AMD Price Forecast: Stock Falls 6% After Record High—Is This the Best Buy-the-Dip Opportunity?

AI Podcast

AMD is experiencing a minor correction after a 171% year-to-date rally, currently trading near $547-$555. Despite short-term volatility, the company’s outlook remains robust, supported by strong Q1 results, record Data Center revenue, and the production ramp of its 2nm EPYC "Venice" CPUs. A major supply agreement with Meta further bolsters its AI accelerator trajectory. While Wall Street maintains bullish price targets up to $700, risks include high valuation multiples, potential declines in gaming demand, and share dilution. Investors should monitor Q2 earnings targets and macroeconomic data as critical benchmarks for the stock's premium valuation.

TradingKey - AMD (AMD) stocks are trading near $547 to $555, or about 5% to 6% off Tuesday's close of $580.91 and up to a new 52-week high earlier this week. The recent pullback has taken some of the heat out of the rally, but it hasn't changed the bigger picture. AMD still has an impressive YTD gain of +171% and an increase of over +300% on the last 12 months.

Those who bought the stock when it reached $580 are on the short-term losing side, while those sitting on the sideline have received their best shot to buy the stock in over a month. It should also be noted that this drop has been mirrored by the general decline in semiconductor stocks, and the real question is not what the chart looks like now, but what's changed in AMD's business.

Q1 Results Set the Bar High

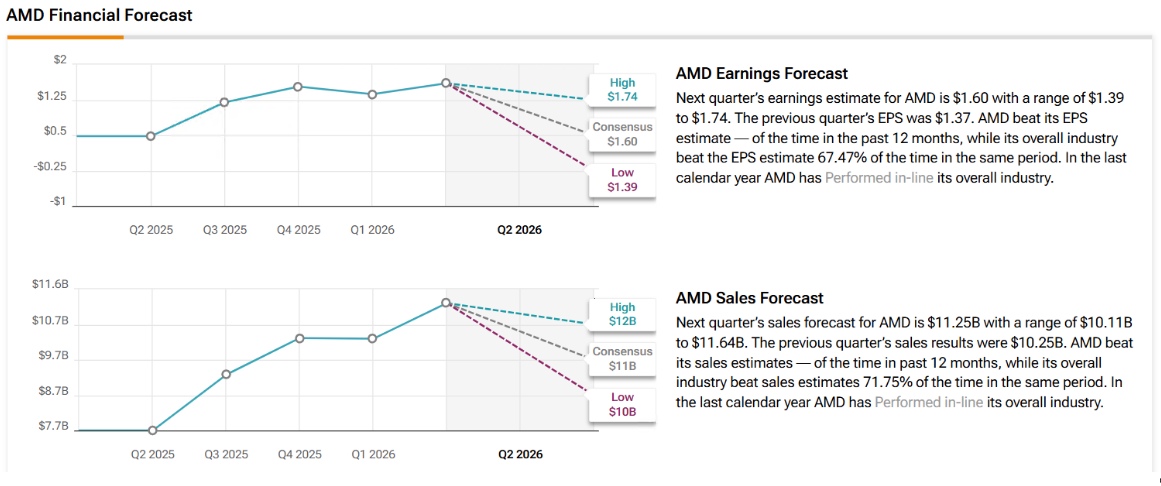

Earlier this year, AMD released its fiscal first-quarter 2026 results, which continue to support the stock's strong performance. Revenue was at $10.25 billion, a 37.85% increase from the prior year, and the non-GAAP EPS was $1.37, almost 6% higher than analysts were expecting. Its Data Center segment was the star performer, with revenue of $5.78 billion, a 57% increase from a year ago.

Moving forward, management expects to report roughly $11.2 billion of second quarter revenue, representing a year-over-year increase of approximately 46%, and non-GAAP gross margins of about 56%. Free cash flow also increased more than threefold to $2.57 billion for the quarter. That Q2 guidance is now the benchmark for investors. If it does not perform well, it would be the first real test of the premium the market has placed on the stock.

Image Source: TipRanks

The EPYC "Venice" Server CPU Ramp

Although much focus has been on AI GPUs, AMD's server CPU business could potentially be more significant in the long-term.

The company's sixth-generation processors, the 2nm EPYC "Venice" chips, have officially launched into production ramp on May 21, and are expected to see wider availability in the second half of 2026. Management notes that it is seeing more customers validate and deploy Venice than any previous EPYC generation – and is raising its forecast on the total addressable market for server CPUs to $120 billion by 2030.

This may be one of the most significant announcements to watch for long-term investors. The server CPU market share is more long-lasting and typically offers higher margins than individual GPU victories, making the business one of the key contributors to future revenue growth.

MI450 GPUs and the Meta Mega-Deal

On the AI accelerator front, AMD won one of its largest business victories ever.

Meta has pledged to roll out as many as 6 gigawatts of AMD Instinct GPUs, and the first gigawatt is based on a custom platform that features the AMD MI450 chip. It marks one of the biggest public AI infrastructure commitments from AMD, and will effectively provide the forthcoming MI400/MI450 product family with a hyperscale customer before the actual shipments are in full production.

This deal is the latest confirmation that key cloud computing firms are making a push to diversify their GPU supply chain, even as investors ponder whether AMD can catch up with Nvidia in the AI accelerators business.

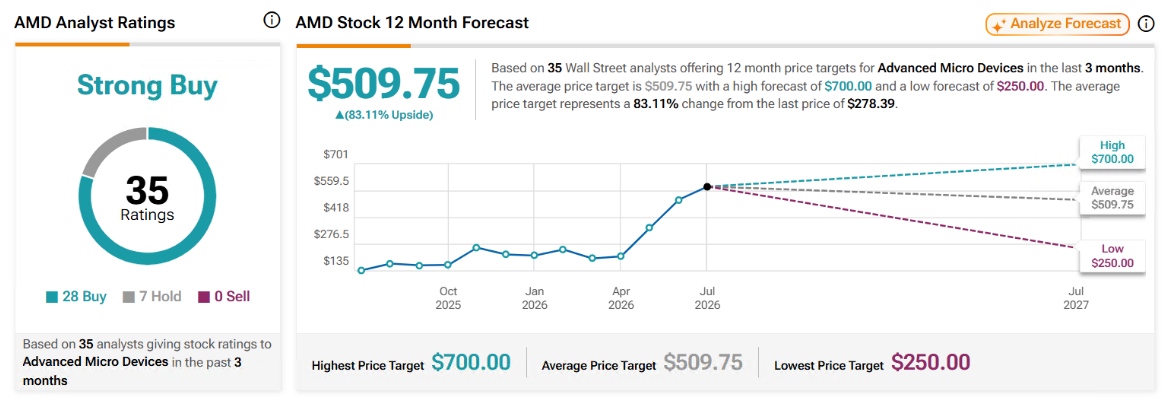

Wall Street Keeps Raising the Bar

Wall Street has become noticeably more optimistic over the past two weeks.

Wells Fargo raised the price estimate to $615, but its investment rating remained at Overweight due to higher expectations of server CPU revenue as opposed to just the AI GPU excitement. Cantor Fitzgerald upped its bet to $700 on June 29, and is one of the highest betters on the Street. UBS also raised its target only days ago, to a similarly bullish range.

The common theme behind these upgrades is clear: analysts are becoming increasingly positive about AMD's CPU business in addition to its AI accelerator opportunity.

Where the Risk Sits

AMD isn't risk-free, even with the promising forecast.

The stock now trades at about 190 to 203 times trailing earnings and about 118 times forward earnings, meaning that it has little margin for error. Management has also indicated that gaming and PC client demand may decline by 20% or more in the second half of the year, which may offset some of the strength in the Data Center business.

The net selling bias of insider transactions has also been negative, and a few of AMD's biggest customer deals involve equity-based compensation arrangements that slowly dilute existing shareholders.

None of these are reasons to drawback the long-term trend, but a further reminder that investors do need to be disciplined with position sizing following such an extended rally.

Analyst Targets and What to Watch Next

Even after this week's decline, Wall Street continues to see additional upside.

The current analyst price targets span from about $586 to $700, with Cantor Fitzgerald's $700 price target being at the high end of the range. Those predictions are based on continued on-time rollouts of the Venice server CPU and the MI450 deployments.

Image Source: TipRanks

The next big driver is Thursday's delayed June jobs report, which could affect the rest of the semiconductor industry, and confirmation that second-quarter revenue falls within management's $11.2 billion forecast.

From a technical standpoint, traders would be interested in the $538-$547 range as an area of support. If prices move below it, they could resume the bull market toward $500, while a move above $580 would indicate that this week's pullback was just a minor correction in a larger long-term uptrend.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.