Booking Holdings Inc Stock Moved Up by 3.42% on Mar 4: Key Drivers Unveiled

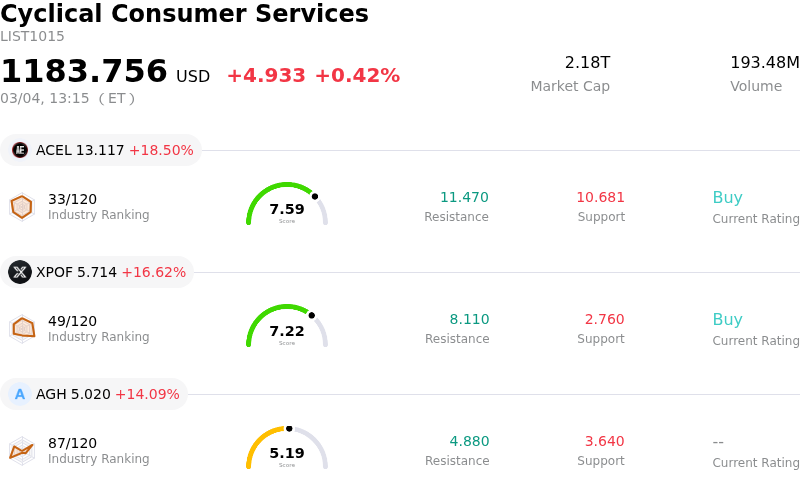

Booking Holdings Inc (BKNG) moved up by 3.42%. The Cyclical Consumer Services industry is up by 0.42%. The company outperformed the industry. Top 3 gainers of the industry: Accel Entertainment Inc (ACEL) up 18.50%; Xponential Fitness Inc (XPOF) up 16.62%; Aureus Greenway Holdings Inc (AGH) up 14.09%.

Booking Holdings experienced upward movement and notable intraday volatility today, largely driven by a combination of strong financial outlook, strategic corporate announcements, and positive analyst sentiment.

The company presented its strategic vision at the Morgan Stanley Technology, Media & Telecom Conference 2026, where it outlined ambitious medium-term growth targets. Management indicated an aim for 8% top-line and 15% EPS growth, building on a successful 2025 where it surpassed these goals with 10% gross bookings and revenue growth and 18% EPS growth. For 2026, Booking Holdings projects a 9% increase in both top-line metrics and a 15% rise in EPS, a forecast that likely bolstered investor confidence. The presentation also highlighted the transformative role of generative AI in enhancing customer service and reducing operational costs, along with an increased $700 million reinvestment program for 2026 designed to boost revenue and bottom-line impact.

Further supporting the positive sentiment, Booking Holdings announced an increase in its quarterly dividend to $10.50 per share, marking a 9.4% rise from the previous payout. This dividend increase, payable on March 31, 2026, signals robust financial health and a commitment to returning value to shareholders. Additionally, the company's board approved a 25-to-1 stock split, effective April 2, 2026. While a stock split is a cosmetic adjustment, it often acts as a psychological catalyst, enhancing liquidity and attracting broader retail investor interest, which historically has been associated with positive post-split performance.

Analyst community views also contributed to the upward trend. Several firms reiterated "Buy" ratings for BKNG, with BTIG Research reaffirming its "buy" rating and assigning a price target suggesting substantial potential upside. The consensus among analysts indicates a "Moderate Buy" rating, with an average price target forecasting significant appreciation over the next year. These positive forecasts are underpinned by the company's strong performance, including a recent earnings beat where reported EPS and revenue exceeded consensus estimates.

The broader industry backdrop also remains favorable, with Booking Holdings well-positioned to capitalize on trends such as the growing demand for "experientialism" in travel and expansion in key markets like Asia-Pacific. The combined effect of these financial, operational, and market-related factors fueled the positive movement in the stock today.

Technically, Booking Holdings Inc (BKNG) shows a MACD (12,26,9) value of [-240.55], indicating a neutral signal. The RSI at 39.00 suggests neutral condition and the Williams %R at -37.31 suggests oversold condition. Please monitor closely.

Booking Holdings Inc (BKNG) is in the Cyclical Consumer Services industry. Its latest annual revenue is 26.92B, ranking 2 in the industry. The net profit is 5.40B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 5844.35, a high of 7746.00, and a low of 4495.00.

Company Specific Risks:

- Booking Holdings faces a proposed $530 million fine from the Spanish competition authority for alleged competition law violations, which has already contributed to a reduction in Q4 net income.

- Investor concerns persist regarding the potential for advanced AI operating systems to disintermediate traditional online travel agencies, threatening Booking Holdings' business model and future profit margins.

- Decelerating room night growth projections for Q1 2026 and a significant reinvestment plan for the year are causing investor apprehension, overshadowing otherwise strong Q4 2025 earnings and contributing to selling pressure.

- Multiple analyst firms have recently reduced their price targets for Booking Holdings, citing concerns over valuation, future margin pressures, and increased expenditures related to AI integration.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.