Lam Research Corp Stock (LRCX) Moved Down by 9.90% on Jun 23: Facts Behind the Movement

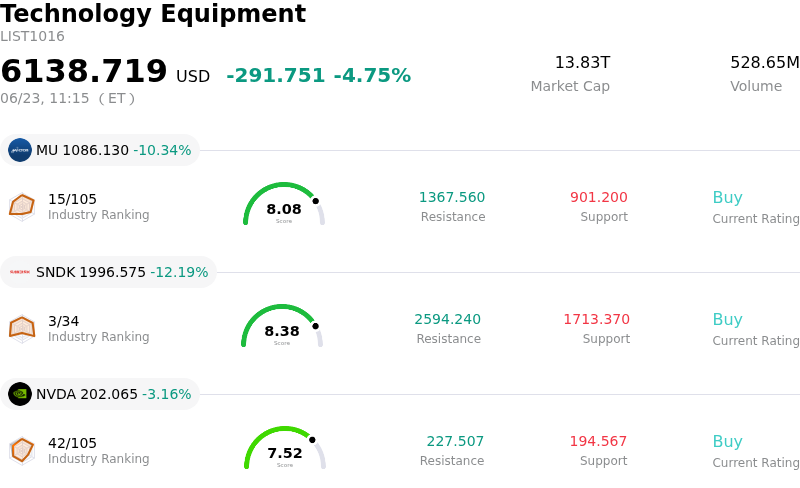

Lam Research Corp (LRCX) moved down by 9.90%. The Technology Equipment sector is down by 4.75%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 10.34%; SanDisk Corporation (SNDK) down 12.19%; NVIDIA Corp (NVDA) down 3.16%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

A massive wave of profit-taking and a coordinated global sell-off in semiconductor equities are the primary drivers behind the sharp downward movement in Lam Research. The sell-off intensified in Asian markets, where South Korea's benchmark Kospi index plunged, triggering trading halts as major chipmakers and key Lam Research customers, Samsung Electronics and SK Hynix, experienced severe declines. This regional panic quickly crossed over to U.S. markets, dragging down major semiconductor equipment suppliers and memory producers as investors reassessed risk across the entire artificial intelligence infrastructure value chain.

Stretched valuations have exacerbated the downward pressure on Lam Research's stock. Following a monumental year-to-date rally fueled by optimism over next-generation wafer fabrication equipment demand, the company's valuation multiple expanded to levels far exceeding historical norms. Trading at a highly elevated price-to-earnings ratio relative to its five-year median, the stock left little margin of safety for investors. Despite recent aggressive price-target upgrades from Wall Street institutions, market participants have opted to secure profits, recognizing that much of the projected long-term AI-driven growth has already been priced into current equity valuations.

Macroeconomic anxieties and policy developments have further dampened investor sentiment. Rising Treasury yields and mounting concerns that the Federal Reserve may keep interest rates elevated to curb inflation have pressured high-multiple technology growth stocks. This is compounded by persistent geopolitical and regulatory overhangs. Investors remain highly sensitive to potential tighter global export controls on semiconductor shipments, which directly threaten the company's substantial revenue exposure in Chinese logic and memory markets. Additionally, localized supply chain risks, such as potential helium supply disruptions stemming from Middle East conflicts, have fueled fears of slowing fab operations for key customers.

Beneath the market volatility, subtle operational signals are also prompting caution. While the company recently raised its global wafer-fabrication equipment market outlook to one hundred and forty billion dollars on strong advanced packaging momentum, a decline in customer down payments to multi-year lows has signaled a potential near-term cyclical cooling in memory capital commitments. This confluence of overstretched multiples, regional hardware sector distress, macro policy headwinds, and underlying customer dynamics has culminated in a substantial correction, erasing several sessions of recent gains.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 10.740, indicating a buy signal. The RSI at 72.195 suggests buy condition and the Williams %R at 0.196 suggests overbought condition. Please monitor closely.

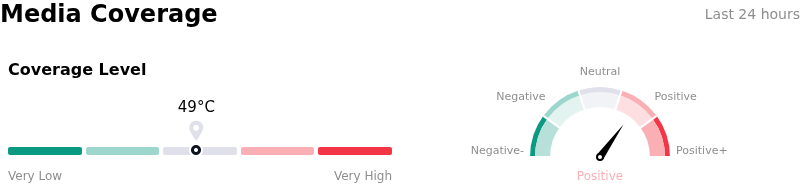

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $332.58, a high of $450.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Extreme Valuation Stretch and Intraday Volatility: Following a massive year-to-date rally of over 115% that pushed LRCX's trailing P/E past 69x and forward P/E over 47x, the stock plummeted by as much as 10.8% intraday on June 23, 2026, demonstrating severe vulnerability to sudden profit-taking and multiple compression as the price has stretched far beyond historical averages.

- China Revenue Concentration and Falling Customer Down Payments: While China accounts for 34% to 35% of total revenue, management has guided for sequential declines in this region, compounded by customer down payments hitting their lowest levels in nearly four years—a metric heavily correlated with Chinese clients—exposing the company to sharp top-line deceleration.

- Material Insider Selling: SEC Form 4 filings disclosing that Director Eric Brandt divested 54,500 shares in open-market transactions totaling over $19.1 million—representing a 21.48% decrease in his direct holdings—have exacerbated investor anxieties regarding high-level net selling at a near-term valuation peak.

- Drastic Projected Deceleration in System Shipment Growth: Institutional analysts have flagged structural concerns regarding a steep projected drop in system shipment growth to just 3% in 2026 from 82% in 2025, driven by an expected cyclical cooling in both the 3D NAND memory and Chinese mature-logic nodes.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.