Lam Research Corp Stock (LRCX) Moved Down by 7.54% on Jul 7: What Signal Does It Send?

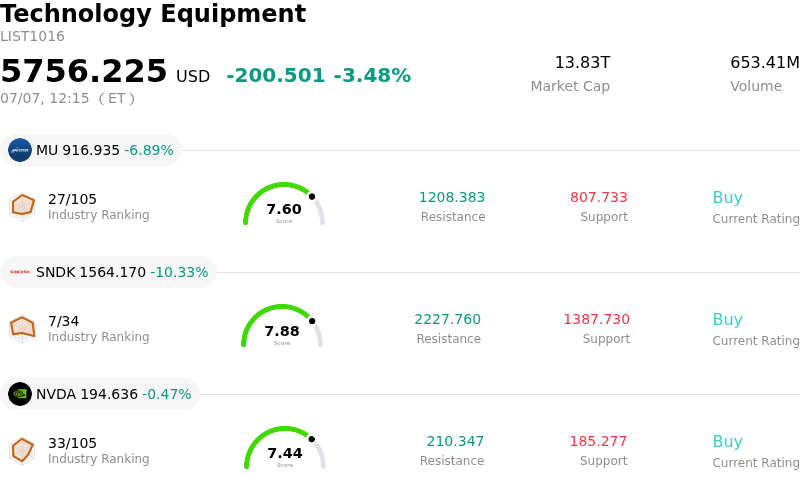

Lam Research Corp (LRCX) moved down by 7.54%. The Technology Equipment sector is down by 3.48%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 6.89%; SanDisk Corporation (SNDK) down 10.33%; NVIDIA Corp (NVDA) down 0.47%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

The intraday volatility and downward pressure on Lam Research Corporation (LRCX) are primarily driven by a broad-based, sector-specific sell-off across the semiconductor industry, coupled with high valuation anxiety and corporate insider selling.

The immediate trigger for the downturn stems from international chipmaker performance that fell short of demanding investor expectations. While Samsung Electronics posted a significant increase in preliminary quarterly operating profit, the figures only slightly beat analyst estimates, failing to justify the extreme valuation expansion seen across the artificial intelligence and semiconductor space over the first half of the year. This sparked widespread profit-taking that rapidly spread to major U.S. chipmakers and wafer fabrication equipment manufacturers, directly dragging down industry heavyweights like Applied Materials and Intel, and pulling Lam Research along in its wake.

Furthermore, institutional investors are increasingly questioning the long-term sustainability of capital expenditure in AI infrastructure. Reports of tech giants exploring ways to monetize excess cloud and computing capacity have signaled that the peak of hyper-scaler AI infrastructure buildout may be nearing. Because wafer fabrication equipment manufacturers operate in a highly cyclical market, any perceived threat of a capital expenditure deceleration in advanced logic and memory nodes results in rapid multiple compression. This is particularly impactful for Lam Research, which entered the second half of the year trading at a premium valuation following months of aggressive gains.

Internal technical pressure has also mounted following recent SEC filings highlighting sustained insider selling. Within the last few months, high-profile executives, including President and CEO Timothy Archer and several directors, executed pre-arranged share liquidations totaling tens of millions of dollars. Coming at a time when the stock is already being reassessed for overvaluation, these high-volume insider sales have further weighed on retail and institutional investor confidence, accelerating the downward momentum despite positive long-term analyst target adjustments from major Wall Street firms.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of -11.281, indicating a neutral signal. The RSI at 48.180 suggests neutral condition and the Williams %R at 91.955 suggests oversold condition. Please monitor closely.

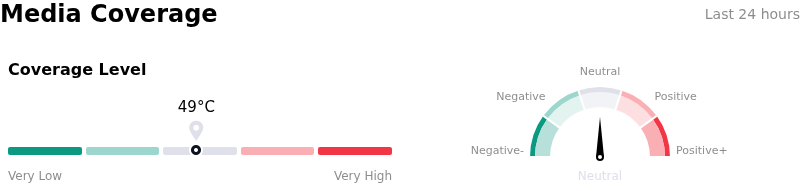

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $346.42, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Severe Structural Shipment Deceleration: Institutional analysts are warning of a significant cyclical cooling across 3D NAND and mature-logic nodes, projecting Lam Research's system shipment growth to sharply decelerate to just 3% in 2026—a steep decline from the 82% expansion observed in 2025.

- Downstream Capital Allocation Shifts: The company's near-term order book is facing compression due to strategic capacity reallocations by major clients like SK Hynix, who are pivoting capital expenditure priorities to chase conventional DRAM margins instead of accelerating next-generation AI high-bandwidth memory (HBM4) ramps.

- Extreme Valuation and Multiple Compression: Following a massive rally of over 150% in the first half of 2026, the stock trades at a highly elevated trailing P/E ratio exceeding 67x. This leaves the stock highly vulnerable to aggressive institutional sector rotations, as seen in the recent sharp drop of over 10% in a single session.

- Material Insider Selling: Recent regulatory filings indicate significant insider profit-taking, highlighted by President and CEO Timothy Archer selling 30,000 shares of common stock totaling approximately $11.7 million on July 2, 2026, which has intensified concerns over near-term peak valuation.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.