Autozone Inc Stock (AZO) Closed Down by 3.68% on Apr 10: Drivers Behind the Movement

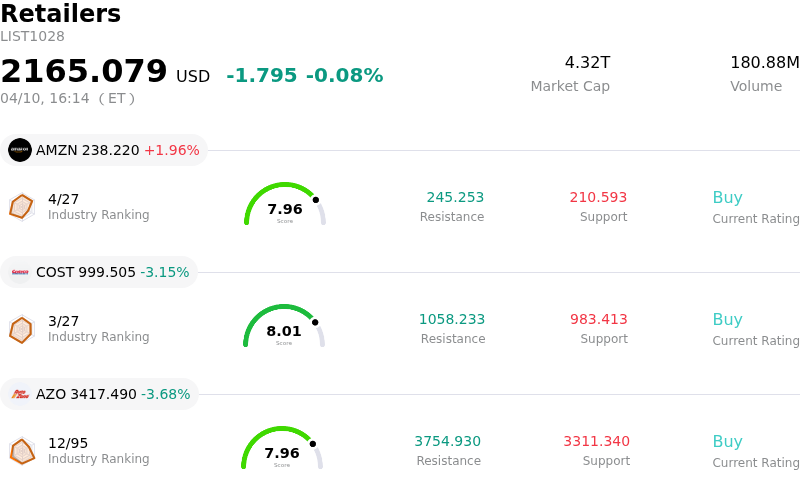

Autozone Inc (AZO) closed down by 3.68%. The Retailers sector is down by 0.08%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Amazon.com Inc (AMZN) up 1.96%; Costco Wholesale Corp (COST) down 3.15%; Autozone Inc (AZO) down 3.68%.

What is driving Autozone Inc (AZO)’s stock price down today?

AutoZone experienced a significant downward movement in its share price today, accompanied by notable intraday volatility. This fluctuation appears to be influenced by a confluence of factors, including investor reactions to recent financial data, shifts in market sentiment regarding its valuation, and broader industry dynamics.

The company's most recent quarterly earnings report, released on March 3, 2026, revealed mixed results. While AutoZone surpassed earnings per share expectations, it fell short on revenue forecasts. A key concern highlighted in the report was the impact of a substantial LIFO charge, which affected gross margins. This financial detail, coupled with an increase in selling, general, and administrative expenses and a reported decline in do-it-yourself (DIY) traffic, likely contributed to a cautious outlook among some investors.

Furthermore, market sentiment suggests that some traders are questioning whether the stock had run too far ahead of its underlying fundamentals. This has led to profit-taking following a period of strength. Despite a consensus "Buy" rating from analysts and an attractive long-term growth outlook, concerns about the company's valuation persist, with its forward price-to-earnings ratio trading at a premium compared to the industry average.

Recent institutional portfolio adjustments have also played a role. Reports indicate that some large institutional investors have either lowered their stake or realigned their holdings, signaling potential concerns about AutoZone's near-term performance and valuation. While some of these adjustments might be due to internal restructuring, the overall trend can influence broader market perceptions.

Finally, broader industry trends and company-specific risks are contributing to investor caution. The automotive aftermarket is navigating challenges such as evolving tariffs affecting supply chains, rising operational costs, and increased competition, particularly in the e-commerce segment. Macroeconomic factors, such as a slowdown in driven miles, could also weigh on future sales. These elements collectively contribute to the observed price volatility as investors assess both the immediate and long-term implications for AutoZone's performance.

Technical Analysis of Autozone Inc (AZO)

Technically, Autozone Inc (AZO) shows a MACD (12,26,9) value of [-65.05], indicating a neutral signal. The RSI at 54.87 suggests neutral condition and the Williams %R at -10.08 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Autozone Inc (AZO)

Autozone Inc (AZO) is in the Retailers industry. Its latest annual revenue is $18.94B, ranking 11 in the industry. The net profit is $2.50B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $4226.37, a high of $4800.00, and a low of $3011.22.

More details about Autozone Inc (AZO)

Company Specific Risks:

- AutoZone faces persistent earnings volatility and margin compression, evidenced by missing Wall Street's earnings estimates for the last four quarters and a 203-basis-point drop in gross margin during Q1 2026 due to LIFO impacts and increased operating expenses.

- Weakening consumer demand and declining customer sentiment pose a risk, as lower-income consumers, a significant portion of AutoZone's customer base, remain under financial pressure through 2025, and customer sentiment metrics (NPS and NPI scores) are nearing three-year lows.

- Macroeconomic headwinds, including increased fuel prices due to geopolitical events such as the war in Iran, are expected to weigh on sales performance, while higher product costs from U.S. tariffs continue to pressure margins as the company struggles to pass these costs to consumers due to strong competition.

- Recent analyst downgrades, including those from Goldman Sachs and Wolfe Research, signal a negative shift in outlook and highlight concerns about the stock's elevated valuation amid slower growth and heightened risks.

Recommended Articles