Synopsys Inc Stock (SNPS) Moved Up by 9.43% on Apr 24: What Investors Need To Know

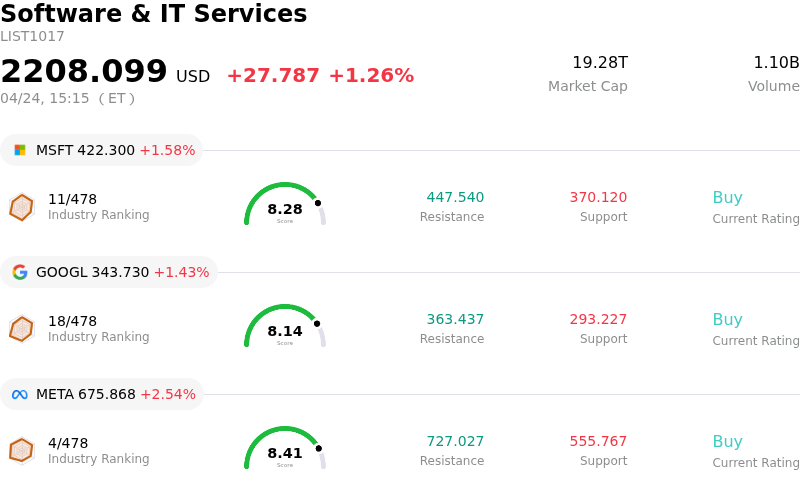

Synopsys Inc (SNPS) moved up by 9.43%. The Software & IT Services sector is up by 1.26%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 1.58%; Alphabet Inc Class A (GOOGL) up 1.43%; Meta Platforms Inc (META) up 2.54%.

What is driving Synopsys Inc (SNPS)’s stock price up today?

Synopsys (SNPS) experienced significant positive intraday volatility today, with its stock demonstrating a substantial upward movement. This notable increase appears to be driven primarily by recent company announcements related to strategic partnerships and advancements in its core technologies, particularly within the burgeoning artificial intelligence (AI) and semiconductor sectors.

A key factor contributing to today's share price appreciation is Synopsys' expanded collaboration with TSMC, announced on April 22, 2026. This partnership focuses on powering next-generation AI systems through silicon-proven intellectual property (IP) and certified electronic design automation (EDA) flows across TSMC's most advanced process and packaging technology nodes, including the 3nm, 2nm, A16, and A14 families. The announcement highlighted major advancements in silicon-proven IP, AI-powered EDA flows, and system-level enablement, with milestones such as PCIe 7.0, HBM4, and M-PHY v6.0 IP on TSMC's advanced nodes. This strategic alliance positions Synopsys strongly to capitalize on the increasing demand for advanced chip design crucial for AI and high-performance computing, signaling robust future revenue streams.

Furthermore, Synopsys announced an extended collaboration with Atomera on April 23, 2026, to advance gallium nitride (GaN) device modeling for radio frequency (RF) and power semiconductor applications. This partnership leverages Synopsys' Sentaurus TCAD tools to develop GaN calibration methodologies and create calibrated TCAD decks, aiming to bring higher-quality GaN solutions to market. Such technological advancements are critical for driving innovation in high-value semiconductor markets.

Adding to the positive sentiment, on April 14, 2026, Synopsys was selected by NASA to support the Artemis program, specifically for spacesuit charging analysis and lunar communications validation using its digital twin and electromagnetic simulation tools. This high-profile collaboration demonstrates the advanced capabilities and reliability of Synopsys' engineering solutions, extending its market reach into specialized, high-growth sectors.

While analyst ratings on SNPS show a mixed consensus of "Hold" with an average price target that suggests potential upside, the recent news regarding strategic technological partnerships and significant project wins likely outweigh these mixed ratings in the short term. The positive financial data from Synopsys' last quarterly earnings report, where it beat analyst expectations for both EPS and revenue and provided strong FY 2026 guidance, also underpins investor confidence. The combination of these favorable developments suggests that the market is reacting positively to Synopsys' strategic positioning and execution in key technological areas.

Technical Analysis of Synopsys Inc (SNPS)

Technically, Synopsys Inc (SNPS) shows a MACD (12,26,9) value of [3.95], indicating a buy signal. The RSI at 60.40 suggests neutral condition and the Williams %R at -25.38 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Synopsys Inc (SNPS)

Synopsys Inc (SNPS) is in the Software & IT Services industry. Its latest annual revenue is $7.05B, ranking 48 in the industry. The net profit is $1.33B, ranking 39 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $533.97, a high of $650.00, and a low of $403.85.

More details about Synopsys Inc (SNPS)

Company Specific Risks:

- Kuehn Law announced an investigation on April 22, 2026, into Synopsys's officers and directors for alleged breaches of fiduciary duties, claiming the company misrepresented or failed to disclose that its increasing focus on AI customers was weakening its Design IP business.

- Analyst reports indicate an ongoing consensus "Hold" rating for the stock, with concerns about a lack of full-year 2026 catalysts and muted growth prospects in the Design IP segment as resources are reallocated towards artificial intelligence opportunities.

- The company faces continued headwinds from geopolitical risks and customer uncertainty, which analysts anticipate will impact the Design IP segment's performance through fiscal year 2026.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.