Intel Q3 2025: AI Boost and Partnerships Signal a New Era for US Chip Leadership

TradingKey - Intel’s Q3 FY2025 earnings smashed Wall Street projections, sending the stock up 8% in after-hours trading and fueling renewed confidence in the company’s turnaround story. Powered by robust gains in AI and data center segments, Intel outperformed consensus on every major metric—delivering a clear message that its strategic reset is gaining traction.

While management spoke enthusiastically about surging AI demand and deepening partnerships with industry giants, they also struck a note of caution: Q4 guidance remains conservative and operational challenges, from supply chain strain to margin headwinds, have not disappeared. The mix of headline beats and prudent outlook makes Intel one of the most closely watched tech stories this quarter.

Q3 Financial Performance vs. Expectations

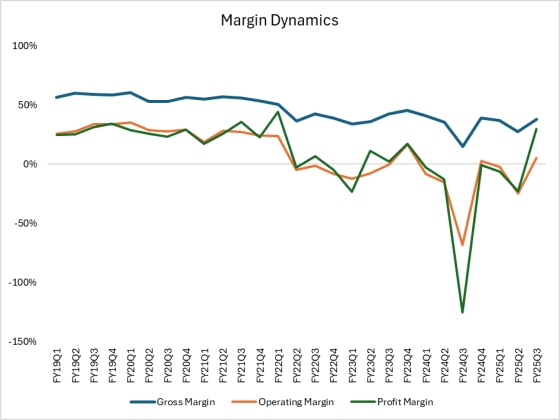

Intel delivered a strong set of quarterly results in Q3 FY2025, outpacing expectations and showing clear improvements on a year-over-year basis. The company reported revenue of $13.7 billion, exceeding consensus and last year’s results. Non-GAAP gross margin improved to 40%, a notable increase from both consensus and 2024 levels, while EPS came in at $0.23, a significant turnaround from a loss the previous year and far above analyst estimates.

Metric | Q3 2025 | Consensus | Q3 2024 | YoY Change | Q4 2025 Guidance |

Revenue | $13.7B | $13.2B | $13.3B | +3% | $12.8-13.8B |

Non-GAAP Gross Margin | 40.0% | 36.1% | 18% | +22 pts | 36.5% |

Non-GAAP EPS | $0.23 | $0.01 | ($0.46) | N/M | $0.08 |

Source: Intel, TradingKey

These results reflect robust operational execution. The margin outperformance was driven mainly by a more favorable product mix, reduced inventory reserves, and rigorous cost control.

Source: Intel, TradingKey

While expenses increased due to the ramping of new products like Lunar Lake and 18A, Intel maintained strong overall profitability, underpinned by solid client and data center demand. Capital expenditures reached $3 billion, and adjusted free cash flow was positive at $900 million, reinforcing Intel’s financial flexibility.

Debt management featured prominently in Intel’s financial strategy this quarter. The company repaid $4.3 billion in debt, an action management highlighted as central to its ongoing deleveraging program. Management reiterated its intent to prioritize repayment of all maturing debt through 2026, supported by strong operational cash flows and nearly $31 billion in cash and short-term investments. This program of aggressive debt reduction, alongside fresh inflows from strategic partners and asset monetizations, supports both Intel’s substantial upcoming CapEx commitments and its aim to lower overall financing costs and risk.

Against this backdrop, Intel’s fourth quarter guidance is more conservative, with projected revenue between $12.8–13.8 billion and EPS of $0.08, both just below consensus.

Segments Performance

Client Computing Group (CCG) revenue grew 8% sequentially, driven by seasonal demand, ongoing migration to Windows 11, and a positive product mix from launches such as Lunar Lake and Arrow Lake. Intel’s deepened ecosystem partnership with Microsoft further strengthened its position in business PCs.

Data Center & AI (DCAI) revenue increased 5% sequentially, supported by AI server demand and a continued shift toward higher-value products. Xeon 6 (Granite Rapids) showed competitive total cost of ownership and efficiency improvements, meeting the demands of expanding hyperscale AI infrastructure.

-3b52cd74c5b544f6b3f2c018a835087c.jpg)

Source: Intel

Intel Foundry’s revenue was $4.2 billion, slightly down. However, operational losses narrowed, attributable to reduced impairment charges and a gradual pivot to advanced product technologies.

-c6348772d79045ee8052b0dae6a18962.jpg)

Source: Intel

And Altera’s removal from consolidated results will create resistance to margin improvement in 2026, as its contribution was accretive to gross margin.

Balance sheet

Inventory remains high, though it declined modestly during the third quarter. This allows Intel to meet near-term demand spikes but signals ongoing capacity constraints in older nodes.

The company remains disciplined with capex decisions, scaling Foundry investments only with confirmed external demand. The planned $18–27 billion capital investment for next year signals flexibility but also adds risk if wafer or packaging demand softens.

Intel’s strong operating performance and prudent balance sheet management have created a foundation for continued investment in future growth markets, while leaving the company well positioned to weather sector headwinds and shifts in global semiconductor demand.

3 Life-Changing Strategic Partnerships

Intel’s liquidity position and financial flexibility in Q3 FY2025 are underpinned by three pivotal strategic partnerships, each significantly strengthening its balance sheet and supporting future investment. These deals have collectively delivered both immediate capital inflows and longer-term confidence in Intel’s central strategic role for the US technology supply chain.

1. US Government Partnership

Intel received an accelerated $5.7 billion infusion from the US Government in Q3. US government owns approximately 10% of Intel’s shares now. This support highlights Intel’s unique position as the only major US-based advanced wafer manufacturer, making it indispensable for national security and future domestic semiconductor capacity. The government’s investment is part of a broader policy initiative: ensuring a resilient and geographically diversified chip supply chain that cannot rely solely on TSMC or foreign-owned fabs. It also gives Intel powerful political backing to attract subsequent corporate or institutional investors. This sovereign anchor investment not only improves liquidity, but also provides confidence to the market and prospective partners. By underwriting Intel’s scale-up, Washington is sending a clear message that domestic chip leadership is a must-do strategic priority before the current administration leaves office.

However, this doesn’t come without a cost. This hands-on government involvement can also create political constraints. Intel may be required to prioritize national security objectives over pure market logic or commercial agility.

2. SoftBank Strategic Investment

SoftBank contributed $2 billion during the quarter, joining as a key partner in Intel’s plans to expand global AI infrastructure—particularly through Foundry and advanced packaging initiatives. This partnership is not a pure financial investment, but also reflects SoftBank’s interest in securing capacity for its portfolio companies and to influence the direction of next-generation node and packaging technologies in the US and globally.SoftBank’s investment broadens Intel’s access to international capital and adds commercial leverage. By bringing in SoftBank, Intel earns validation from one of the world’s largest technology investors, positioning the company not merely as a supplier, but as an innovation hub for AI and compute infrastructure.

3. Nvidia Collaboration

Nvidia’s $5 billion investment, expected to close by the end of Q4, marks a high-profile endorsement of Intel’s future direction, but its near-term impact is limited.

The partnership covers joint development of x86 CPUs for NVLink systems and SoCs integrating Nvidia GPU chiplets with Intel CPUs. Importantly, Nvidia confirmed that initial products from this collaboration will not be fabricated at Intel foundries—they will rely on TSMC instead.

Moreover, Nvidia indicated that no meaningful commercial products are expected before 2027, with the timeline possibly extending further. While this alliance strengthens Intel’s AI ecosystem positioning and opens the door to future foundry opportunities, the tangible business and financial benefits are several years away and contingent on successful execution and technological parity.

These three transactions directly boosted Intel’s cash and short-term investments to $31 billion by quarter end. This unique combination of government, institutional, and flagship commercial partnerships creates a “too big to fail” narrative around Intel, securing its role at the center of US and global chip supply chain policy and investment. The partnerships are mutually reinforcing: government backing draws in private capital, while SoftBank and Nvidia provide commercial validation and future strategic optionality.

Intel’s ability to convert these capital inflows into winning technology advances, improved foundry economics, and scalable AI platform leadership will determine how durable this strategic advantage proves in the years to come.

Capturing Strong AI demand

Management commentary suggests AI is now driving fundamentally new demand for compute architectures, with x86 at the core of cloud, edge, and agentic workloads. The rise of AI inference, especially in the enterprise sector, is presented as both a near-term growth driver and a long-term market foundation for Intel’s product and platform strategy. Its x86’s massive installed base makes it the default foundation for enterprises upgrading to AI-powered systems, especially for hybrid environments that blend traditional and AI-intensive operations.

As AI inference becomes central to enterprise and cloud deployments, Intel sees near-term growth opportunities, not just from high-value server upgrades, but also from the proliferation of AI PCs, which are expected to ship nearly 100 million units this year. The flexibility of x86 allows it to support a diverse set of AI workloads, from large-model inference in data centers to low-latency tasks at the edge, helping customers transition seamlessly between architectures and use cases.

Intel’s adaptability is further enhanced by collaborations, notably with Nvidia, to develop new generations of x86 CPUs integrated with advanced GPU capabilities. This allows Intel to target both mainstream computing and cutting-edge AI acceleration. However, despite the strategic promise, structural challenges persist: supply constraints in older process nodes and ongoing inventory reliance have limited Intel’s ability to capture all available demand, especially in fast-growing server and client segments.

Ultimately, Intel’s strategy hinges on leveraging its core x86 strengths—compatibility, security, and scale—while innovating through partnerships and technical advances to fully unlock AI-led growth across markets.

Foundry and Product Roadmap

Progress continues on next-generation process nodes. Panther Lake launches are on track, with Fab 52 in Arizona now fully operational for 18A manufacturing.

However, Foundry remains margin-challenged near term. Gross margin improvement is expected as higher-end nodes capture scale, yet negative margins in early phases show significant startup costs and product mix dilution. Management is candid that 18A yields, while sufficient for supply, are not yet at levels required for optimal profitability; these are not expected to reach industry-acceptable standards until at least the end of next year. 14A appears to be progressing faster, both in yield and performance.

Customer commitment is cited as a precondition for new Foundry capacity investment, a prudent step to avoid excess capex, but one that could lengthen the path to competitive scale.

Intel’s advanced packaging technologies, such as EMIB and Foveros, are becoming an important source of incremental revenue. Growing demand for complex chip integration—driven by chiplets, AI workloads, and heterogeneous computing—is prompting more customers, including cloud providers and competitors, to seek US-based packaging solutions. By differentiating from traditional wafer-only foundries, Intel is well positioned to capture this expanding market.

At the same time, the newly formed Central Engineering Group is streamlining engineering and IP development, helping Intel align manufacturing efforts more effectively with customer needs and supporting a scalable future for its foundry ambitions.

Conclusions

Intel’s Q3 FY2025 performance demonstrates real improvement and a more resilient balance sheet, while positioning the company for a pivotal role in next-generation AI infrastructure. Strategic partnerships and sovereign backing provide financial stability but do not guarantee competitive success. The outlook for 2026–2027 is cautiously optimistic: Intel retains leadership in x86 for AI-first and inference-centric computing, enjoys strong government and institutional support, and has potential for significant margin expansion if Foundry advances materialize.

Valuation remains reasonable, with a forward PE of 15 reflecting cautious optimism around future profitability. Investors should expect near-term margin pressures and carefully watch for evidence of execution—particularly around advanced node yields, packaging revenue growth, and the pace of collaborative product launches. If Intel continues to execute on ramping manufacturing technology and captures incremental value in advanced packaging, it can justify its leadership and potentially deliver disproportionate upside as the multi-year AI cycle plays out. For long-term holders, patience and vigilance are warranted; Intel’s ambition is high, but so are the stakes.

Risks

Intel continues to face substantial challenges that could weigh on its growth trajectory and market positioning.

Competitive pressures from established foundry players like TSMC and Samsung remain intense, especially in advanced logic and packaging.

Persistent supply chain tightness and substrate shortages impact Intel’s ability to fully meet demand, particularly for older process nodes.

Macroeconomic volatility could affect global semiconductor demand and disrupt capital flows or investment plans. The company’s heavy foundry and capex commitments require extraordinary discipline, ensuring that capacity expansions are tightly aligned with customer commitments and profitable yield improvements.

Finally, innovation risk is material; Intel must continually advance its AI hardware and software platforms to maintain relevance and differentiation as AI and heterogenous workloads redefine industry standards.

-d50fb618d28d499fa3b1efa38c699e4f.jpg)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.