Apple’s Seasonal Q4 Rally Kicks In — Will iPhone 17 Break the Upgrade Cycle and Add More Fuel?

TradingKey - Historical data over the past decade shows a clear seasonal trend in Apple’s stock price: consistent gains in Q3 and Q4. While not guaranteed, unexpectedly strong demand for the iPhone 17 series is now reinforcing confidence in Apple’s solid performance, sharply reversing earlier investor concerns about weak iPhone demand.

For this global innovation leader, 2025 has been a year of “weak start, strong recovery.” By late October, Apple’s stock has fully recovered its year-to-date losses and posted a modest gain — erasing the gloom that clouded its outlook earlier in the year.

Early 2025 brought challenges: concerns over sluggish iPhone demand, slow AI progress and monetization, U.S. tariffs, and an antitrust case linked to Google led rare downgrades from firms like MoffettNathanson, Loop Capital, and Jefferies.

However, as Trump tariff impacts eased and Apple ramped up external AI partnerships, the stock accelerated its rebound in the second half. Historically, Apple shares tend to rise in the latter part of the year — and the iPhone 17 series, breaking traditional upgrade cycles, adds fresh momentum.

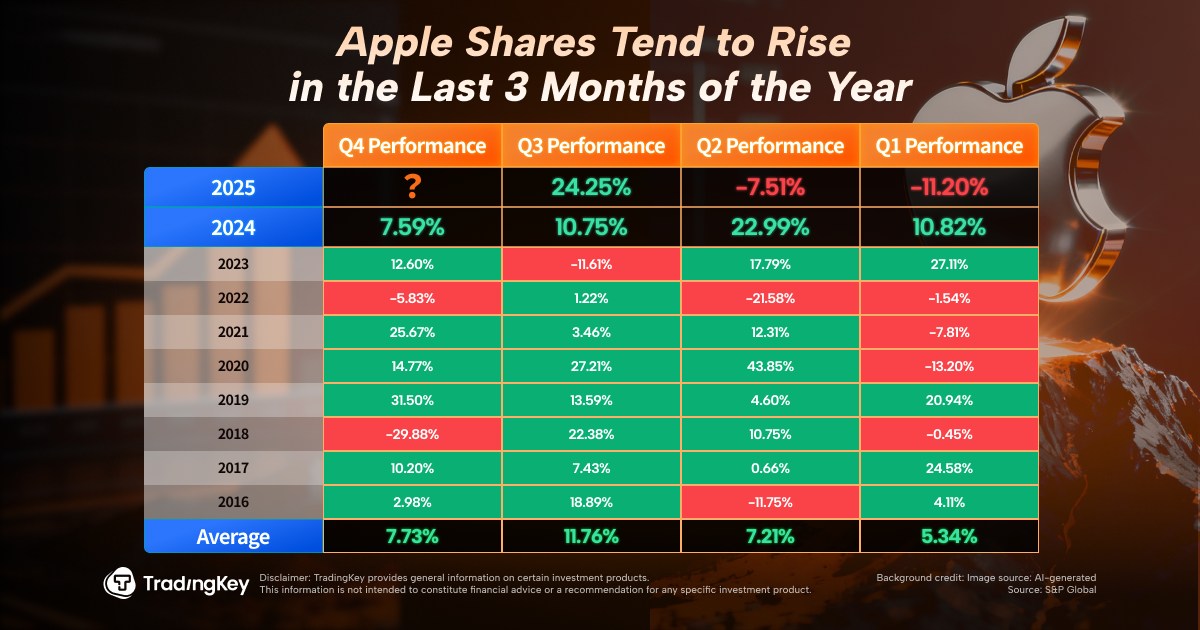

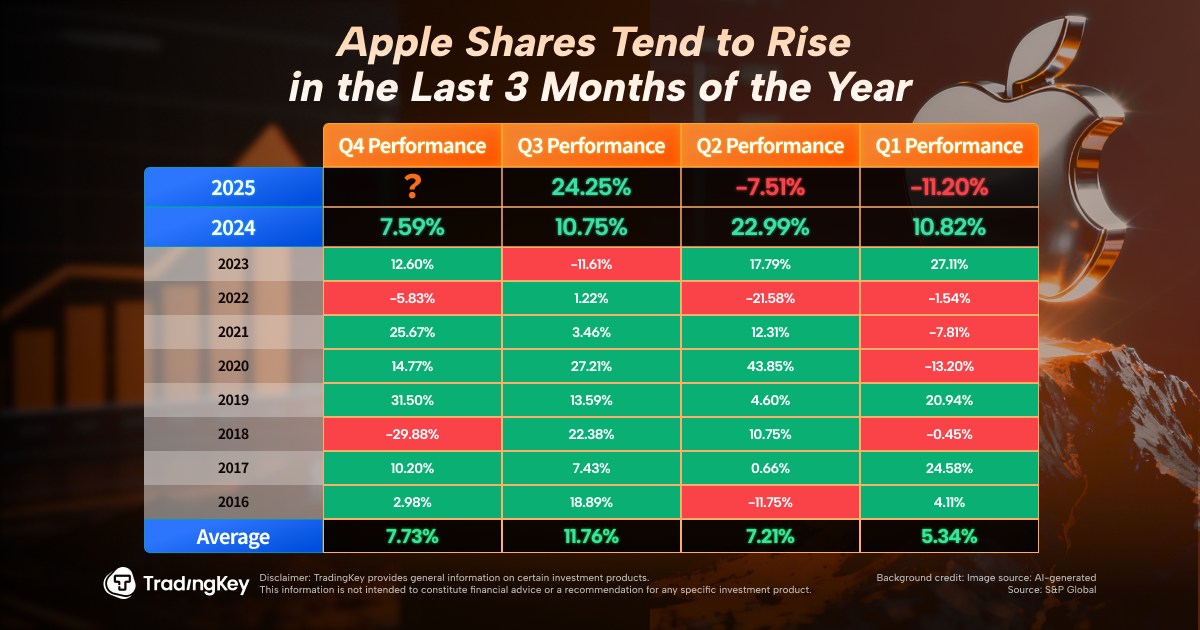

Seasonal Strength: A Decade of Q3 and Q4 Gains

According to TradingKey’s compiled data, Apple’s stock has consistently followed a seasonal pattern from 2016 to 2025: "weakest in Q1, second weakest in Q2, strongest in Q3, and second strongest in Q4" in terms of both the probability and magnitude of gains.

After a stellar +24% gain in Q3 2025, Apple remains well-positioned for further upside based on historical trends.

iPhone Demand Improves — iPhone 17 Sparks a “Super Cycle”?

The iPhone, accounting for about 47% of Apple’s revenue, has shown surprising strength recently. In Q2, iPhone sales rose 13.5% YoY to $44.58 billion, surpassing the consensus estimate of $40.06 billion and ranking second among Apple’s five major revenue streams — behind only Mac computers.

The launch of the iPhone 17 series has become a new growth catalyst. According to Counterpoint Research, sales of the phone — described as Apple’s most significant upgrade in years — were 14% higher in the first 10 days after launch in two key markets, China and the U.S., compared to the previous-generation iPhone 16 series.

With extended delivery timelines, higher production targets, and positive feedback from carrier channels, Goldman Sachs analysts expect iPhone 17 demand to exceed that of the iPhone 16.

They posed the question: Are we entering an iPhone super cycle?

Evercore analysts also noted recent signals suggesting the new model may break the average iPhone upgrade cycle — with base-model iPhone 17 delivery times already exceeding levels seen in October last year.

While the Air model’s positioning remains debated, its popularity in China is undeniable. Looking ahead, the expected launch of a foldable iPhone next year, along with a rumored fully glass curved-screen device to mark the 20th anniversary of the iPhone, could sustain Apple’s product momentum.

Earnings Report to Show Its Mettle

Apple will report its fiscal Q4 2025 results on October 30. Although the quarter includes only partial iPhone 17 sales, any positive guidance or data will likely boost market sentiment.

Per Seeking Alpha, analyst consensus forecasts:

- Revenue: Rising from $94.93B to $102.09B — Apple’s first return to the $100B+ club in 2025

- EPS: Jumping from $0.97 to $1.77

An Evercore ISI survey found that the proportion of respondents planning to buy a new iPhone this year is above historical averages. Stronger iPhone demand and clearer visibility into double-digit growth in services create a favorable backdrop ahead of earnings.

Noting Apple’s tendency to outperform in the final quarter — driven by holiday shopping expectations — Evercore maintains an “Outperform” rating on Apple, with a $290 price target, implying about 12% upside from current levels.

Is the Super Cycle Already Priced In?

Despite optimism, it’s too early to confirm a true iPhone super cycle.

Earlier this month, Jefferies downgraded Apple, warning that the recent rally was fueled by better-than-expected demand for the latest iPhone and excitement around foldable devices — but these factors may already be fully priced into the stock.

This could leave the market overly optimistic about the iPhone 18 foldable and future upgrade cycles, setting up potential disappointment if expectations aren’t met.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.