Vertiv Holdings Co Stock (VRT) Moved Up by 4.90% on Jun 21: A Full Analysis

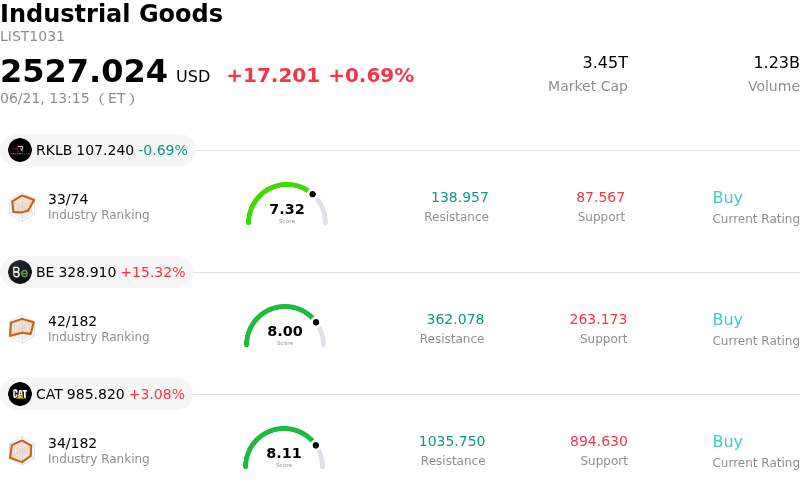

Vertiv Holdings Co (VRT) moved up by 4.90%. The Industrial Goods sector is up by 0.69%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Rocket Lab USA Inc (RKLB) down 0.69%; Bloom Energy Corp (BE) up 15.32%; Caterpillar Inc (CAT) up 3.08%.

What is driving Vertiv Holdings Co (VRT)’s stock price up today?

Vertiv Holdings Co experienced positive upward momentum alongside notable intraday volatility, driven by robust sector demand, strategic acquisitions, and a technical recovery from a recent market-wide pullback. As a crucial provider of critical power and cooling infrastructure, the company continues to benefit from the accelerating secular buildout of high-density artificial intelligence data centers, where massive GPU workloads demand increasingly sophisticated thermal management solutions.

A primary catalyst for the recent gains is the company's recent completion of its ThermoKey acquisition. This acquisition expands the company's heat rejection and heat-exchange technology portfolio, notably enhancing its manufacturing capacity in the Europe, Middle East, and Africa region. By integrating ThermoKey's technology, the company is better positioned to address its massive backlog, which has reached approximately fifteen billion dollars. This follows the earlier closing of the Strategic Thermal Labs acquisition, further demonstrating an aggressive expansion into advanced liquid-cooling engineering.

Furthermore, operational and product developments have supported investor optimism. The company recently introduced its fluid management service designed to minimize water usage during the commissioning of high-density liquid cooling projects, addressing environmental and regulatory hurdles for hyperscale data centers. Additionally, its collaboration with NVIDIA on digital twin simulation for AI factories, along with a recently declared quarterly cash dividend, has reinforced positive long-term momentum among both growth and income-focused institutional investors.

The stock’s intraday volatility, however, reflects a broader tension between stellar underlying business fundamentals and a premium valuation. Earlier in the month, the stock underwent a significant macro-driven pullback, dropping from its mid-May highs due to sector rotation and shifting sentiment around artificial intelligence capital expenditure. This pullback presented a buying opportunity for fundamental investors, as the underlying business remains strong, evidenced by a high book-to-bill ratio and robust full-year earnings guidance.

Nonetheless, trading at a high multiple of trailing earnings with a high beta, the equity remains sensitive to broader market swings. Concerns regarding geographic execution risks—specifically surrounding recent growth deceleration in certain international markets—and the operational integration of new acquisitions continue to trigger rapid intraday price swings. Ultimately, while valuation premium and macro sensitivities fuel trading volatility, the company's central role in the physical AI infrastructure chain and its expanding thermal capabilities continue to attract strong institutional demand.

Technical Analysis of Vertiv Holdings Co (VRT)

Technically, Vertiv Holdings Co (VRT) shows a MACD (12,26,9) value of 2.647, indicating a neutral signal. The RSI at 56.646 suggests neutral condition and the Williams %R at 17.329 suggests overbought condition. Please monitor closely.

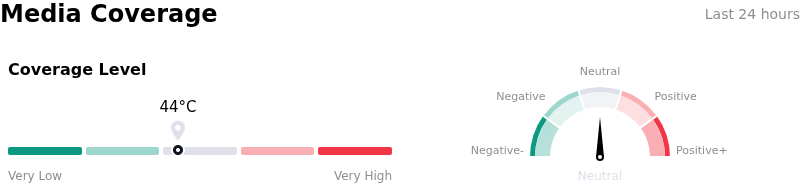

Media Coverage of Vertiv Holdings Co (VRT)

In terms of media coverage, Vertiv Holdings Co (VRT) shows a coverage score of 44, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Vertiv Holdings Co (VRT)

Vertiv Holdings Co (VRT) is in the Industrial Goods industry. Its latest annual revenue is $10.23B, ranking 17 in the industry. The net profit is $1.33B, ranking 13 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $369.90, a high of $500.00, and a low of $188.00.

More details about Vertiv Holdings Co (VRT)

Company Specific Risks:

- Severe Regional Growth Deceleration in EMEA: Vertiv's Europe, Middle East, and Africa (EMEA) segment has experienced a sharp 20.3% year-over-year revenue contraction, with organic sales plunging 29.4%. Achieving full-year 2026 targets remains highly dependent on a projected second-half regional recovery, creating a major geographic execution vulnerability if market stabilization fails.

- Integration Hurdles of the ThermoKey Acquisition: Following the official close of the ThermoKey S.p.A. transaction disclosed in an 8-K filing, the company faces immediate operational and supply chain integration challenges. Absorbing the Italian heat-exchange manufacturer's physical facilities and proprietary liquid-cooling technology into Vertiv's global footprint exposes the company to near-term capital expenditure overhead and execution risks.

- Extreme Valuation and Hyperscaler CapEx Sensitivity: Trading at a premium multiple of approximately 75x to 83x trailing earnings with a high beta of 2.04, the stock has priced in years of perfect execution. This complete lack of a margin of safety makes the share price highly vulnerable to rapid multiple compression if there is any projected cooling, delays, or spending deceleration in AI data-center infrastructure budgets by major hyperscale cloud operators.

- Operational Bottlenecks in Backlog Execution: While carrying a massive $15.0 billion backlog provides strong forward visibility, converting these orders into recognized revenue requires rapid and aggressive global manufacturing capacity expansion. This rapid scaling poses execution risks, potential supply chain bottlenecks, and significant capital expenditure requirements as the company rushes to meet the volume demands of high-density cooling systems.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.