Arm Holdings PLC Stock (ARM) Closed Down by 3.48% on Jun 25: Drivers Behind the Movement

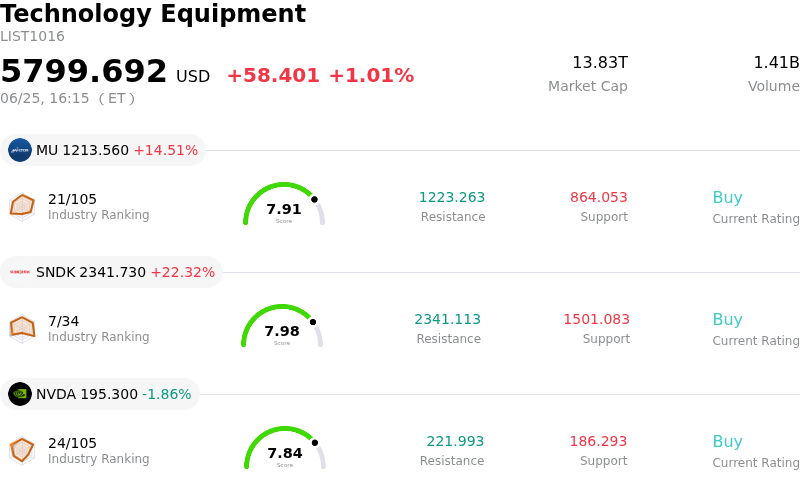

Arm Holdings PLC (ARM) closed down by 3.48%. The Technology Equipment sector is up by 1.01%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 14.51%; SanDisk Corporation (SNDK) up 22.32%; NVIDIA Corp (NVDA) down 1.86%.

What is driving Arm Holdings PLC (ARM)’s stock price down today?

While some chip stocks found support following blowout earnings within the memory sector, Arm Holdings experienced a downward trend as part of a broader consolidation and profit-taking wave. Having been one of the strongest performers in the market this year, the stock faces heavy pressure from investors capitalizing on its massive year-to-date gains. Arm's valuation has become extremely stretched, carrying a triple-digit trailing price-to-earnings multiple. This premium pricing has made the high-beta stock highly vulnerable to market fluctuations and sector de-risking, as investors rotate out of high-flying artificial intelligence names to lock in profits.

Recent institutional actions and analyst sentiment have further amplified this downward momentum. Although some Wall Street brokerages recently raised their price targets on Arm’s long-term potential in AI, a notable downgrade from New Street Research from Buy to Neutral has warned that the stock's rapid run-up has pushed it to an unsustainable premium. Compounding these valuation jitters, recent regulatory filings disclosed substantial insider selling, with multiple senior executives liquidating shares on the open market. This executive activity has triggered caution among institutional investors, raising concerns about a near-term ceiling for the stock.

Underlying operational risks and regulatory headwinds also continue to weigh on investor confidence. Arm’s strategic transition into proprietary hardware—specifically with its newly developed central processing units—creates potential channel conflicts with its core licensing partners, such as Nvidia, Qualcomm, and Apple, who may increasingly view the chip designer as a direct competitor. Additionally, intensifying regulatory and antitrust scrutiny over the company’s licensing practices continues to inject uncertainty into its high-margin business model. Together, these structural concerns and valuation pressures have overshadowed long-term bullish forecasts, driving the stock's downward movement amid heightened intraday volatility.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of -11.072, indicating a neutral signal. The RSI at 52.731 suggests neutral condition and the Williams %R at 60.666 suggests sell condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $281.13, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Severe Valuation Compression and Analyst Downgrades: Following a downgrade by New Street Research from Buy to Neutral citing an unsustainable trailing P/E ratio exceeding 470x, ARM has suffered massive intraday volatility and a steep week-to-date decline of nearly 19% as institutional investors lock in profits and rotate out of richly valued AI names.

- Ecosystem Friction and Channel Conflict: Arm's strategic transition into developing proprietary hardware and custom subsystems—specifically its new 136-core AGI CPU—creates a direct conflict of interest with its key licensing partners, such as Nvidia, Qualcomm, Apple, and AWS, who may increasingly view Arm as a hardware competitor rather than a neutral intellectual property supplier.

- Compounding Regulatory and Legal Headwinds: The company faces intensifying regulatory scrutiny, including an active Federal Trade Commission (FTC) probe examining potential monopolistic behavior in licensing terms, alongside the highly anticipated Qualcomm/Nuvia contract litigation set for late 2026, which analysts warn could trigger a severe downward de-rating if decided unfavorably.

- Margin Compression and Scaling Execution Risks: Arm's operating margins have compressed from 52.8% to 49.1% due to a 43% surge in R&D expenses ($1.911 billion) to support its standalone CPU roadmap. Because this internal CPU business is not projected to generate material revenue until fiscal 2028, any execution delays represent a major financial vulnerability.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.