Taiwan Semiconductor Manufacturing Co Ltd Stock (TSM) Moved Up by 3.02% on Jun 30: What Signal Does It Send?

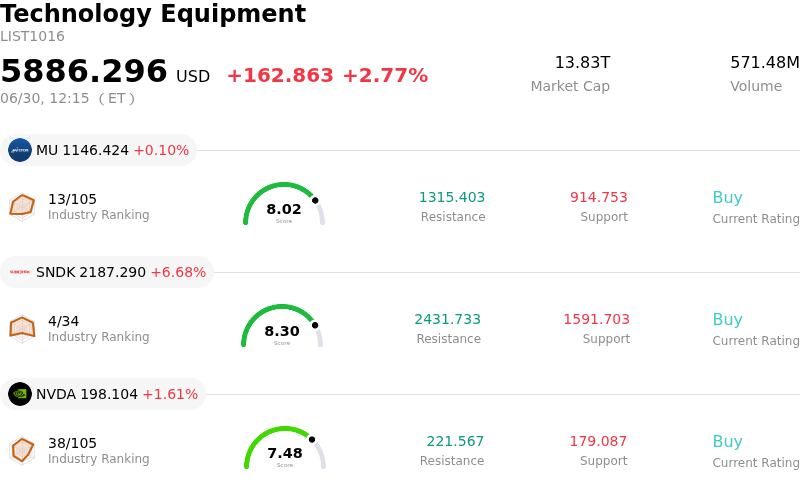

Taiwan Semiconductor Manufacturing Co Ltd (TSM) moved up by 3.02%. The Technology Equipment sector is up by 2.77%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 0.19%; SanDisk Corporation (SNDK) up 6.68%; NVIDIA Corp (NVDA) up 1.66%.

What is driving Taiwan Semiconductor Manufacturing Co Ltd (TSM)’s stock price up today?

The upward movement in Taiwan Semiconductor Manufacturing Company’s (TSM) share price is primarily driven by a wave of bullish analyst upgrades, strong fundamental growth forecasts, and positive developments in the global artificial intelligence chip supply chain.

A major catalyst for the positive sentiment is the aggressive upward revision of price targets and earnings estimates by top-tier investment firms. Morgan Stanley raised its price target for TSM, citing improved revenue and pricing outlooks, while projecting approximately 40% year-on-year revenue growth for the company in 2026. This was closely followed by UBS, which raised its price target and revised TSM's sales growth expectations upward, anticipating sustained long-term demand. Analysts also point out that TSM is well-positioned to implement price increases for its advanced packaging and fabrication technologies by early 2027, further boosting its long-term profit margins.

The underlying business fundamentals remain exceptionally strong, fueled by the relentless build-out of artificial intelligence infrastructure. Management previously guided for full-year revenue growth above 30% in U.S. dollar terms, supported by robust AI accelerator demand that is projected to grow at a high-double-digit compound annual growth rate. The market is also reacting positively to the upcoming second-quarter investor conference scheduled for mid-July, where institutional investors expect the company to raise its capital expenditure forecast toward the upper end of its guidance to support advanced technology nodes.

Operational expansion has further bolstered investor confidence. The company’s newly solidified ten-year partnership with Amkor Technology to expand advanced packaging and testing capacity in Arizona strengthens TSM’s onshore manufacturing footprint in the United States. This geographical diversification helps mitigate geopolitical risks while securing priority access to key customers. While competitor announcements concerning next-generation semiconductor processes have emerged, TSM’s clear roadmap for 1.4-nanometer pilot production and its strong market-share dominance keep it firmly ahead in the high-performance computing sector, reinforcing its status as an indispensable partner to major tech firms.

Technical Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Technically, Taiwan Semiconductor Manufacturing Co Ltd (TSM) shows a MACD (12,26,9) value of -0.597, indicating a neutral signal. The RSI at 58.316 suggests neutral condition and the Williams %R at 30.429 suggests buy condition. Please monitor closely.

Fundamental Analysis of Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Taiwan Semiconductor Manufacturing Co Ltd (TSM) is in the Technology Equipment industry. Its latest annual revenue is $122.22B, ranking 2 in the industry. The net profit is $55.12B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $476.24, a high of $625.00, and a low of $351.00.

More details about Taiwan Semiconductor Manufacturing Co Ltd (TSM)

Company Specific Risks:

- Q2 Revenue Growth Underperformance: Although TSMC posted solid double-digit sales growth, its combined April and May revenue increase of 24% year-over-year fell short of Wall Street's elevated quarterly projections of 35%. This gap, paired with persistent weakness in downstream smartphone and consumer hardware demand, heightens the risk of a near-term revenue miss heading into the company's July 16, 2026 earnings conference.

- High CapEx Commitments and Margin Erosion Risk: TSMC's massive projected 2026 capital expenditure budget of $52 billion to $56 billion to expand advanced sub-3nm nodes exposes the company to severe fixed-cost underutilization and gross margin compression if global demand for AI-related hardware begins to soften or experience a cyclical cooling period.

- Downstream Price Hikes Dampening End-Consumer Demand: Escalating chip and memory manufacturing costs have forced key downstream hardware partners, including Apple, to increase consumer pricing on their latest devices. Institutional analysts are increasingly concerned that these higher retail price points will dampen global consumer electronics demand, leading to a subsequent pullback in wafer order volumes.

- Immediate Patent Dispute and Import Ban Threat: TSMC faces legal pressure from a patent infringement complaint filed with the U.S. International Trade Commission (ITC). With a preliminary ruling expected by the end of June 2026, the company faces the immediate downside risk of a potential U.S. import ban on chips manufactured with key AI-accelerator technologies.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.