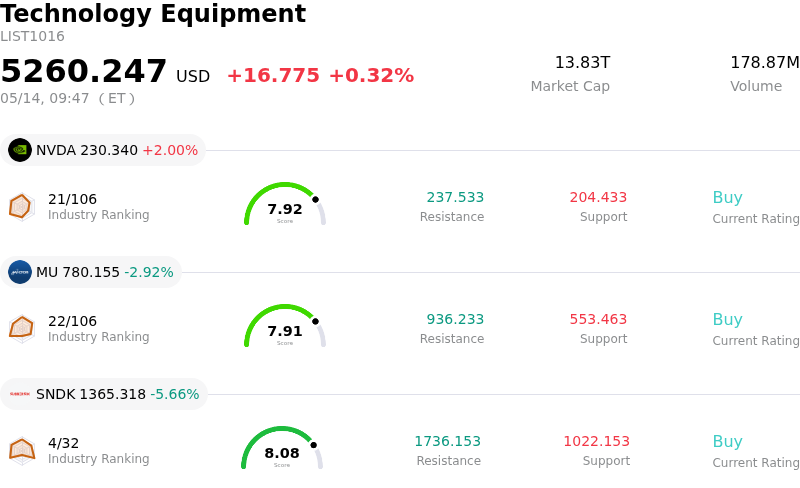

Intel Corp Stock (INTC) Opened Down by 5.21% on May 14: Drivers Behind the Movement

Intel Corp (INTC) opened down by 5.21%. The Technology Equipment sector is up by 0.32%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 2.00%; Micron Technology Inc (MU) down 2.92%; SanDisk Corporation (SNDK) down 5.66%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel experienced a notable intraday downturn, influenced by a convergence of several factors. A primary catalyst appears to be recent analyst commentary and adjustments to ratings, which have introduced caution into the market regarding the company's outlook. HSBC, for instance, downgraded the stock, expressing concerns that its prior significant rally was fueled by one-off deals rather than sustainable improvements in its fundamental operations, particularly highlighting ongoing challenges within the foundry business. Other institutions also maintained cautious ratings, citing lower-than-expected yields on advanced process nodes and a lack of substantial external foundry customer wins.

This cautious analyst sentiment coincided with a reassessment of the stock's valuation following an extended period of considerable gains. Technical indicators suggested the stock was in overbought territory, prompting investors to engage in profit-taking. The discrepancy between the stock's market valuation and the consensus analyst price targets further underscored concerns about potential overvaluation.

Persistent issues within the company's foundry division continued to weigh on investor confidence. The foundry segment reported significant operating losses in the first quarter of 2026 and faced difficulties securing meaningful external customers at scale, despite strategic initiatives. Reports of lower-than-anticipated yields and potential delays for advanced manufacturing processes, such as Panther Lake and 18A, added to the skepticism surrounding the long-term profitability and competitiveness of this key strategic area.

Broader macroeconomic data also contributed to the negative sentiment. A higher-than-expected inflation report for April created uncertainty in the market regarding the Federal Reserve's monetary policy path. This broader concern about persistent inflation dampened expectations for future interest rate reductions, which in turn affected the entire semiconductor sector, including demand for AI infrastructure investment. Additionally, the company is grappling with internal and external supply constraints for critical components, which could hinder its ability to capitalize on demand. This confluence of company-specific challenges, valuation scrutiny, and macroeconomic headwinds likely drove the stock's downward movement.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of [14.51], indicating a buy signal. The RSI at 74.77 suggests buy condition and the Williams %R at -23.45 suggests oversold condition. Please monitor closely.

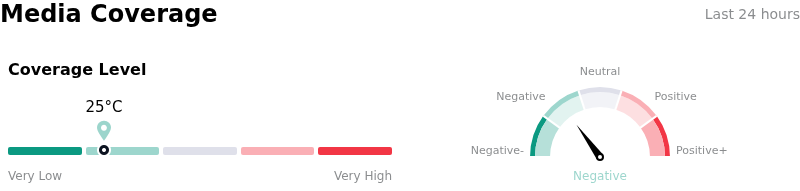

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 25, indicating a low level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $83.42, a high of $124.00, and a low of $20.40.

More details about Intel Corp (INTC)

Company Specific Risks:

- Intel's Foundry division continues to incur substantial operating losses, reporting a $2.3 billion loss in Q1 2026, with analysts expressing concerns over lower-than-expected yields on its advanced 18A and 14A process nodes, hindering its path to profitability and external customer acquisition.

- Intel is experiencing ongoing market share erosion in the crucial server CPU segment, with AMD and ARM continuing to gain significant ground at Intel's expense in Q1 2026.

- Weakening demand in the traditional PC market poses a risk, highlighted by a reported 27% month-over-month decline in April notebook shipments, directly impacting Intel's revenue streams due to its significant reliance on client computing.

- The company faces an increased debt burden and refinancing risk following its $14.2 billion repurchase of a 49% equity interest in the Fab 34 joint venture, partly financed by a $6.5 billion bridge loan that Intel intends to refinance, contributing to credit rating downgrades and a projected high debt-to-EBITDA ratio.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.