Shell PLC Stock (SHEL) Moved Up by 3.25% on Jul 7: Drivers Behind the Movement

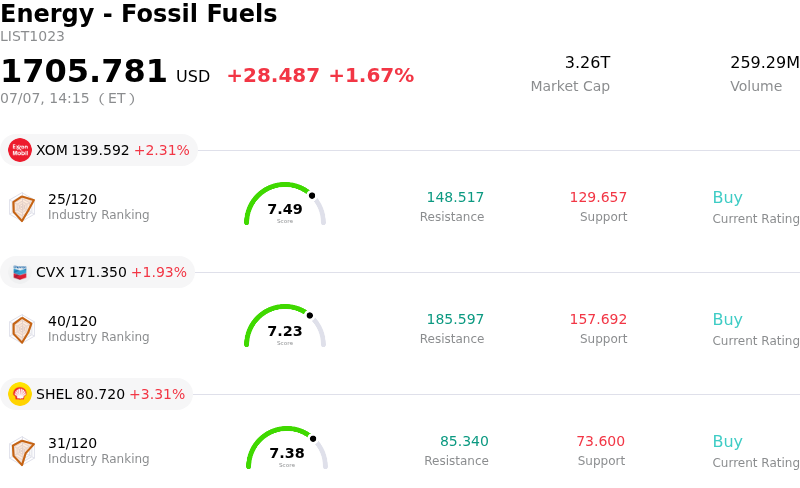

Shell PLC (SHEL) moved up by 3.25%. The Energy - Fossil Fuels sector is up by 1.67%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Exxon Mobil Corp (XOM) up 2.31%; Chevron Corp (CVX) up 1.93%; Shell PLC (SHEL) up 3.25%.

What is driving Shell PLC (SHEL)’s stock price up today?

The rise in Shell’s share price was driven primarily by a positive and reassuring second-quarter trading update that exceeded investor expectations, coupled with a broader lift in global oil prices. This pre-results announcement provided a welcome sense of relief to the market, highlighting the energy giant’s operational resilience and its ability to capitalize on market volatility.

The core catalyst was Shell's upward revision of its production guidance. Despite the ongoing conflict in the Middle East significantly impacting Qatari volumes and shutting down the Pearl gas-to-liquids facility in March, Shell managed to raise its projected second-quarter integrated gas production and upstream output limits above its previous forecasts. This proved that the underlying production baseline remains far more robust than analysts had feared following regional disruptions.

Furthermore, Shell announced that earnings from its integrated gas trading and optimization desk are expected to be significantly higher than in the previous quarter. Market dislocations and price volatility in commodity markets, while challenging for physical supply chains, created highly profitable conditions for the company's trading operations. Additionally, the refining margin in its chemicals and products unit is tracking higher than in the first quarter.

Financially, the company projected a dramatic turnaround in its capital position. Following a massive working capital outflow in the first quarter, Shell expects a substantial cash inflow for the second quarter, largely driven by the normalization of commodity price volatility. This rapid reversal alleviates pressure on the balance sheet and bolsters investor confidence regarding the sustainability of the company's aggressive shareholder return initiatives, including dividends and active share buyback programs.

Beyond company-specific metrics, market sentiment was supported by a pick-up in international crude benchmarks, driven by persistent geopolitical uncertainty in crucial shipping lanes like the Strait of Hormuz. Combined with an attractive, discounted valuation relative to historical and sector averages, the robust update sparked widespread buying interest, triggering a volatile but strong upward push in Shell's shares.

Technical Analysis of Shell PLC (SHEL)

Technically, Shell PLC (SHEL) shows a MACD (12,26,9) value of -0.220, indicating a sell signal. The RSI at 37.065 suggests neutral condition and the Williams %R at 72.271 suggests sell condition. Please monitor closely.

Fundamental Analysis of Shell PLC (SHEL)

Shell PLC (SHEL) is in the Energy - Fossil Fuels industry. Its latest annual revenue is $266.89B, ranking 2 in the industry. The net profit is $17.84B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $95.66, a high of $122.40, and a low of $46.46.

More details about Shell PLC (SHEL)

Company Specific Risks:

- Severe Sequential Production Drop in Integrated Gas: According to Shell’s Q2 2026 trading update released on July 7, 2026, Integrated Gas production is projected to fall sharply to between 610,000 and 650,000 barrels of oil equivalent per day (boe/d). This represents a significant decline from the 909,000 boe/d achieved in Q1 2026, driven by ongoing regional conflicts in the Middle East that have disrupted Qatari gas volumes and caused structural asset damage.

- Refining and Chemicals Margin Dislocation: Despite guiding for higher indicative refining margins of $20/bbl and chemicals margins of $240/tonne in Q2 2026, Shell explicitly cautioned in its July 7, 2026 update that severe market dislocations will cause actual, realized refining and chemicals margins to fall below these calculated indicative figures.

- Elevated Tax Liabilities and Broad Profitability Swings: The company raised its Q2 2026 taxation guidance to a range of $2.6 billion to $3.4 billion, up from $2.3 billion in Q1 2026. Furthermore, the Renewables and Energy Solutions segment continues to experience extreme performance swings, with Q2 earnings guided to a highly volatile range spanning from a $300 million loss to a $300 million profit.

- Long-Term Resource Depletion: Institutional analysts remain highly cautious regarding Shell's long-term organic pipeline, highlighting that its total oil reserves have declined to their lowest levels since 2013. This depletion forces the company into highly capital-intensive M&A cycles, such as the C$22 billion ARC Resources acquisition, which is driving elevated capital expenditure projections of $24 billion to $26 billion for 2026.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.