KLA Corp Stock (KLAC) Moved Down by 9.85% on Jun 23: Facts Behind the Movement

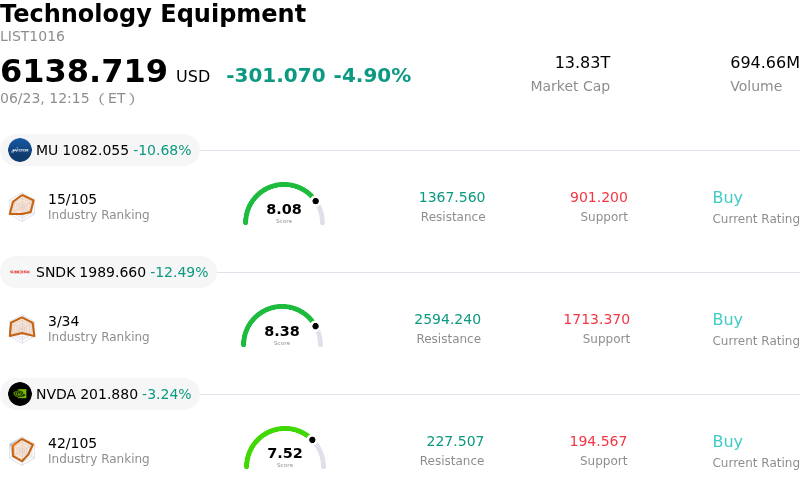

KLA Corp (KLAC) moved down by 9.85%. The Technology Equipment sector is down by 4.90%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 10.68%; SanDisk Corporation (SNDK) down 12.49%; NVIDIA Corp (NVDA) down 3.29%.

What is driving KLA Corp (KLAC)’s stock price down today?

The significant downward pressure on KLA Corporation today is primarily driven by a severe, global technology sell-off that has triggered a broad repricing across the semiconductor and chip equipment sectors. This market correction originated overnight in Asian markets, with major South Korean chipmakers suffering steep losses, before propagating through European tech indices and ultimately hitting Wall Street. As major benchmarks like the Nasdaq Composite and S&P 500 fell, chip-equipment heavyweights were swept up in the sector-wide risk-off sentiment, leading to synchronized declines among KLA’s direct peers, including Applied Materials and Lam Research.

This macro-driven pullback has amplified several pre-existing, company-specific vulnerabilities for KLA, most notably its stretched valuation. Following a highly anticipated ten-for-one forward stock split earlier in the month, the stock embarked on a major vertical run-up that pushed its trailing price-to-earnings multiple to more than double its five-year median. This high premium left the stock with little fundamental cushion. With the average analyst price target sitting below recent peak trading levels, institutional investors and traders increasingly viewed the equity as overextended, prompting rapid profit-taking as broader market conditions deteriorated.

Negative technical and operational factors have further compounded the selling pressure. Recent regulatory disclosures revealing substantial insider selling, led by Chief Executive Officer Richard Wallace liquidating a multi-million-dollar portion of his equity, have raised concerns regarding the sustainability of the stock's post-split valuation. Furthermore, persistent geopolitical risks remain a major overhang. Strict government export controls targeting semiconductor technology shipments to China are projected to result in a substantial drag on KLA's top-line growth, costing the company hundreds of millions of dollars in forfeited revenue for the year. The combination of these structural challenges, elevated multiples, and a coordinated global sector rotation has ultimately driven today's sharp intraday volatility.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of -353.897, indicating a sell signal. The RSI at 20.053 suggests sell condition and the Williams %R at 97.671 suggests oversold condition. Please monitor closely.

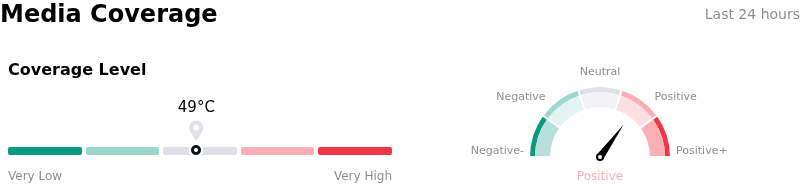

Media Coverage of KLA Corp (KLAC)

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $196.47, a high of $290.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- Extreme Post-Split Valuation Premium: Following its 10-for-1 stock split, KLAC's trailing P/E multiple expanded to over 67x and its forward P/E surpassed 52x—substantially above its five-year historical median of 26x—prompting analyst warnings of overstretched multiples and sparking defensive profit-taking.

- Input Cost Pressures and Gross Margin Contraction: Management projects a negative impact of approximately 100 basis points on gross margins. This compression is driven by soaring memory component costs required for the high-performance computers inside KLA's inspection tools, which the company is currently unable to pass down to customers.

- Aggressive Executive Divestments: SEC filings showing high-profile insider selling, highlighted by CEO Richard Wallace liquidating approximately $10 million in stock (45,120 shares), have amplified institutional concerns regarding the sustainability of current valuation levels.

- Geopolitical and China Export Restraints: Strict federal export control policies on advanced semiconductor technology shipments to China continue to limit top-line growth, creating regulatory friction projected to cost the company an estimated $300 million to $350 million in forfeited revenue for the year.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.