Corning Inc Stock (GLW) Opened Up by 3.03% on Mar 30: Drivers Behind the Movement

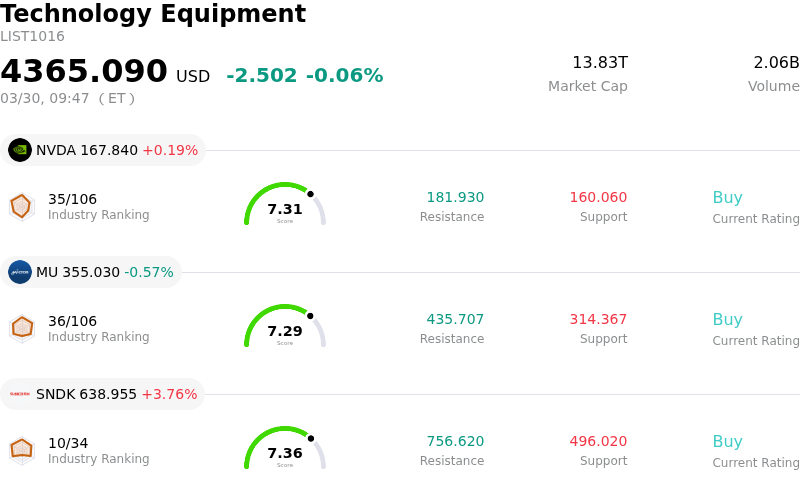

Corning Inc (GLW) opened up by 3.03%. The Technology Equipment sector is down by 0.06%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 0.19%; Micron Technology Inc (MU) down 0.57%; SanDisk Corporation (SNDK) up 3.76%.

What is driving Corning Inc (GLW)’s stock price up today?

Corning (GLW) experienced an upward share price movement today, indicating positive investor sentiment driven by several recent developments. A significant factor appears to be the company's strong positioning and continuous innovation in artificial intelligence (AI) data center connectivity solutions. Corning recently announced a collaboration with US Conec, licensing its PRIZM® TMT optical ferrule technology to expand its high-density optical connectivity offerings for next-generation AI networks. This move enables higher fiber counts within data centers, which is crucial as AI infrastructure scales.

Building on this, Corning showcased a suite of AI-oriented optical innovations at the Optical Fiber Communication Conference (OFC 2026) in mid-March. These new offerings, including multicore-fiber solutions, micro cables, and co-packaged optics systems, are designed to optimize AI data center networks by increasing density and efficiency. This strategic focus on the burgeoning AI ecosystem has positioned Corning as an essential supplier and has been met with an optimistic response from the markets. Investment banks have increasingly highlighted Corning as a major player in AI optical networking, emphasizing potential upward momentum.

Furthermore, the company recently launched its toughest cover material yet, Corning Gorilla Glass Ceramic 3, in early March. This advanced material, which will debut on Motorola's upcoming razr fold device, offers enhanced drop durability and is expected to strengthen relationships with device makers and boost demand for Corning's specialty materials.

Analyst sentiment has been broadly positive, with several financial institutions reiterating "Buy" ratings and raising price targets for GLW throughout March. For instance, B of A Securities reaffirmed its "Buy" rating and increased its price target earlier this month, following similar upward adjustments from Citigroup, Morgan Stanley, UBS, and Mizuho in prior weeks. This strong analyst conviction regarding Corning's growth potential and strategic market positioning has likely contributed to increased buying interest.

Finally, Corning reported strong fourth-quarter 2025 financial results in late January, with core sales and core EPS showing significant year-over-year growth. The company also provided an optimistic outlook for the first quarter of 2026, forecasting accelerated year-over-year growth in core sales and core EPS, and upgraded its Springboard Plan for faster sales growth. These solid financial indicators and positive guidance contribute to a favorable investment outlook.

Technical Analysis of Corning Inc (GLW)

Technically, Corning Inc (GLW) shows a MACD (12,26,9) value of [2.41], indicating a neutral signal. The RSI at 52.74 suggests neutral condition and the Williams %R at -51.01 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Corning Inc (GLW)

Corning Inc (GLW) is in the Technology Equipment industry. Its latest annual revenue is $15.63B, ranking 7 in the industry. The net profit is $1.60B, ranking 3 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $131.37, a high of $171.00, and a low of $91.00.

More details about Corning Inc (GLW)

Company Specific Risks:

- Elevated valuation metrics, including a high price-to-earnings (P/E) ratio, have led to recent intraday declines and concerns that the stock may be overvalued, posing a risk of pullbacks and profit-taking from current levels.

- Significant insider selling activities, including the CEO's disposal of 137,514 shares on February 26th and total executive sales of approximately $32.6 million in Q1 2026, suggest potential diminishing confidence in future performance or a belief in current overvaluation by company insiders.

- The company's substantial reliance on AI-driven capital expenditures exposes it to significant downside risk from any slowdown in the AI sector or increased competitive pressure from alternative data center connectivity technologies, such as copper.

- Operational headwinds in key segments include declining glass volumes in the display technologies segment due to cyclical saturation, and the solar segment experiencing heavy cash burn from initial ramp-up costs despite strong sales, impacting net income.