Corning Inc Stock (GLW) Closed Down by 4.96% on Jul 7: What Investors Need To Know

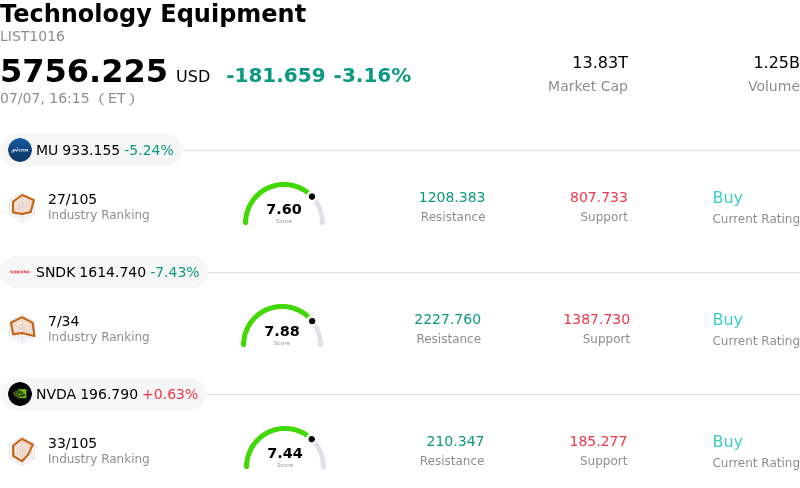

Corning Inc (GLW) closed down by 4.96%. The Technology Equipment sector is down by 3.16%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 5.24%; SanDisk Corporation (SNDK) down 7.43%; NVIDIA Corp (NVDA) up 0.63%.

What is driving Corning Inc (GLW)’s stock price down today?

Corning Incorporated experienced a downward shift as investors continued to unwind positions in artificial intelligence and semiconductor infrastructure stocks. This decline extended a multi-day pullback from the stock's recent all-time high reached in late June. The broader market has witnessed a technical unwind in high-flying technology names, and Corning, which has functioned as a primary beneficiary of the AI fiber thesis, became highly vulnerable to profit-taking following its parabolic run.

The downward pressure has also been exacerbated by structural valuation concerns. Following its massive AI-driven rally, Corning was trading at a trailing price-to-earnings ratio exceeding ninety times, making the stock highly priced for perfection and sensitive to any shifts in macro sentiment or institutional portfolio rotations. Additionally, recent Form 4 filings with the SEC revealed notable executive insider selling over the preceding weeks, including transactions by the chief executive officer and other senior leadership, which failed to see any offsetting insider purchases and dampened immediate institutional buying appetite.

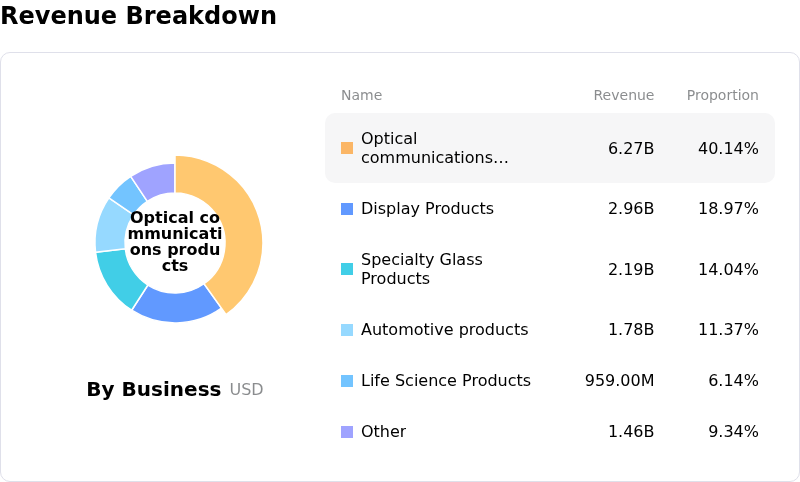

Despite the current drop, Wall Street analysts maintain a highly constructive long-term outlook on Corning's fundamentals. Major investment firms, including Oppenheimer and Bank of America, recently reiterated outperform and buy ratings while raising their respective price targets. Analysts emphasize that the demand signal for Corning's optical communications products remains robust. The rapid expansion of artificial intelligence data centers continues to require massive capital expenditures on optical fiber, cabling, and connectivity. Large-scale contracts with major hyperscalers, such as Meta and Amazon, are expected to bolster the company's financial performance through the second half of the year.

While the short-term pullback reflects a valuation normalization and technical shakeout among AI infrastructure hardware plays, Corning's underlying growth narrative in optical networks and its expanding footprint in high-margin automotive glass and ceramic technologies continue to underpin positive long-term analyst projections.

Technical Analysis of Corning Inc (GLW)

Technically, Corning Inc (GLW) shows a MACD (12,26,9) value of -0.522, indicating a neutral signal. The RSI at 48.121 suggests neutral condition and the Williams %R at 77.734 suggests sell condition. Please monitor closely.

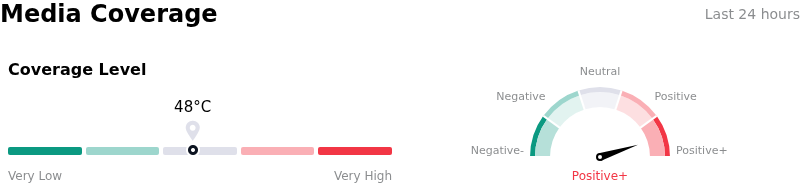

Media Coverage of Corning Inc (GLW)

In terms of media coverage, Corning Inc (GLW) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of Corning Inc (GLW)

Corning Inc (GLW) is in the Technology Equipment industry. Its latest annual revenue is $15.63B, ranking 7 in the industry. The net profit is $1.60B, ranking 3 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $216.22, a high of $270.00, and a low of $158.87.

More details about Corning Inc (GLW)

Company Specific Risks:

- Severe Valuation Premium and Overextension: Following an aggressive AI-fueled rally, Corning’s trailing price-to-earnings (P/E) ratio has spiked past 93x to 105x—far exceeding its historical 5-year median of 45.6x. This massive premium leaves the stock highly vulnerable to sharp technical corrections, profit-taking, and index-driven sell-offs.

- Heavy Executive Insider Divestment: SEC filings show zero offsetting insider buying against massive executive liquidations, with top leadership—including CEO Wendell Weeks and CHRO Michelle Gullo—unloading over $54.1 million in shares near recent peak price levels.

- Operational Bottlenecks and Elevated Costs: Corning is incurring a significant financial headwind due to an extended, costly maintenance shutdown at its solar wafer facility. This planned transition to a permanent power system and equipment upgrade is imposing an unexpected $30 million in additional expenses, weighing heavily on near-term margins.

- Capital Intensity and Weak Free Cash Flow Conversion: Despite robust top-line revenue growth, Corning remains a capital-heavy manufacturer with planned capital expenditures of $1.7 billion. This intensive overhead resulted in adjusted free cash flow of just $188 million on $4.35 billion in revenue, highlighting a deep disconnect between the stock's software-like valuation and its physical asset-heavy business model.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.