Intel Corp Stock (INTC) Moved Down by 8.32% on Jul 1: Key Drivers Unveiled

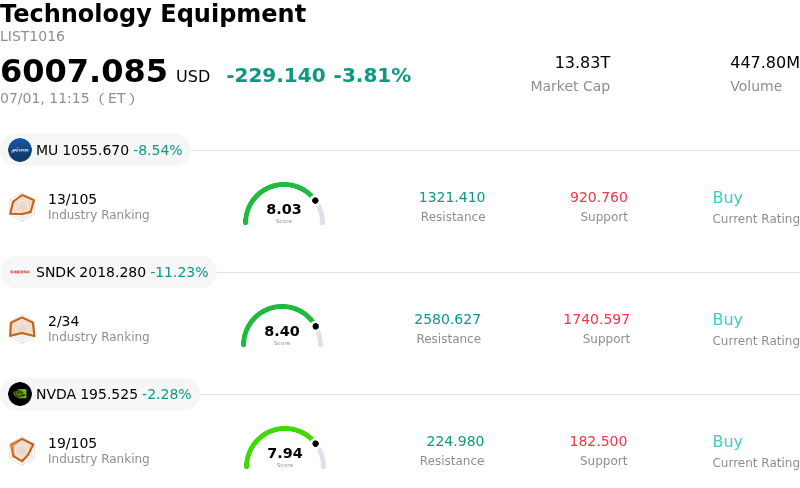

Intel Corp (INTC) moved down by 8.32%. The Technology Equipment sector is down by 3.81%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 9.16%; SanDisk Corporation (SNDK) down 11.23%; NVIDIA Corp (NVDA) down 2.28%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel experienced downward pressure as a wave of profit-taking swept through the semiconductor sector, halting its recent upward momentum. Having recently rallied to a new multi-year high, the chipmaker became highly susceptible to short-term selling pressure. This downward movement reflects growing caution among investors who chose to lock in profits, particularly as the broader market exhibited a more risk-off posture with Nasdaq and S&P 500 futures showing overnight weakness.

The downward correction is further compounded by underlying fundamental anxieties regarding Intel's aggressive manufacturing roadmap and its near-term financial profile. While the company's next-generation 18A-P process node has successfully transitioned into its risk production phase, industry data highlights that current manufacturing yields remain below the threshold required for profitable commercial-scale production. Reaching a profitable yield is not anticipated until late 2026 or 2027, posing ongoing concerns of gross margin dilution and execution setbacks. Ramping up complex nodes is notoriously capital-intensive, and any manufacturing bottlenecks could delay margin recovery, a risk that looms large given the stock's elevated valuation.

This high-expenditure transformation has created a persistent cash drain, forcing the company to rely heavily on debt financing. In addition, despite optimism surrounding AI-related custom-chip partnerships, analysts remain wary of persistent competitive pressures. Intel continues to contend with market share erosion in its core central processing unit business, facing fierce rivalry in both the personal computer and data center landscapes.

Furthermore, some market participants believe that the recent positive catalysts, including speculative foundry agreements and Wall Street analyst upgrades, have already been fully priced into the stock. Given the massive year-to-date run, the bar for financial success is exceptionally high. With the next major catalyst being the second-quarter earnings release on July 23, investors are taking a step back to evaluate whether Intel can deliver concrete foundry contract disclosures and volume commitments to justify its valuation.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of 1.170, indicating a buy signal. The RSI at 63.198 suggests neutral condition and the Williams %R at 7.267 suggests overbought condition. Please monitor closely.

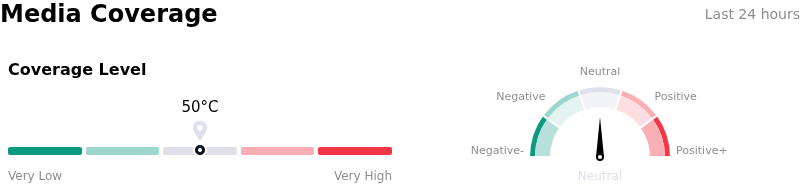

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 50, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $94.77, a high of $160.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Extreme Valuation Multiples and Pullback Vulnerability: Following a massive multi-hundred percent rally over the past year, Intel's stock is trading at historically elevated multiples, leaving it highly vulnerable to short-term downside risks and valuation compression if future data center and foundry performance fails to meet inflated expectations.

- 18A-P Yield and Margin Headwinds: The transition to and scale-up of the next-generation Intel 18A-P manufacturing node presents a substantial risk to near-term profitability, with management actively cautioning that the initial ramp-up will serve as a decent headwind to gross margins due to high development costs and lower early yields.

- Hyperscaler Capital Constraints: Analyst downgrades highlight systemic concerns that massive infrastructure debt and cash flow allocation to chip-buying among major "hyperscale" AI buyers could restrict future capital expenditures, capping Intel's high-end data center chip growth potential.

- Cash Burn and Substantial Debt Obligations: Intel continues to operate in a capital-intensive turnaround phase, reporting significant net losses, heavy capital expenditures, and highly negative free cash flows, which are further pressured by major transactions such as the recent $14.2 billion repurchase of Apollo's stake in Ireland's Fab 34.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.