Arm Holdings PLC Stock (ARM) Moved Up by 3.62% on Jun 15: Key Drivers Unveiled

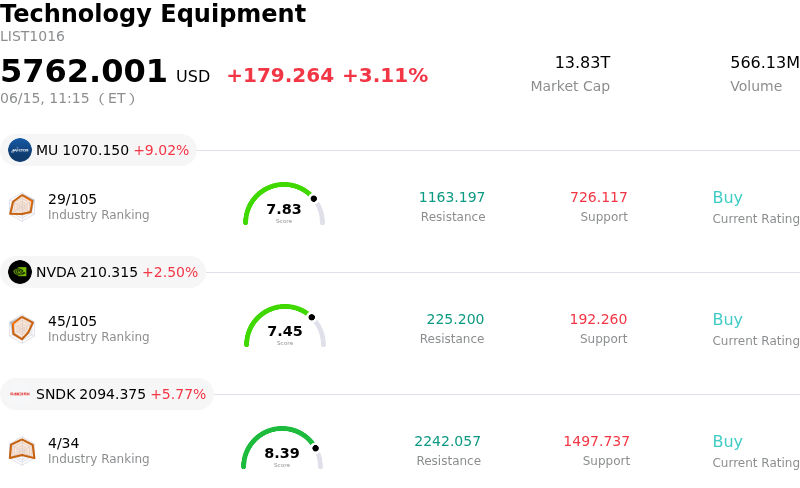

Arm Holdings PLC (ARM) moved up by 3.62%. The Technology Equipment sector is up by 3.11%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 9.02%; NVIDIA Corp (NVDA) up 2.50%; SanDisk Corporation (SNDK) up 5.77%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

Arm Holdings is experiencing an upward movement today, driven primarily by continued positive sentiment surrounding its integral role in the rapidly expanding artificial intelligence (AI) infrastructure market. Recent upgrades in analyst price targets have provided significant tailwinds, with multiple Wall Street firms reinforcing a bullish outlook and highlighting strong demand for agentic AI and data center CPUs. For instance, Bank of America recently raised its price target for the company. This positive re-evaluation by analysts is a key factor in the stock's performance.

The company's strong financial performance, as evidenced by its record Q4 fiscal 2026 earnings, continues to support investor confidence. Arm reported substantial year-over-year revenue growth, with licensing revenue and data center royalties showing particularly robust increases. The CEO's remarks about the company potentially reaching its $15 billion in-house chip sales target ahead of schedule due to overwhelming demand from the AI sector have also fueled investor enthusiasm. This underscores Arm's strategic positioning at the intersection of several powerful secular trends, including AI infrastructure and data center expansion.

Despite the overall positive trajectory, significant intraday volatility suggests investors are also factoring in certain risks. Concerns about the company's elevated valuation are present, with some analyses indicating the stock may be significantly overvalued after its substantial rally. Additionally, reports of an FTC investigation into Arm's licensing practices could be contributing to market uncertainty. Supply chain constraints within the broader semiconductor industry, particularly concerning wafer, memory, and packaging capacity, also represent a potential headwind that could temper near-term growth, even amidst strong demand for Arm's datacenter chips.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [39.06], indicating a neutral signal. The RSI at 63.81 suggests neutral condition and the Williams %R at -36.40 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $258.98, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- An ongoing U.S. Federal Trade Commission (FTC) antitrust investigation introduces significant regulatory and legal risk regarding Arm's chip licensing practices, with concerns that the company might disadvantage rivals as it expands into designing its own chips.

- Recent substantial open-market share sales by multiple top executives, including the Chief Accounting Officer on June 2, 2026, and the Chief Commercial Officer in late May and early June 2026, may signal a lack of confidence in the company's future outlook and contribute to negative sentiment.

- Arm's strategic shift into direct chip manufacturing with its AGI CPU poses a risk of alienating long-standing intellectual property licensees, potentially leading to customer defection and increased competition from alternative architectures.

- The company continues to face premium valuation concerns, with analyses indicating overvaluation based on its current forward P/E ratio, which could lead to significant volatility if growth expectations are not met.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.