Applied Materials Inc Stock (AMAT) Closed Up by 3.07% on Apr 9: A Full Analysis

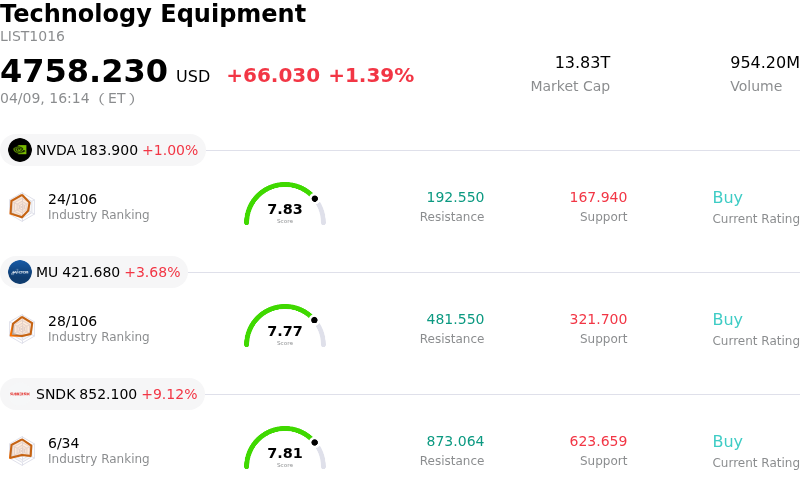

Applied Materials Inc (AMAT) closed up by 3.07%. The Technology Equipment sector is up by 1.39%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 1.00%; Micron Technology Inc (MU) up 3.68%; SanDisk Corporation (SNDK) up 9.12%.

What is driving Applied Materials Inc (AMAT)’s stock price up today?

Applied Materials experienced positive share price movement today, driven primarily by favorable analyst sentiment and a significant product announcement. Susquehanna, a prominent investment firm, raised its price target for Applied Materials to $500 from $435, maintaining a Positive rating for the stock in a report published today. This upward revision by analysts reflects growing confidence in the company's future performance. This follows several other analyst upgrades and increased price targets from various firms in recent months, contributing to a generally optimistic outlook for the company.

Adding to the positive momentum, Applied Materials unveiled two new advanced chipmaking systems yesterday, designed for angstrom-era logic chips. These new deposition systems, Precision Selective Nitride PECVD and Trillium ALD, are crucial for enabling 2nm and beyond Gate-All-Around technology, which is essential for developing faster and more power-efficient transistors in advanced artificial intelligence compute chips. The market reacted favorably to this product launch, with multiple reports indicating a surge in the stock after the announcement.

Furthermore, the company's strong financial performance in the first quarter of 2026, where it exceeded analyst expectations for both earnings per share and revenue, continues to underpin investor confidence. Applied Materials also provided an optimistic outlook for the second quarter of 2026, attributing strong guidance to accelerating investments in artificial intelligence and rising memory demand. Management has projected over 20% growth in its semiconductor equipment business for calendar year 2026, indicating robust demand.

The broader semiconductor equipment market is experiencing significant growth, largely propelled by investments in AI, particularly in leading-edge logic and memory technologies. Industry forecasts indicate sustained double-digit growth in global 300mm fab equipment spending for both 2026 and 2027. Applied Materials is strategically positioned to capitalize on these industry trends, given its leadership in advanced logic, DRAM, and packaging solutions. The company also recently increased its quarterly dividend, signaling financial strength and a commitment to enhancing shareholder returns.

Technical Analysis of Applied Materials Inc (AMAT)

Technically, Applied Materials Inc (AMAT) shows a MACD (12,26,9) value of [1.56], indicating a buy signal. The RSI at 62.69 suggests neutral condition and the Williams %R at -5.22 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Applied Materials Inc (AMAT)

Applied Materials Inc (AMAT) is in the Technology Equipment industry. Its latest annual revenue is $28.37B, ranking 10 in the industry. The net profit is $7.00B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $417.41, a high of $500.00, and a low of $280.00.

More details about Applied Materials Inc (AMAT)

Company Specific Risks:

- InvestingPro analysis indicates that AMAT's stock is currently overvalued relative to its Fair Value, placing it among companies on the most overvalued list and suggesting potential for price correction despite recent market momentum.

- Ongoing U.S. export restrictions and geopolitical tensions are projected to cause a 15-20% year-over-year decline in Applied Materials' revenues from the Chinese market for fiscal year 2025, reflecting continued market headwinds.

- Heightened geopolitical tensions, particularly in the Middle East, introduce fragility to the global semiconductor supply chain, threatening disruptions in access to essential manufacturing inputs like helium, which could impact production and costs.

- The company faces continuous regulatory compliance scrutiny following a $252.5 million settlement with the U.S. Department of Commerce for past export control violations involving China shipments, which highlights ongoing compliance risk and the necessity for enhanced internal audits and reporting.

Recommended Articles