KLA Corp Stock (KLAC) Moved Down by 6.56% on Jul 7: What Signal Does It Send?

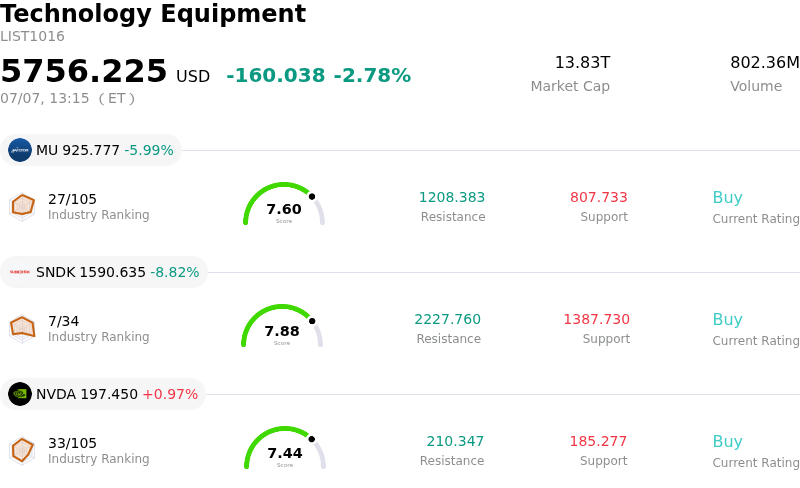

KLA Corp (KLAC) moved down by 6.56%. The Technology Equipment sector is down by 2.78%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 5.99%; SanDisk Corporation (SNDK) down 8.82%; NVIDIA Corp (NVDA) up 0.69%.

What is driving KLA Corp (KLAC)’s stock price down today?

KLA Corporation (KLAC) experienced significant intraday volatility and a sharp downward move, driven by a combination of sector-wide profit-taking, high valuation sensitivities, and localized insider transaction signals. Despite solid fundamentals and the company's leading role in the critical semiconductor process control niche, broader market forces and specific industry triggers heavily pressured the stock.

A primary catalyst for the decline was a major global semiconductor sector reset triggered by international earnings news. Samsung Electronics posted an exceptionally strong preliminary quarterly operating profit, yet its stock fell sharply in Asian trading as the results failed to satisfy the market’s most optimistic forecasts. This dynamic immediately sparked profit-taking across global markets, hitting semiconductor equipment makers particularly hard. Because KLA provides process control and metrology systems to major global chipmakers, its valuation is highly sensitive to changes in memory and capital expenditure sentiment, leaving it exposed to broader sector-wide adjustments.

Furthermore, KLA entered this trading session following a massive run-up over the past year, leaving its valuation multiples stretched. Market analysts had increasingly pointed to the company’s premium trading multiples relative to near-term earnings growth, making the stock highly susceptible to any shifts in momentum or broader technology-sector rotations. The overall semiconductor capital equipment space has faced an ongoing divergence, where massive AI infrastructure spending contrasts with a more cautious outlook on mature-node production and memory-capex cycles, compounding pressure on equipment stocks.

Adding to the downward momentum were recent regulatory disclosures revealing notable insider selling. Highly visible filings showed that KLA’s Chief Financial Officer and an Executive Vice President both disposed of shares. Although these transactions were executed under pre-planned trading schedules or aimed at covering tax obligations, the timing of these sales further cooled short-term retail and institutional sentiment, contributing to the stock gapping down at the opening bell.

While KLA’s long-term growth story remains supported by advanced packaging demand and the AI chip transition, today’s sharp move reflects a typical high-valuation squeeze where macroeconomic momentum, global peer earnings, and executive stock sales converged to prompt immediate risk mitigation from investors.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of 29.779, indicating a neutral signal. The RSI at 22.448 suggests sell condition and the Williams %R at 93.322 suggests oversold condition. Please monitor closely.

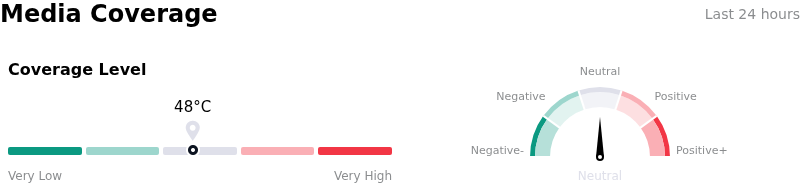

Media Coverage of KLA Corp (KLAC)

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $211.75, a high of $317.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- Elevated Input Costs and Margin Compression: KLA is facing a persistent 100 basis point gross margin headwind driven directly by surging prices for high-speed DRAM memory chips used in the image processing computers of its inspection systems. This input cost inflation is compounded by an additional 50 to 100 basis point margin drag from international tariffs.

- Severe Geopolitical and Trade Export Risks: The company remains highly exposed to stringent Bureau of Industry and Security (BIS) export regulations, with China representing 34% of sales in Q3 fiscal 2026 and 37% cumulatively over the first nine months. Any potential expansion of regulatory bans to encompass legacy tools or broadband plasma systems threatens to instantly compromise a $4 billion revenue pool.

- High Customer Concentration Vulnerabilities: Because the leading-edge wafer fabrication market is dominated by a select handful of global semiconductor giants, KLA's high-end process control business is highly concentrated. If any of these major customers delay their capital expenditure roadmaps, reduce capacity expansion plans, or adjust fab build timelines, KLA's projected earnings run rate faces swift downward revisions.

- Valuation Premium Overhang and Insider Liquidations: Trading at approximately 45x to 50x forward earnings, KLA's valuation leaves virtually no margin of safety if near-term growth decelerates. This vulnerability has been underscored by recent Form 4 filings detailing over $11 million in combined insider stock liquidations by CFO Bren Higgins and EVP Mary Beth Wilkinson, which triggered a pre-market gap down and heightened intraday volatility.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.