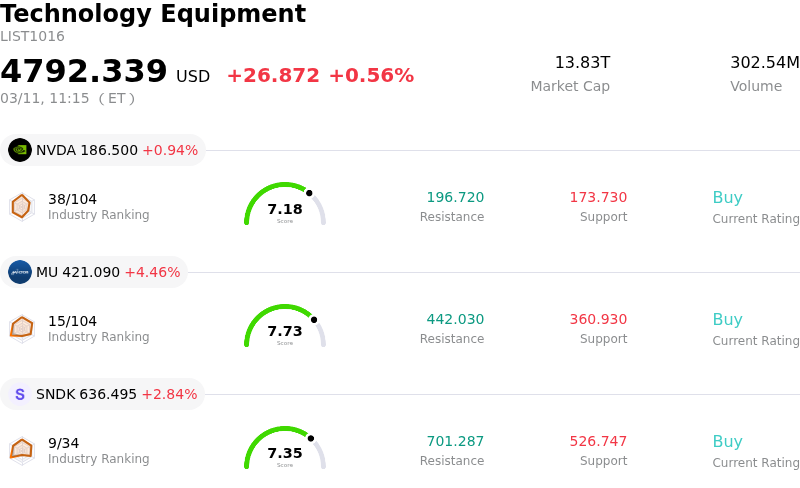

Micron Technology Inc Stock (MU) Moved Up by 4.46% on Mar 11: Key Drivers Unveiled

Micron Technology Inc (MU) moved up by 4.46%. The Technology Equipment sector is up by 0.56%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 0.94%; Micron Technology Inc (MU) up 4.46%; SanDisk Corporation (SNDK) up 2.84%.

Micron Technology (MU) experienced an upward share price movement driven by a confluence of positive analyst sentiment, robust memory pricing forecasts, and surging demand from the artificial intelligence (AI) sector.

Multiple analyst firms significantly raised their price targets for Micron. Wolfe Research, for instance, increased its target to $500 from $350, maintaining an Outperform rating. Aletheia Capital, UBS, Stifel, Susquehanna, Citi, Needham, and Morgan Stanley also delivered upgrades and boosted price targets, citing strong fundamentals in the memory market. These upgrades were largely predicated on expectations of substantial increases in DRAM and NAND pricing throughout 2026 and 2027.

The primary catalyst for the anticipated memory pricing surge is the escalating demand for high-bandwidth memory (HBM) and DDR5, critical components for AI systems and data centers. The AI boom is reallocating manufacturing capacity towards these high-margin products, leading to tightening supply in conventional memory segments. Reports indicate that NAND production lines are effectively sold out through 2026, contributing to the supply-demand imbalance. This intense demand from AI infrastructure is expected to continue absorbing a significant portion of global memory production.

Analysts have revised their revenue and earnings per share estimates for Micron upward for both calendar years 2026 and 2027, reflecting confidence in the company's financial performance amidst the strong memory cycle. Furthermore, Micron is slated to report its Q2 2026 earnings on March 18, 2026, with analysts anticipating strong results, following a beat in its Q1 2026 report. The positive outlook is also evidenced by institutional investors, with ProShares Ultra QQQ Top 30 initiating new positions in Micron, alongside other large investors increasing their holdings.

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of [8.20], indicating a neutral signal. The RSI at 52.08 suggests neutral condition and the Williams %R at -42.64 suggests oversold condition. Please monitor closely.

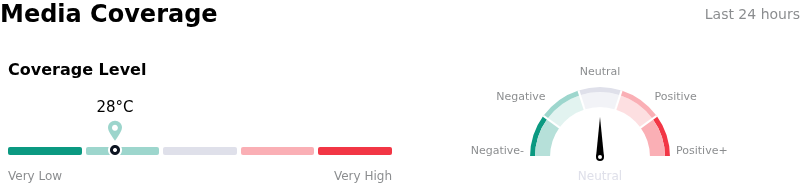

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 28, indicating a low level of media attention. The overall market sentiment index is currently in neutral zone.

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $389.29, a high of $650.00, and a low of $86.28.

Company Specific Risks:

- Micron's HBM4 memory has reportedly been dropped from Nvidia's next-generation Vera Rubin accelerator supplier list, according to recent Korean media reports, posing a potential threat to its high-bandwidth memory market share.

- The company's shares are noted to be trading significantly above estimated fair value, with a 99.7% premium, signaling a potential valuation risk exacerbated by a recent 6.2% decline in 30-day returns and overall stock momentum struggle over the past month.

- Micron faces inherent vulnerability to the cyclical nature of the memory industry, with ongoing analyst concerns regarding potential oversupply, decreased bit demand growth, competitive pressures, and broader macroeconomic uncertainties leading to possible pricing declines.

- Rising operating costs and a massive increase in capital expenditure requirements are identified as downside risks that could negatively impact Micron's near-term profitability.

Related Articles

Ahead of CPI Release, Credit Crisis Panic Haunts Markets, Wall Street Eyes How Inflation Data Will Impact US Stocks

TradingKey - At 8:30 AM ET on Wednesday, the U.S. Bureau of Labor Statistics will release the February Consumer Price Index (CPI) report, which traders view as setting the tone for investment direction.

Trump Wants TACO? The Script for an Iran War May No Longer Be His to Write

TradingKey - As the US-Israel-Iran conflict enters its second week, new developments have emerged in the situation. On March 9 local time, U.S. President Trump sent a clear signal during a press conference, stating that military operations against Iran would end "soon" but would not be completed within this week. This statement has been interpreted by observers as a direct signal that the U.S. is seeking a "graceful exit." In response to the de-escalatory signals from the U.S., Iran’s stance remains defiant.

Bitcoin Price Analysis: BTC Eyes $72K Breakout Amid Mideast Supply Shocks and Short Squeeze Risk

BTC faces a critical $72K resistance amid Middle East supply shocks and a $4.3B short squeeze risk. Explore the latest btc price trends, institutional ETF outflows, and the impact of the upcoming "Clarity Act" on bitcoin’s market forecast.

Micron vs. Samsung vs. SK Hynix: Is MU Stock the Best Memory Stock for 2026?

TradingKey - Relying on strong AI demand, more memory per system, and sluggish supply response, 2026 will be the memory cycle. Micron Technology (MU) is now in an excellent competitive position today with HBM3E and looking to ramp HBM4E into Nvidia’s Vera Rubin platforms in the second half of 2026.