As Project Backlog Grows, Is Now the Time to Buy Kinder Morgan?

While Kinder Morgan's (NYSE: KMI) stock didn't get a huge lift from its recent earnings report, it's been a strong performer this year, with its price up about 40% year to date.

The pipeline operator has been showing relatively modest growth this year, and its third-quarter results were were no different. However, management's commentary pointed to a lot of growth opportunities ahead.

Let's dig into Kinder Morgan's most recent results and look at why 2025 could be shaping up to be a good year for the company.

Lackluster Q3 results, but a bright outlook

Kinder Morgan's Q3 results weren't anything to write home about. Its adjusted earnings per share (EPS) was flat year over year at $0.25, while its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) edged up 2% to $1.88 billion. Its distributable cash flow (DCF), which is similar to free cash flow except that it only subtracts maintenance capital expenditures (capex) and not growth capex, was essentially flat at $1.1 billion.

Volumes across its systems, meanwhile, were mixed. Natural gas transport volumes rose 2% year over year, while natural gas gathering volumes rose 4%. However, crude and condensate volumes were down 4%. Kinder Morgan ended the quarter with a leverage ratio (net debt divided by trailing-12-month adjusted EBITDA) of 4.1. It declared a dividend of $0.2875 per share, unchanged from last quarter and up 2% compared to a year ago. That translates to a forward yield of 4.6%.

Kinder Morgan management lowered its full-year guidance, saying it expects adjusted EBITDA to be about 2% below prior forecasts and adjusted EPS to be approximately 4% lower than expected. Previously, the company guided for adjusted EBITDA of $8.16 billion and DCF of $5 billion, an 8% increase for both. It now sees itself ending the year at 4 times leverage. It said the reduction was due to lower commodity prices and a delay in the start-up of a renewable natural gas (RNG) facility.

Despite the lowered 2024 guidance, the company said it has "never seen a macro environment so rich with opportunities for incremental build out of natural gas infrastructure." It credited the artificial intelligence (AI)-fueled data center buildout, as well as liquified natural gas (LNG) exports and the exports of natural gas to Mexico, for its bullishness.

Kinder Morgan highlighted its previously announced $3 billion South System Expansion 4 project to help with the growing power needs in the southeast, as well as the expansion of its GCX system in Texas to transport associated natural gas out of the Permian. It expects to announce additional growth projects in the coming months that will lead to sustained and consistent growth in EPS, EBITDA, and DCF.

Overall, it has a backlog of $5.1 billion, up 34% from a year ago. It is looking to spend around $2 billion a year on capex, perhaps more, with the ability to fund up to $2.5 billion for its cash-flow generation.

Image source: Getty Images.

Is now a good time to buy the stock?

While it has other businesses, Kinder Morgan is primarily a transporter of natural gas. Nearly two-thirds of its cash flow comes from activities involving natural gas, and within that segment, 88% is from transport and storage while the remainder is from gathering and processing.

The company's system is also very tied to Texas and Louisiana, which is where a lot of demand growth is expected to take place due to cheap associated gas from the Permian and export facilities in the Gulf. Earlier this month, the Department of Energy even granted a long-term permit for natural gas to be delivered to Mexico, turned into LNG, and then shipped from Mexico's west coast to any country that has a free trade agreement with the U.S.

As such, the combination of increasing AI power consumption and export opportunities bode well for Kinder Morgan over the next several years.

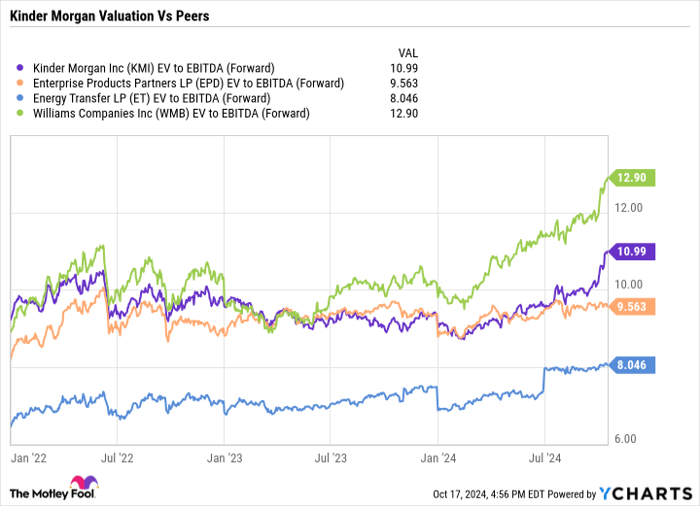

From a valuation perspective, Kinder Morgan trades at a forward enterprise value-to-EBITDA multiple of about 11 times, which is higher than its peers that are structured as master limited partnerships (MLPs), but below rival Williams Companies.

KMI EV to EBITDA (Forward) data by YCharts

While I prefer Kinder's MLP peers Energy Transfer and Enterprise Products Partners due to the valuation gap, similar natural gas opportunity set, and better recent growth, Kinder is still a solid option for investors who don't want to deal with the MLP structure and K-1s. In addition, despite its higher valuation, it still trades below where the sector traded a few years before the pandemic.

As such, I'd still be a buyer of Kinder Morgan at current levels.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,285!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,456!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $411,959!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 14, 2024

Geoffrey Seiler has positions in Energy Transfer and Enterprise Products Partners. The Motley Fool has positions in and recommends Kinder Morgan. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.