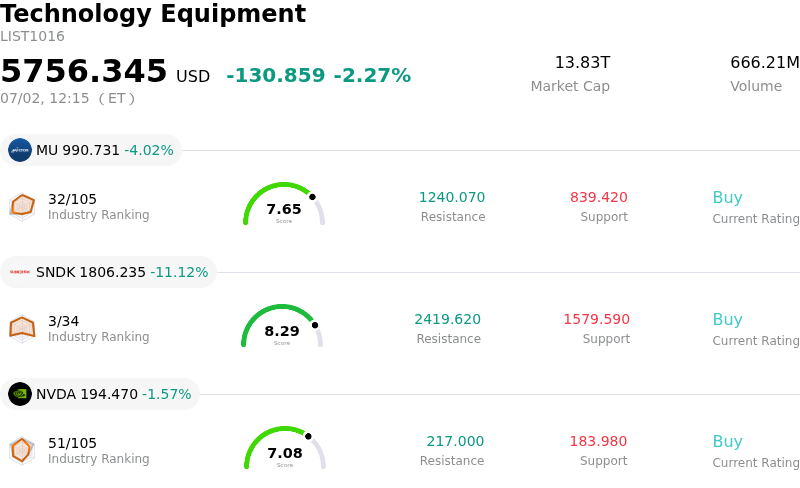

Lam Research Corp Stock (LRCX) Moved Down by 7.40% on Jul 2: What Investors Need To Know

Lam Research Corp (LRCX) moved down by 7.40%. The Technology Equipment sector is down by 2.27%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 4.02%; SanDisk Corporation (SNDK) down 11.12%; NVIDIA Corp (NVDA) down 1.57%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

Lam Research has experienced significant downward pressure and intraday volatility, driven by a convergence of macroeconomic headwinds, broader semiconductor sector corrections, and company-specific valuation concerns. A major trigger was the weaker-than-expected ADP private payrolls report, which signaled a cooling labor market and introduced fresh economic uncertainty ahead of the rescheduled monthly non-farm payroll data. This macro-level anxiety was compounded by rising bond yields and monetary policy caution, prompting institutional investors to rotate out of high-flying tech and growth stocks.

The broader semiconductor sector faced a severe sentiment shock following Meta's announcement of a new cloud service to sell its surplus AI computing power. This raised concerns that major hyperscalers might have overbuilt their artificial intelligence infrastructure, suggesting a looming oversupply and a potential deceleration in the AI-led capital expenditure cycle. Given that Lam Research's wafer fabrication equipment is heavily utilized in high-density memory and advanced packaging, any indication that Big Tech is cooling its pace of AI hardware accumulation directly pressures the company's near-term demand projections. This fear was reflected in a sharp global sell-off of memory chipmakers, directly dragging down equipment manufacturers.

Additionally, Lam Research's premium valuation left little room for error. Following an extraordinary run in the first half of the year, the stock traded at a significant valuation premium relative to historic norms and its peer group. As doubts arose regarding the sustainability of current wafer fabrication spending, institutional profit-taking accelerated. Recent material insider selling, including a major share divestment by a company director, further dampened retail and institutional investor confidence, signaling that insiders may view the valuation as fully priced.

Finally, persistent geopolitical risks continue to weigh on the company. With China accounting for a substantial portion of Lam Research's total revenue, the threat of stricter export controls remains a lingering headwind. These combined factors—macroeconomic jitters, sector-wide oversupply fears triggered by Big Tech strategy shifts, stretched valuations, insider selling, and geopolitical exposure—have intensified profit-taking and fueled the sharp intraday retreat.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 2.339, indicating a buy signal. The RSI at 56.335 suggests neutral condition and the Williams %R at 46.178 suggests neutral condition. Please monitor closely.

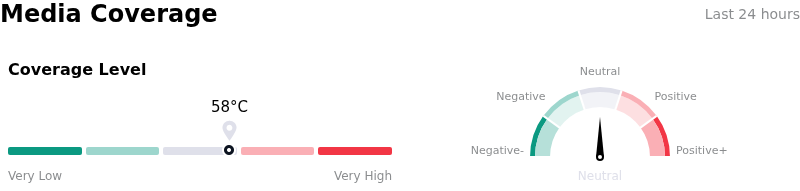

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 58, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $343.42, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- **Stretched Valuations and Multiple Compression:** Following a price surge of over 150% in the first half of 2026, LRCX is trading at a premium trailing P/E exceeding 70x. This extreme multiple expansion leaves the stock highly vulnerable to sharp pullbacks and multiple compression, which triggered a cumulative decline of over 15% across consecutive trading sessions as institutional investors aggressively rotated out of overextended semiconductor equipment names.

- **Geopolitical Vulnerabilities and China Revenue Concentration:** China remains a heavily concentrated source of revenue for Lam Research, contributing 34% to 35% of overall sales. This geographical exposure leaves the company acutely vulnerable to evolving U.S. export controls and "affiliate rules," which are projected to create a direct revenue headwind of approximately $600 million in fiscal year 2026.

- **Escalating Insider Selling and Form 144 Filings:** Market confidence has been dented by significant executive and director stock liquidations. Notably, on July 2, 2026, President and CEO Timothy Archer filed a Form 144 outlining his intent to sell 30,000 shares of common stock, closely following a $19.1 million divestment by Director Eric Brandt and a $4.6 million liquidation by SVP Neil Fernandes.

- **Deceleration in System Shipments and Capex Commitments:** Amidst cyclical cooling across 3D NAND and mature-logic nodes, institutional analysts are warning of a severe deceleration in Lam’s system shipment growth down to just 3% in 2026, a steep decline from the 82% growth rate observed in 2025. This structural slowdown is compounded by falling customer down payments, indicating a near-term contraction in capital expenditure commitments.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.