source: Vilmate

Apple may also roll out a full refresh of its Apple Watch lineup, including the Series 11, Ultra 3, and SE 3 — marking the first time all models are updated simultaneously. Ultra 3 will reportedly feature a bigger display and improved charging speeds. In addition, products like the AirPods Pro 3, a new HomePod mini, and an upgraded Apple TV 4K could make appearances.

China Demand and Tariff Worries

China has long been one of Apple’s most critical growth markets, but iPhone sales there have struggled in recent quarters — hurt by soft consumer demand and a lack of headline-grabbing innovation. But signs of stabilization are starting to emerge.

In Q2, Apple leaned into heavier discounts to reignite demand. Beyond its typical mid-year shopping festival promotions, the 2025 iPhone 16 Pro (128GB) saw an extra ¥100 price cut and came in under the ¥6,000 (~$840) threshold to qualify for China’s 15% government subsidy — aimed at boosting domestic tech spending. CEO Tim Cook noted on the earnings call that the program had a “clear positive impact” on sales in the region.

Globally, Apple held on to its No. 2 spot in smartphone shipments in Q2 2025, according to Counterpoint Research, posting a 4% year-over-year growth while the overall market edged up 2%. The U.S. saw a pull-forward in demand from consumers worried about future tariffs, while India and Japan posted solid volumes.

Those tariff concerns have also eased. Apple’s long-running commitment to invest an additional $100 billion in U.S.-based iPhone component manufacturing — seen as a goodwill gesture toward Washington — appears to have shielded it from some political fallout. And while the Trump administration recently announced a 25% tariff hike on Indian imports, smartphones were excluded, calming investor fears about rising input costs.

iPhone Pricing Could Make or Break the Momentum

A lot now hinges on how Apple prices the new phones. After months of soft performance, investors are watching closely to see whether the upcoming iPhone can both excite the market and deliver unit growth.

J.P. Morgan’s Samik Chatterjee expects the new iPhone Air to land in the $899–$949 range. But pricing closer to the low $800s could unlock demand — especially in China, where it would remain eligible for government subsidies. That could give Apple stronger footing in the premium mid-tier segment, where competition is intensifying.

AI: Still a No-Show

For all the attention on hardware, many investors are also wondering: what happened to Apple’s AI ambitions?

So far, the company has failed to deliver on the “Apple Intelligence” promises it made at WWDC 2024. Back then, software head Craig Federighi touted a future where iPhones would offer smarter, deeply integrated personal AI. “Not this year,” it turns out.

When Apple Intelligence debuted in October 2024, it came with modest upgrades: Siri dictation for texts, notification summaries, and a writing assistant. While useful, the rollout underwhelmed — and since then, strategic clarity has only gotten murkier.

Leadership changes haven’t helped. Siri chief John Giannandrea was reassigned to lead Vision Pro, and Apple has not named a clear AI successor. Bloomberg previously reported internal disagreements over how hard to push into AI, with Federighi seen as reluctant to divert resources from core platforms. Giannandrea had pushed for more AI investment early on but was frequently blocked.

The competitive gap is widening. Microsoft’s Copilot is now baked into Windows 11 and enterprise workflows. Google’s Gemini is live on Pixel and Android. Apple, by comparison, has said its full AI-powered Siri redesign won’t arrive until 2026 — effectively putting it 12–24 months behind rivals in one of tech’s fastest-moving arenas.

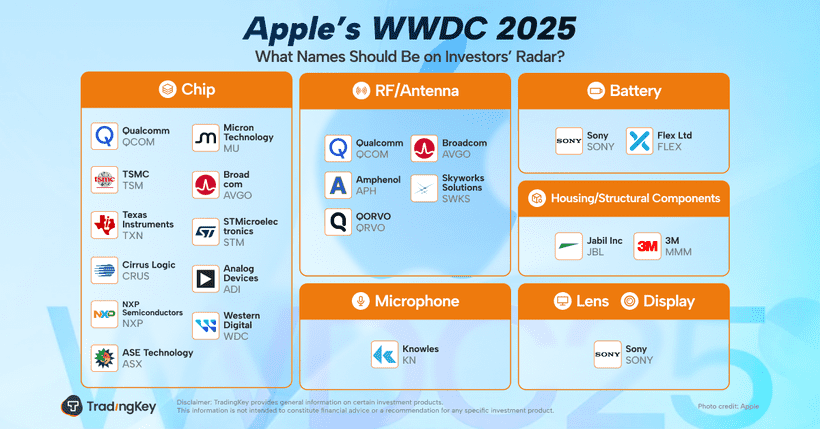

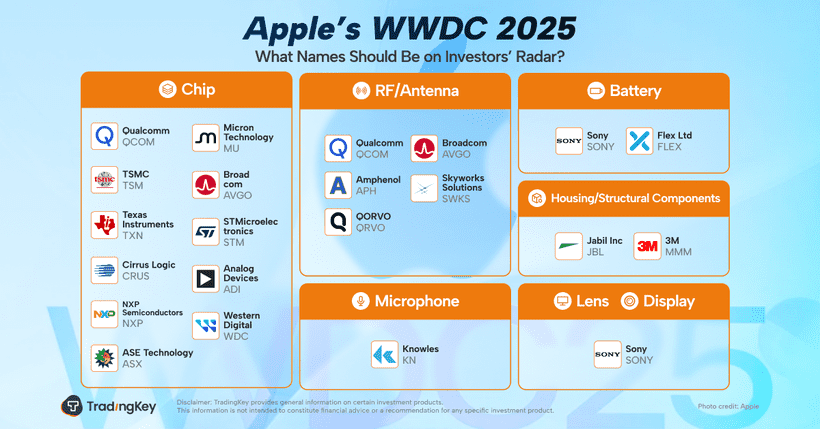

The Apple Trade: What to Watch in the Supply Chain

Every Apple event tends to ripple across its global supply chain. “Buy the rumor” bets often lead to near-term pops in component makers. If the iPhone 17 prices aggressively — or Apple drops a surprise on the AI front — related names could catch a bid.

Here are some of the likely beneficiaries across hardware categories:

Semiconductors: Qualcomm (QCOM), Micron (MU), TSMC (TSM), Broadcom (AVGO), Texas Instruments (TXN), STMicro (STM), Cirrus Logic (CRUS), Analog Devices (ADI), NXP (NXPI), Western Digital (WDC), ASE Technology (ASX)

RF / Antennas: Qualcomm (QCOM), Broadcom (AVGO), Amphenol (APH), Skyworks (SWKS), Qorvo (QRVO)

Battery Components: Sony (SONY), Flex (FLEX)

Audio / Microphones: Knowles (KN)

Camera / Imaging: Sony (SONY)

Structural / Casings: 3M (MMM), Jabil (JBL)

Displays: Sony (SONY)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.