Can Gold Still Glitter in a Liquidity Trap?

AI Podcast

Last week's "sell-everything" event saw gold, silver, and cryptocurrencies sharply decline due to a liquidity squeeze, forcing institutions into cash. This was a technical breakdown driven by deleveraging, not a fundamental shift. Record $26 billion in global gold ETF inflows in January 2026, led by Asia, indicates strategic capital positioning into weakness. Asian inflows reflect reallocation hedges amidst volatile domestic markets, while North America and Europe use gold as credit insurance against Fed policy concerns and trade anxiety. The macro narrative has shifted to recession expectations, potentially accelerating Fed rate cuts. Long-term investors may find the dip a strategic entry point, but short-term volatility necessitates caution.

TradingKey - Global major assets went through a rare “sell‑everything” last week. After briefly touching $5,100, gold reversed sharply; silver and cryptocurrencies saw outright capitulation. Yet beneath the surface volatility, new data from the World Gold Council (WGC) reveal a strikingly different undercurrent: strategic capital is positioning into weakness at a scale not seen in decades.

The Liquidity Trap: Why Did Safe Havens Falter When Fear Peaked?

Gold’s latest correction was the textbook symptom of a liquidity squeeze. A violent sell‑off in the S&P 500’s tech complex—led by Amazon, whose AI‑driven capex shock rattled earnings expectations—rekindled concerns over a bursting tech bubble. The unwind spread quickly: leveraged liquidations across Bitcoin and silver cascaded through derivative markets, forcing institutions into a “cash‑only” stance.

In the first stage of any liquidity crunch, even safe assets become collateral. Gold’s high convertibility turns it into the first line of defense for margin calls. The simultaneous rebound in the dollar index and the drop in Treasury yields told the same story: capital wasn’t seeking assets, it was seeking cash. The drawdown in gold was never about fundamentals—it was a mispricing born of deleveraging mechanics, not a change in belief.

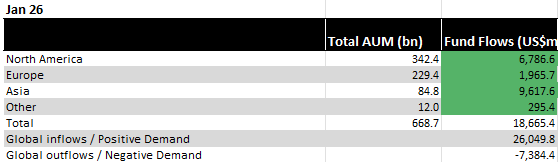

Capital Rotation: Record ETF Inflows, Shifting Price Power

Market screens looked ugly, but fund flows said otherwise. According to WGC, global gold ETFs recorded a record $26 billion net inflow in January 2026, the largest monthly intake in history.

The detail that matters: where that money came from. Asia accounted for $9.6 billion, overtaking North America for the first time. In China, with real estate and equity markets swinging wildly, gold has regained centre stage as a reallocation hedge. In India, where equities have softened, flows point to a clear rotation—out of risk, into metal.

North America and Europe tell a different story. There, gold is functioning as credit insurance. The region logged its eighth straight month of inflows, driven by rising doubts over the Federal Reserve’s political independence. As fear of policy interference grows, investors are buying gold as a hedge against systemic dollar‑credit risk. Heightened trade anxiety— rekindled by the Greenland territorial dispute—kept European flows steady.

The Macro Turn: From Inflation Trade to Recession Play

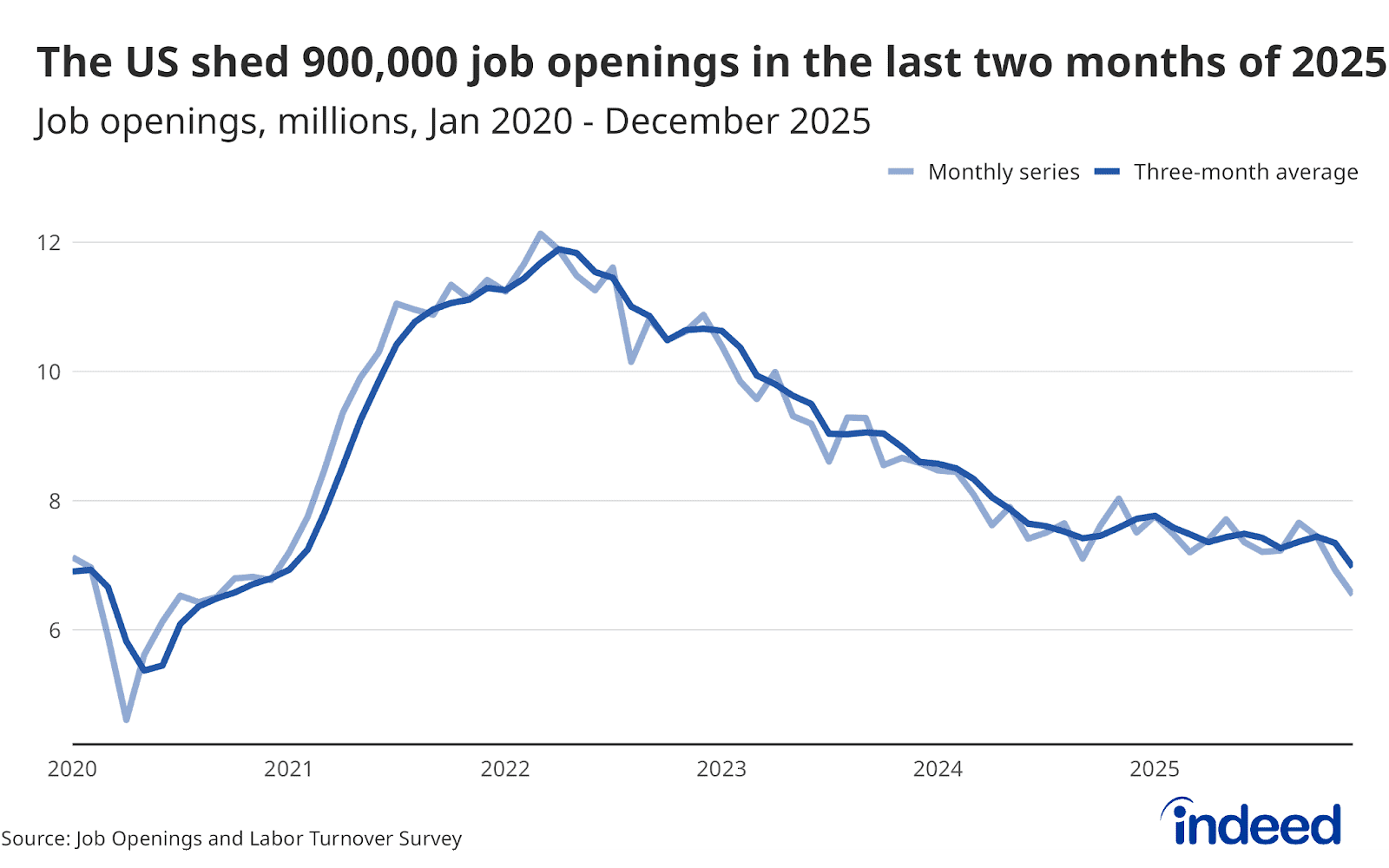

The U.S. labour market failed to improve last week: job openings hit a five‑year low, while announced layoffs surged 205 per cent. The macro narrative has shifted decisively—from fighting inflation to bracing for impact.

That pivot explains the short‑term liquidation rush, but at a cycle level it signals something deeper: the Fed may have no choice but to move faster on rate cuts. Once markets rotate from panic to pricing easing expectations, gold’s recession‑hedge status tends to reprice quickly.

Investors: Keep Cautious

Today’s gold market sits at a rare intersection—technical breakdown against structural strength. The liquidity unwind has amplified noise, but the core thesis remains intact: deepening fractures in dollar credit, persistent geopolitical tension, and sticky Asian demand all reinforce the metal’s long‑term footing.

For long‑horizon capital, the panic‑driven drop could define a strategic entry zone around $4,400–$4,500. Yet with volatility gauges like VIX spiking, short‑term trades demand humility. In markets governed by forced selling rather than fundamentals, discipline—not bravado—remains the only durable edge.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.