Arm Holdings PLC Stock (ARM) Moved Up by 15.40% on Mar 26: Drivers Behind the Movement

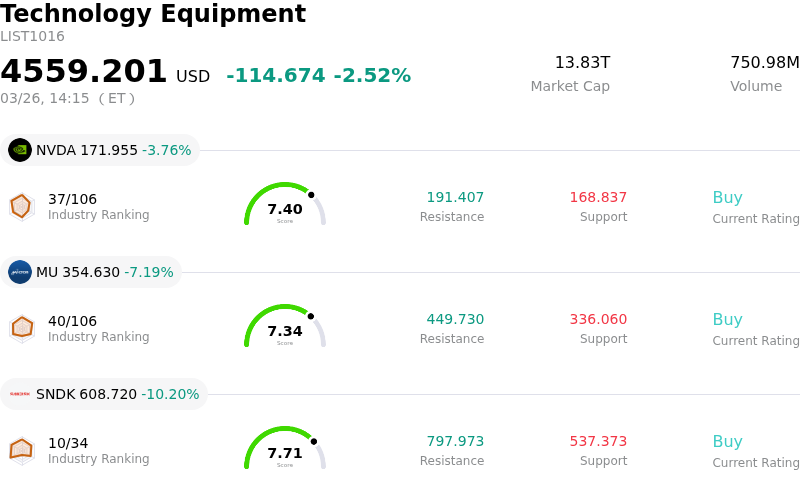

Arm Holdings PLC (ARM) moved up by 15.40%. The Technology Equipment sector is down by 2.52%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) down 3.76%; Micron Technology Inc (MU) down 7.19%; SanDisk Corporation (SNDK) down 10.20%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

ARM Holdings experienced significant upward movement in its share price due to a confluence of major strategic announcements and overwhelmingly positive analyst forecast adjustments. The primary catalyst was the official launch of Arm's first in-house produced silicon, the Arm AGI CPU, designed specifically for AI data centers. This represents a pivotal shift in the company's business model from primarily licensing intellectual property to also developing and selling its own chips, opening up a multi-billion-dollar revenue opportunity.

This new AGI CPU targets agentic AI workloads and has garnered immediate high-profile adoption, with Meta Platforms identified as a lead co-developer and primary customer. Other major technology companies such as OpenAI, Cloudflare, SAP, and SK Telecom are also confirmed customers or partners, underscoring strong industry validation for Arm's new offering.

In conjunction with these product launches and strategic partnerships, there has been a wave of analyst upgrades and increased price targets for ARM. Notably, Needham upgraded ARM to a "Buy" rating with a price target of $200.00, shifting from a previous "Hold" rating. Other firms like Raymond James, Guggenheim, Wells Fargo, RBC Capital, Deutsche Bank, Barclays, Jefferies, Evercore ISI, and UBS also either upgraded ratings or significantly raised their price targets for ARM, reflecting increased confidence in the company's market potential and the financial impact of its AI initiatives.

Analysts anticipate that this new chip business could generate substantial additional revenue, with projections ranging from an estimated $15 billion annually within five years to $15 billion by fiscal year 2031, with total revenues potentially reaching $25 billion by fiscal year 2031. This expansion into direct chip production and the strong customer traction in the burgeoning AI data center market are seen as transformative for Arm's growth trajectory, complementing its traditional licensing model and offsetting any potential slowdowns in its smartphone chip design business.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [2.36], indicating a buy signal. The RSI at 77.17 suggests buy condition and the Williams %R at -17.36 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.01B, ranking 26 in the industry. The net profit is $792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $157.88, a high of $227.00, and a low of $81.78.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- ARM's stock is currently trading at a high valuation, with a P/E ratio of 209, suggesting it may be overvalued relative to its fair value and leaving little margin for error in its performance.

- The company faces significant execution risks and a long pathway to profitability as it pivots from its traditional intellectual property licensing model to directly selling its own AGI CPU silicon, with ambitious long-term revenue projections for this new segment.

- ARM's strategic shift to become a direct vendor of chips introduces potential channel conflict and direct competition with its historical customer base and existing licensees, which could strain crucial business relationships.

- The revenue growth rate, particularly from its established licensing segment, tends to be erratic and lumpy quarter to quarter, contributing to inherent volatility and complexity in financial modeling.