Polestar Automotive Holding Uk Plc Stock (PSNY) Moved Up by 7.62% on Apr 2: Facts Behind the Movement

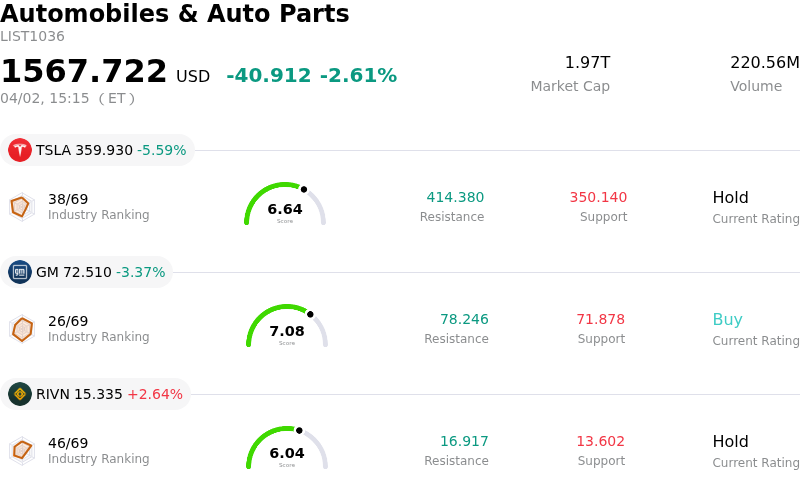

Polestar Automotive Holding Uk Plc (PSNY) moved up by 7.62%. The Automobiles & Auto Parts sector is down by 2.61%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Tesla Inc (TSLA) down 5.59%; General Motors Co (GM) down 3.37%; Rivian Automotive Inc (RIVN) up 2.64%.

What is driving Polestar Automotive Holding Uk Plc (PSNY)’s stock price up today?

Polestar's stock experienced significant upward movement, largely driven by strategic developments related to its financial structure and manufacturing operations. A key factor was Volvo Cars' decision to convert a substantial portion of its shareholder loan to Polestar into equity. This move is anticipated to alleviate Polestar's financial leverage and reduce interest obligations, thereby strengthening its balance sheet.

Concurrently, the announcement that future production of the Polestar 3 will be concentrated at its U.S. plant in South Carolina has been viewed positively by the market. This expanded manufacturing collaboration with Volvo could provide Polestar with access to established production expertise and scale benefits within a crucial electric vehicle market. These developments collectively suggest an improving short-term outlook for the company, as they address critical aspects of its financial stability and operational efficiency.

Moreover, analyst sentiment might be contributing to the upward momentum. Several reports indicate that Polestar could be undervalued, with some analysts suggesting a significant potential upside from its current trading levels. This re-evaluation of the company's valuation, coupled with its strategic advancements, could be attracting investor interest. The company's recent operational performance, including improved gross margins and narrowing net losses in past quarters, alongside plans for new model launches and retail network expansion, also provides a foundation for a more optimistic investor outlook.

The stock's movement may also be influenced by its short interest. With a relatively high days to cover ratio, any positive news or increased buying pressure could lead to a short squeeze, amplifying the upward price action as short sellers close their positions. This dynamic can contribute to heightened intraday volatility, especially when coupled with favorable company-specific news.

Technical Analysis of Polestar Automotive Holding Uk Plc (PSNY)

Technically, Polestar Automotive Holding Uk Plc (PSNY) shows a MACD (12,26,9) value of [-0.16], indicating a neutral signal. The RSI at 56.07 suggests neutral condition and the Williams %R at -15.67 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Polestar Automotive Holding Uk Plc (PSNY)

Polestar Automotive Holding Uk Plc (PSNY) is in the Automobiles & Auto Parts industry. Its latest annual revenue is $2.03B, ranking 37 in the industry. The net profit is $-2.05B, ranking 82 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Sell, with an average price target of $22.50, a high of $30.00, and a low of $15.00.

More details about Polestar Automotive Holding Uk Plc (PSNY)

Company Specific Risks:

- Polestar faces ongoing financial instability, evidenced by Volvo Cars' recent conversion of approximately $339 million in shareholder loans to equity and the extension of an additional $661 million in loan maturities to 2031, signaling continued dependence on major shareholders for liquidity management.

- The company is operating under a consensus "Sell" rating from analysts as of April 1, 2026, driven by concerns over potential tariffs, a projected slowdown in electric vehicle (EV) demand, enduring supply chain disruptions, and heightened market competition.

- Operational execution risks are elevated due to the planned consolidation of all global Polestar 3 production for non-Chinese markets to Volvo's U.S. plant by late 2026, involving the cessation of current production in China and a significant manufacturing transition.

- Polestar continues to grapple with fundamental profitability challenges, as reflected by previously reported significantly negative gross margins and persistent skepticism from investors and analysts regarding the company's credible path to achieving sustained positive earnings.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.