ServiceNow Inc Stock (NOW) Moved Up by 5.34% on Apr 24: Key Drivers Unveiled

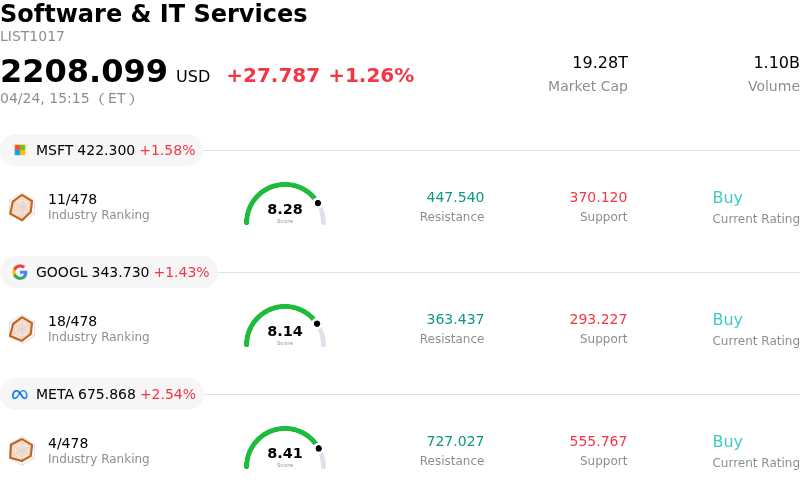

ServiceNow Inc (NOW) moved up by 5.34%. The Software & IT Services sector is up by 1.26%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 1.58%; Alphabet Inc Class A (GOOGL) up 1.43%; Meta Platforms Inc (META) up 2.54%.

What is driving ServiceNow Inc (NOW)’s stock price up today?

ServiceNow (NOW) experienced a notable upward movement of 5.34% on April 24, 2026, alongside significant intraday volatility. This intraday performance occurred in the wake of the company's Q1 FY2026 earnings report, released on April 22, 2026, which initially triggered a substantial negative reaction from the market.

The Q1 FY2026 financial results themselves were strong, with ServiceNow exceeding revenue and earnings guidance. Total revenue reached $3.8 billion, a 22% year-over-year increase, surpassing Wall Street's consensus of $3.7 billion. Non-GAAP diluted earnings per share also increased significantly to $0.97 from $0.81 in Q1 FY2025. The company further raised its full-year subscription revenue outlook. Strategically, ServiceNow also announced new AI-native manufacturing solutions and deepened its partnership with Google Cloud for autonomous enterprise operations, demonstrating continued innovation and market expansion. The company's AI product, Now Assist, showed strong traction, with management projecting an increase in AI revenue forecast to approximately $1.5 billion for 2026.

However, despite these positive financial and strategic developments, the market reacted negatively to the earnings report, leading to a significant stock plummet of 15-18% on April 23rd and extending into April 24th. Investors expressed concerns over the company's high valuation, geopolitical uncertainties impacting deal timings, particularly in the Middle East, and potential margin pressures stemming from recent acquisitions like Armis. Analysts, while largely maintaining "Buy" ratings, adjusted their price targets downward, reflecting scrutiny over the quality of growth, especially the organic component versus acquisition-driven growth.

The intraday upward movement of 5.34% on April 24th suggests a partial rebound within the trading day, indicating that some investors may have viewed the significant prior drop as an overselling event or an opportunity to buy the dip, reflecting the noted significant intraday volatility. This aligns with increased options activity on the day, with a rise in call options indicating anticipation of upward movement. Nonetheless, the overall sentiment following the earnings report remained cautious due to the broader concerns about the software sector and the impact of AI on established business models.

Technical Analysis of ServiceNow Inc (NOW)

Technically, ServiceNow Inc (NOW) shows a MACD (12,26,9) value of [-4.20], indicating a neutral signal. The RSI at 35.29 suggests neutral condition and the Williams %R at -85.46 suggests oversold condition. Please monitor closely.

Fundamental Analysis of ServiceNow Inc (NOW)

ServiceNow Inc (NOW) is in the Software & IT Services industry. Its latest annual revenue is $13.28B, ranking 30 in the industry. The net profit is $1.75B, ranking 31 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $150.70, a high of $240.00, and a low of $85.00.

More details about ServiceNow Inc (NOW)

Company Specific Risks:

- ServiceNow experienced significant margin compression in Q1 2026, with operating margin declining to 13.3% from 14.6% year-over-year, and subscription gross margin falling to 82.5% from 84.5% due to the Armis acquisition and geopolitical headwinds, impacting profitability despite a revenue beat.

- Geopolitical tensions in the Middle East led to a 75 basis point headwind in Q1 2026 subscription revenue growth due to delayed large on-premise deals, a factor the company has incorporated into its full-year outlook, indicating ongoing operational and revenue generation risks.

- Multiple analysts have downgraded ServiceNow and significantly cut price targets following Q1 earnings, reflecting concerns about a shift in enterprise spending priorities towards AI and away from traditional software, potentially leading to "seat compression" and increased competitive pressure from AI-driven solutions.

- A miss on Q1 2026 billings, which grew slower than total sales, indicates that the company is recognizing revenue faster than it collects cash, posing a potential headwind for future liquidity and slower revenue growth.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.