Lam Research Corp Stock (LRCX) Closed Up by 5.14% on Jun 22: A Full Analysis

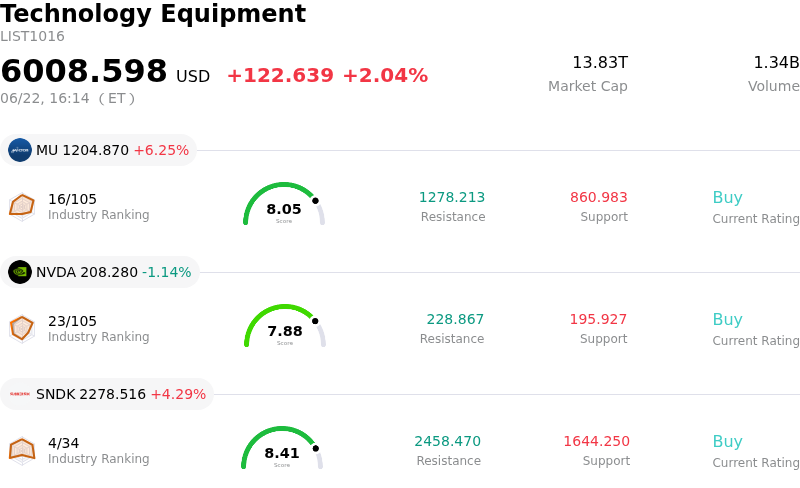

Lam Research Corp (LRCX) closed up by 5.14%. The Technology Equipment sector is up by 2.04%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 6.25%; NVIDIA Corp (NVDA) down 1.14%; SanDisk Corporation (SNDK) up 4.29%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research experienced a strong upward move driven by a positive revision of industry growth forecasts and bullish analyst commentary. Specifically, Wells Fargo aggressively raised its price target for the company while maintaining an Overweight rating. This upward adjustment was supported by a broader lifting of the firm's global Wafer Fab Equipment industry spending forecast for both 2027 and 2028. The revised outlook underscores robust and accelerating demand for specialized manufacturing tools, providing strong visibility for long-term semiconductor equipment capital expenditure.

A primary structural driver behind the positive momentum is the ongoing expansion of artificial intelligence infrastructure and advanced packaging technologies. As chipmakers accelerate the deployment of high-performance computing systems, demand is spiking for advanced wafer fabrication equipment capable of producing complex chip designs and high-bandwidth memory. Lam Research is uniquely positioned as a leading provider of advanced etch and deposition tools, which are critical for building complex structures in logic and memory chips. The market's optimism is further reinforced by expectations that persistent memory supply constraints will extend well into the future, forcing major semiconductor manufacturers to sustain high levels of capital investment.

This constructive fundamental outlook builds upon the company’s strong financial execution. Recent quarterly earnings outperformed expectations with impressive revenue and earnings per share beats, alongside an optimistic forward guidance that surprised the market. Despite these strengths, the stock has shown notable intraday volatility, reflecting a market that is actively balancing long-term momentum against valuation concerns. Stretched valuation multiples relative to historical averages, along with geographical risks such as concentration in China and potential export restrictions, continue to keep trading active and volatile. However, on this trading day, the overarching sentiment was dominated by structural growth opportunities in AI and positive analyst revisions, driving the stock higher.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of 8.446, indicating a buy signal. The RSI at 68.591 suggests neutral condition and the Williams %R at 12.172 suggests overbought condition. Please monitor closely.

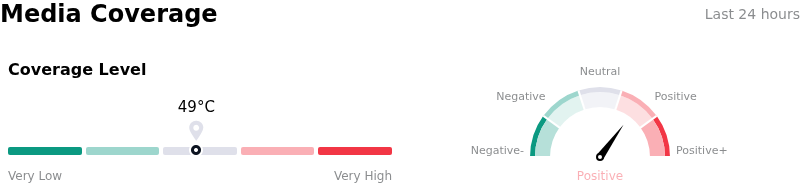

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $332.58, a high of $450.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Geopolitical and Export Control Exposure in China: China accounts for approximately 34% to 35% of Lam Research's total revenue, leaving the company highly vulnerable to severe top-line volatility. Recent reports indicating that the U.S. Department of Commerce is restricting equipment shipments to Chinese semiconductor manufacturer Hua Hong highlight the immediate threat of expanding export controls and potential market share impairment in the region.

- Drastic Deceleration in System Shipment Growth: Analysts maintain structural concerns regarding a projected drop in system shipment growth to just 3% in 2026, down from 82% in 2025. This steep deceleration is driven by expected cyclical cooling in both the NAND memory and Chinese logic markets, threatening sustained top-line expansion.

- Stretched Valuation and Multiple Compression: Due to massive AI infrastructure momentum, the stock's trailing P/E ratio has surged past 72x, vastly exceeding its five-year historical median of 23x. Trading approximately 16% above its consensus analyst price target, the stock is highly vulnerable to multiple compression and sharp profit-taking during tech-sector consolidations.

- Significant Insider Divestment: Market anxieties are compounding around heavy insider net-selling, with $47.7 million in shares divested over the last three months. This trend is highlighted by SEC Form 4 filings showing Director Eric Brandt's open-market divestment of 54,500 shares totaling over $19.1 million, signaling potential near-term valuation peaks to institutional investors.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.