Applied Materials Inc Stock (AMAT) Moved Down by 6.81% on Jul 2: What Investors Need To Know

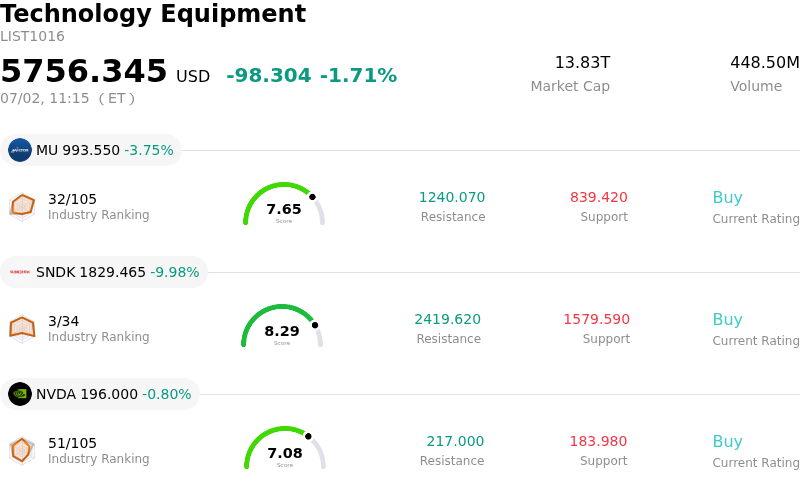

Applied Materials Inc (AMAT) moved down by 6.81%. The Technology Equipment sector is down by 1.71%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 4.27%; SanDisk Corporation (SNDK) down 9.98%; NVIDIA Corp (NVDA) down 0.80%.

What is driving Applied Materials Inc (AMAT)’s stock price down today?

The downward movement and heightened intraday volatility in Applied Materials shares are primarily driven by sector-wide profit-taking and a valuation-driven cooling period across the semiconductor industry. Following an extraordinary rally fueled by the rapid expansion of artificial intelligence infrastructure, the broader chip sector has faced intense scrutiny regarding whether stock valuations have become too expensive relative to near-term returns.

A major catalyst for the current pressure is a cautious shift in market sentiment. Analysts have warned that major semiconductor and equipment stocks had entered extremely overbought territory, leaving them highly vulnerable to a correction. This sentiment was exacerbated by a recent warning from Bank of America regarding rising bubble risks in the broader AI trade. Although demand for advanced AI chips remains fundamentally strong, investors are reassessing the pace of capital spending and potential barriers to near-term AI adoption. Concerns over a possible supply glut and capacity overbuilding by hyperscalers have led to a broader rotation out of high-flying semiconductor names.

In addition to sector-level headwinds, company-specific technical factors and insider activity have weighed heavily on investor confidence. Recent SEC filings revealed notable insider selling at Applied Materials, including significant, multi-million dollar stock liquidations by the Chief Executive Officer and other senior executives into recent strength. Although these transactions do not alter the company's long-term business thesis, the timing and concentration of executive profit-taking have reinforced the market's perception that the stock may be priced for perfection in the short term.

Finally, despite the company's robust fundamentals—such as the recent rollout of a new suite of chipmaking systems targeting high-bandwidth memory and advanced 3D packaging—the market is increasingly focused on execution risks. Applied Materials' management has previously flagged supply chain and parts sourcing constraints as primary operational bottlenecks. With the stock trading at elevated valuation multiples, any potential deceleration in wafer fab equipment spending or supply chain execution delays makes the current share price highly sensitive to negative revisions, triggering the sharp intraday sell-off.

Technical Analysis of Applied Materials Inc (AMAT)

Technically, Applied Materials Inc (AMAT) shows a MACD (12,26,9) value of 14.330, indicating a buy signal. The RSI at 60.363 suggests neutral condition and the Williams %R at 40.388 suggests buy condition. Please monitor closely.

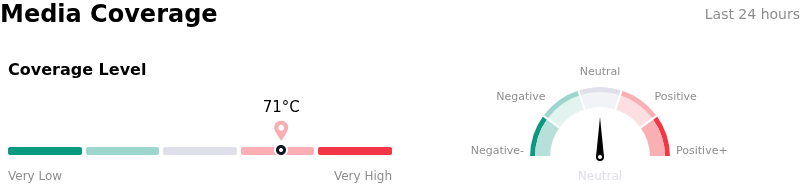

Media Coverage of Applied Materials Inc (AMAT)

In terms of media coverage, Applied Materials Inc (AMAT) shows a coverage score of 71, indicating a high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Applied Materials Inc (AMAT)

Applied Materials Inc (AMAT) is in the Technology Equipment industry. Its latest annual revenue is $28.37B, ranking 10 in the industry. The net profit is $7.00B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $570.07, a high of $900.00, and a low of $308.00.

More details about Applied Materials Inc (AMAT)

Company Specific Risks:

- Extreme Valuation Premium and Price-to-Target Divergence: Following a massive year-to-date rally of over 140%, AMAT is trading at an elevated trailing P/E of approximately 65.2x—more than 220% above its five-year median of 20.4x. With the consensus analyst mean target of $550 sitting roughly 12% below recent trading levels, the stock faces significant risk of severe multiple compression and profit-taking volatility as market expectations outstrip near-term fundamental value.

- Aggressive and Concentrated Insider Liquidations: SEC filings from late June and early July 2026—including a Form 4 filed on July 1, 2026—reveal heavy insider de-risking totaling over $114 million in stock sales over the last three months with zero purchasing activity. This massive selling pressure, led by CEO Gary Dickerson's $42.5 million liquidation and CTO Omkaram Nalamasu's $14.4 million sale, signals that corporate leadership perceives the stock to be near its valuation ceiling.

- Vulnerability to Memory CapEx Moderation and HBM Slowdown: The stock has suffered heightened intraday volatility as markets react to reports that major memory manufacturer SK Hynix is moderating its High-Bandwidth Memory (HBM4) expansion. Because AMAT is heavily exposed to DRAM and advanced packaging tool demand, capital spending pauses or capacity reshuffling among leading Asian chipmakers directly threatens to thin out its high-growth order book.

- Severe Free Cash Flow and Liquidity Contraction: Despite posting robust headline revenues, AMAT's quarterly free cash flow severely contracted year-over-year to just $210 million, vastly missing the institutional consensus expectation of $1.6 billion. This cash drain is driven by mounting working capital requirements to build advanced materials inventory and self-fund highly capital-intensive projects, such as the $500 million Singapore manufacturing facility expansion, severely limiting immediate financial flexibility.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.