Alibaba’s Friday Earnings to Crown China Tech’s Q2 Winner

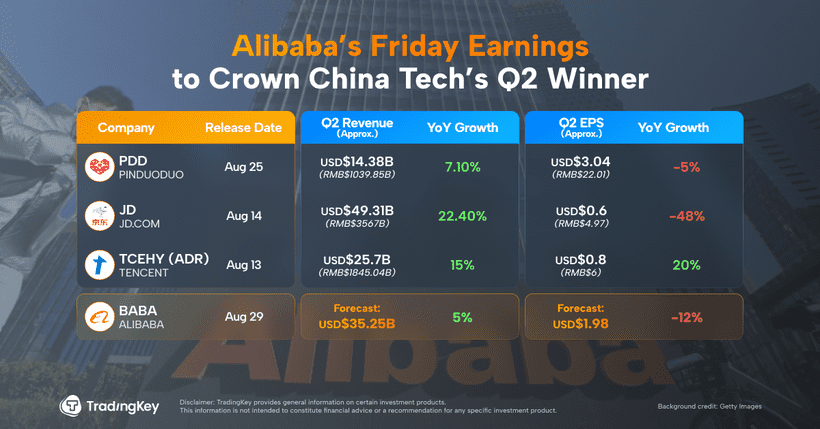

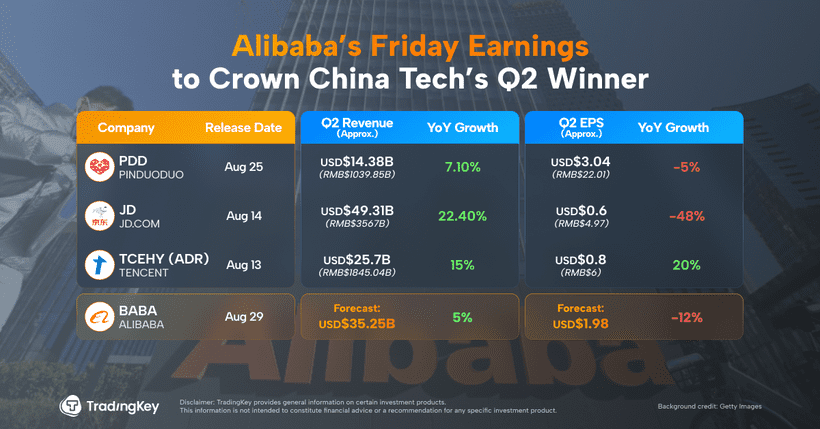

TradingKey - Names like JD.com, Pinduoduo, Tencent, and Alibaba represent the top-tier of Chinese tech stocks trading in the U.S. But their FY2025 Q2 earnings paint very different pictures.

Tencent delivered the most stable performance this quarter. Revenue from advertising and gaming continued to grow at a healthy pace with high profitability. Total Q2 revenue reached RMB 184.5 billion, up 15% year-over-year. Net income and EPS both climbed 20% year-over-year.

JD.com pulled in RMB 356.7 billion in revenue, up 22.4% YoY, but profits took a hit. The company’s aggressive investment in its food delivery business weighed heavily on bottom-line numbers. Net income dropped nearly 48% YoY, and EPS took a significant dive. While the food delivery push did help drive user activity and top line growth, it also applied serious short-term pressure on profit margins.

Pinduoduo (PDD) reported Q2 revenue of RMB 103.99 billion, a 7.1% increase YoY, but EPS fell 5%. On the earnings call, management reiterated that future growth could be unpredictable. That has investors watching closely, wondering how PDD will sustain meaningful progress in such a competitive environment.

Alibaba will report earnings on August 29. According to Bloomberg’s consensus estimates, Alibaba’s FY2026 Q1 revenue is expected to hit RMB 253.4 billion, a 4.2% YoY increase. Adjusted EPS, however, is forecast to dip 3.8% YoY to RMB 15.8, while profit margin is expected to slide to 15%.

The drop in profitability is widely attributed to Alibaba’s heavy spending on its “Flash Sale” business. Since announcing its RMB 50 billion subsidy initiative on July 2, daily orders from Taobao Flash Sale events have skyrocketed from 10 million to 80 million. But while the growth is impressive, this aggressive expansion strategy has come at the expense of sharply deteriorating margins in the Local Services division.

On the flip side, Alibaba Cloud is showing strong momentum. Analysts generally expect Q1 revenue from Alibaba’s Cloud Intelligence Group to hit RMB 32.5 billion, up 22% YoY. AI-related product revenue has now posted triple-digit growth for seven quarters in a row—and that’s turning this division into a key potential profit center for the group.

The recent earnings cycle suggests China's largest stocks are still facing serious headwinds.

AI is no longer a 'future story,' but real returns are still a work in progress

Advertising continues to be the biggest engine powering Tencent’s growth—it has now posted double-digit revenue increases for 11 straight quarters. AI-powered upgrades to Tencent’s ad tech and improved commerce capabilities within the WeChat ecosystem are fueling demand across video feeds, Mini Programs, and in-app search. That said, the company’s rising spending on AI infrastructure is starting to challenge near-term profitability. In Q2 2025 alone, Tencent racked up RMB 19.1 billion in capital expenditures, a 119% jump YoY.

On the company’s earnings call, management addressed those concerns about rising costs, pointing out that Tencent needs to “spend smart,” not just throw money at the latest AI trend—whether that means chip buys, hiring waves, or marketing spend.

For Alibaba Cloud, the growth narrative has come back to life. Over the past year, its revenue growth rate accelerated from just 3% to 18%. For FY2025, the segment generated RMB 118 billion in revenue, up 11% YoY. Investors credit the turnaround in large part to booming interest and enterprise investment in AI.

Alibaba plans to put more than RMB 380 billion over the next three years into building up its cloud and AI infrastructure. According to CEO Eddie Wu, the capital deployment will be balanced across periods, with FY2025 alone expected to see over RMB 120 billion in spending. The company is targeting three key focus areas: core infrastructure for cloud and AI, large foundational models, and AI-native applications—including embedded upgrades across core business units.

Both Tencent and Alibaba are making it clear: AI investment isn’t slowing anytime soon. And, based on recent earnings trends, AI is already showing up as a tangible revenue driver. Still, in terms of translating those gains into lasting profits, we’re still early in the marathon.

A slowing macro backdrop is dragging on consumer demand

The good news: with state-backed stimulus still supporting consumption, core marketplace results remain fairly solid. JD’s core retail business generated revenue of RMB 310.1 billion, up 20.6% YoY. Alibaba’s core commerce unit is also expected to maintain low single-digit sales growth.

How long that growth momentum can last, though, depends on the strength and duration of national subsidy policies. With a new round of subsidies issued in early August—and the government openly prioritizing consumption—analysts expect the support to hold up, at least in the short term.

But beyond subsidies, the broader reality is that China’s economy is still in a transitional phase. Consumer spending may have some resiliency, but confidence is still fragile. Structural pressure persists, and there's little sign of significant recovery in willingness to spend.

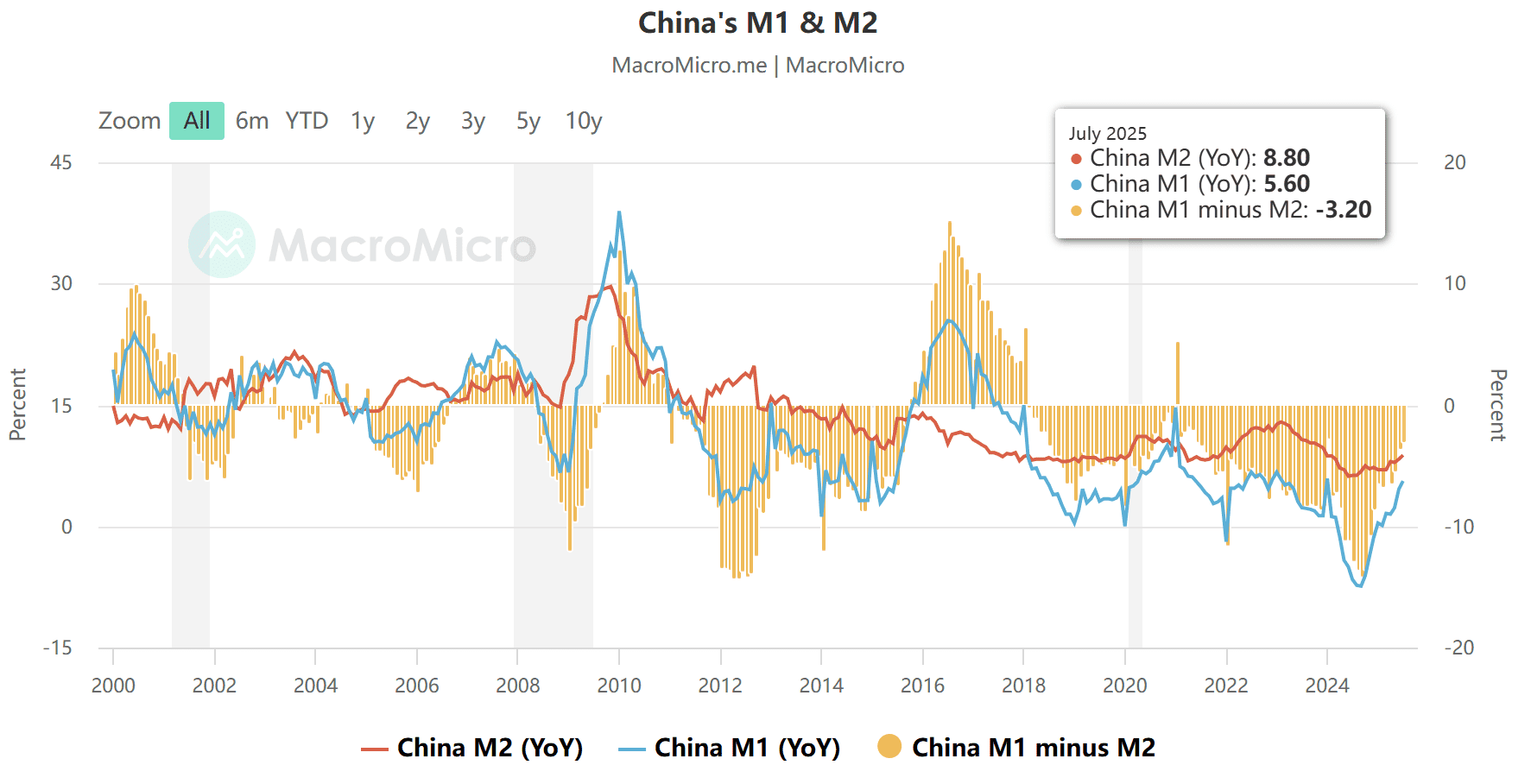

At the end of July, China’s M2–M1 gap sat at 3.2 percentage points, 0.5 percentage points narrower than the previous month but still solidly positive. In other words, a lot of money is stuck in long-term deposits, not circulating through the economy. For H1 2025, M2 money supply grew an estimated 10% YoY.

According to reporting from Reuters, new RMB loan issuance in July contracted by RMB 50 billion (approximately USD 6.97 billion). That figure missed forecasts by a wide margin and marked the first July contraction since 2005—and the largest month-over-month drop since 1999.

This suggests underlying private sector demand remains weak. Companies aren’t feeling pressure to expand or hire, and wage growth has slowed. With households facing an uncertain income outlook, sentiment around broader economic conditions has turned cautious. That makes it hard to materially boost either consumer credit or spending. Soft credit data is yet another sign that demand-side momentum remains flat and economic energy hasn’t broken out.

Fierce competition is putting the squeeze on profits

E-commerce in China has entered a new phase—fighting for share in a low-growth environment. And the new battle is being played across both legacy and emerging fronts. Platforms are shifting away from pure price wars to more refined strategies—focus on ecosystem, operational efficiency, and differentiated value creation. Taobao and Tmall remain in the lead, largely due to their entrenched position and AI capabilities. Pinduoduo, meanwhile, is still growing fast by playing to its strength in lower-tier cities and continuing its aggressive subsidy model.

But a major wave of competition is now taking shape around instant retail and on-demand delivery. That means even more money is being funneled into new subsidy programs—now not just for traditional e-commerce but for local services too.

Food delivery is not a quick-win business. It takes long-term capital and logistical execution to move the needle. If national subsidies fade, many players may find themselves overextended. For JD.com, for example—where high-margin categories like electronics anchor profitability—covering persistent losses in delivery subsidies could quickly become a concern.

That said, instant retail does more than bolster gross merchandise value—it drives platform engagement. High-frequency use cases like takeout can meaningfully boost daily activity, extend user time on app, and create a flywheel effect for lower-frequency verticals like discretionary goods and CPG. Categories such as daily essentials and supermarkets already show strong upward momentum. Still, from a more cautious point of view, adding more users means little unless retention and repeat purchase patterns hold up over time.

Worth noting: earlier this year, Tencent's WeChat (WXG division) quietly set up an internal E-commerce Product Group tasked with consolidating its shopping-related projects into Mini Programs. It’s a clear signal that Tencent is gearing up to enter the intensifying e-commerce battle.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.