ASML Holding NV Stock (ASML) Moved Down by 7.60% on Jun 23: What Investors Need To Know

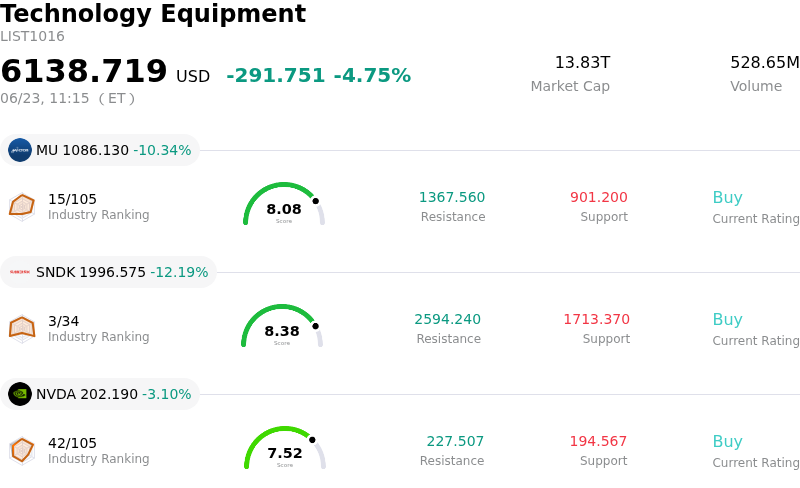

ASML Holding NV (ASML) moved down by 7.60%. The Technology Equipment sector is down by 4.75%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 10.34%; SanDisk Corporation (SNDK) down 12.19%; NVIDIA Corp (NVDA) down 3.16%.

What is driving ASML Holding NV (ASML)’s stock price down today?

The downward movement in ASML Holding N.V. is primarily driven by a broader selloff in the semiconductor sector, rather than any sudden operational failure. As a key enabler of advanced artificial intelligence hardware, ASML is highly susceptible to macroeconomic swings. Growing concerns over rising interest rates and elevated valuations across high-growth technology equities have spurred a general de-risking phase. With inflation data on the horizon, investors are rotating out of high-beta tech names that had been trading at historical premiums, pushing the entire chip equipment sector into a defensive posture.

In addition to macro headwinds, intensifying geopolitical tensions and tighter regulatory oversight regarding China-bound exports remain a significant overhang. Recent events highlighted this regulatory spotlight, including discussions surrounding the MATCH Act in the United States, which could potentially expand export bans to include less advanced deep ultraviolet lithography systems and restrict ASML from servicing its substantial installed machine base in China. With the Chinese market contributing a sizable portion of ASML's projected annual revenue, any threat to high-margin recurring service contracts heightens risk profiles. This regulatory friction is underscored by the Netherlands officially joining the U.S.-led Pax Silica initiative to coordinate AI supply chains, amplifying investor anxiety over future export policies.

Furthermore, undercurrents of cautious customer behavior are impacting investor sentiment. While long-term demand for artificial intelligence infrastructure remains robust, leading foundries and memory chipmakers have shown a degree of conservatism regarding the immediate, high-volume deployment of next-generation High-NA EUV systems. Major customers are prioritizing less capital-intensive advanced packaging alternatives in the near term over immediate capital expenditure upgrades. This slower backlog monetization, coupled with ASML's intensive working capital requirements and rigid cost structures, has put pressure on the firm's free cash flow, making the stock's premium valuation vulnerable to correction during periods of market volatility.

Technical Analysis of ASML Holding NV (ASML)

Technically, ASML Holding NV (ASML) shows a MACD (12,26,9) value of 24.585, indicating a buy signal. The RSI at 65.661 suggests neutral condition and the Williams %R at 9.290 suggests overbought condition. Please monitor closely.

Fundamental Analysis of ASML Holding NV (ASML)

ASML Holding NV (ASML) is in the Technology Equipment industry. Its latest annual revenue is $36.83B, ranking 7 in the industry. The net profit is $10.83B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1743.10, a high of $2345.00, and a low of $994.01.

More details about ASML Holding NV (ASML)

Company Specific Risks:

- Geopolitical Friction and EUV Export Scrutiny: On June 19, 2026, reports surfaced that US Commerce Secretary Howard Lutnick confronted ASML executives over concerns that restricted Extreme Ultraviolet (EUV) lithography machines or specialized transport components may have slipped into China. Although ASML issued a formal denial on June 23, 2026, stating it has never shipped EUV tools to China, the incident has intensified regulatory scrutiny and sparked fears of tighter multilateral export curbs on deep ultraviolet (DUV) equipment. This poses an immediate threat to ASML’s top-line guidance, as China is expected to represent roughly 20% of its projected 2026 revenues.

- Extreme Valuation Premium and Market De-Risking: Amid a broad semiconductor and Big Tech selloff on June 23, 2026, ASML shares fell more than 6% on interest rate fears and growing AI-spending skepticism. Trading at a premium valuation of over 51x forward earnings—which exceeds its estimated fair value and sits above the €1,573 analyst consensus target—the stock is highly susceptible to severe intraday drawdowns and rapid multiple compression when market sentiment shifts risk-off.

- Customer Adoption Delays for High-NA EUV Systems: Major semiconductor foundry and memory manufacturers, including Taiwan Semiconductor Manufacturing Co. (TSMC), have signaled delays in deploying ASML’s next-generation, high-volume High-NA EUV systems. Rather than committing to immediate, highly capital-intensive upgrades of the €350–400 million machines, clients are prioritizing less expensive advanced packaging alternatives, which risks slowing down the monetization of ASML's backlog.

- Severe Working Capital Pressures and Rigid Overhead: ASML faces immediate cash flow constraints, highlighted by a deep negative free cash flow of -$3.08 billion in early 2026 due to intensive working capital demands and complex equipment shipping timelines. The financial drag is worsened by a rigid cost structure and a union-backed labor agreement that bans forced layoffs until May 2027, preventing management from quickly optimizing overhead or scaling down operations during localized demand slowdowns.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.