Arm Holdings PLC Stock (ARM) Moved Up by 12.94% on Mar 25: A Full Analysis

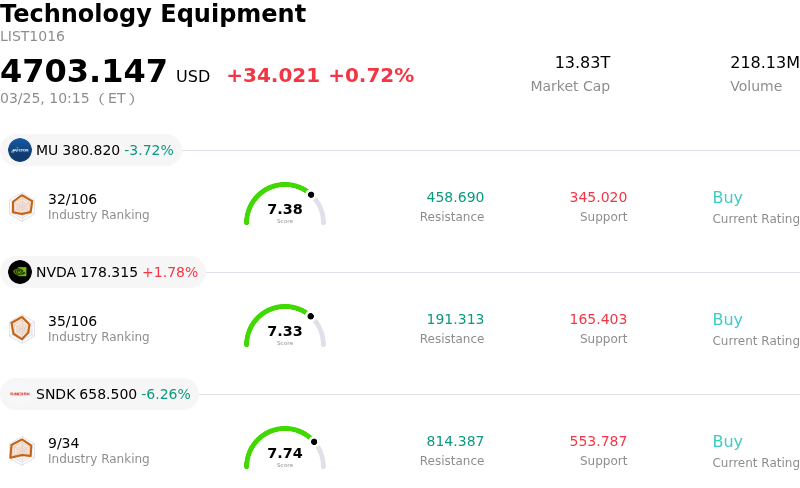

Arm Holdings PLC (ARM) moved up by 12.94%. The Technology Equipment sector is up by 0.72%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 3.72%; NVIDIA Corp (NVDA) up 1.78%; SanDisk Corporation (SNDK) down 6.26%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

Arm Holdings experienced significant upward movement today, driven by a major strategic announcement and robust future financial projections. The company revealed a pivotal shift in its business model, moving beyond its traditional role of solely licensing chip designs to directly developing and selling its own chips for artificial intelligence (AI) workloads. This marks the most substantial change in Arm's operational strategy in its 35-year history.

The focal point of this transformation is the introduction of the Arm AGI CPU, its first internally designed chip specifically tailored for AI data centers and agentic AI applications. This new product is positioned to deliver substantial performance benefits, reportedly offering more than double the performance per rack compared to x86 platforms and leading to significant capital expenditure savings for AI data center infrastructure.

Accompanying this product launch, Arm provided ambitious long-term financial guidance. The company anticipates its new chip business alone could generate approximately $15 billion in annual sales within five years, contributing to a projected total annual revenue of $25 billion and earnings per share of $9 by fiscal year 2031. This forecast represents a substantial increase over its current revenue and fundamentally redefines the market's valuation perspective of Arm, positioning it as an AI hardware leader with considerable growth potential.

Further bolstering investor confidence are key customer endorsements and positive analyst revisions. Meta Platforms has been confirmed as the inaugural major customer for the AGI CPU, with other prominent tech entities like OpenAI, Cloudflare, SAP, and SK Telecom also planning deployments. In response to these developments, several Wall Street analysts have upgraded their ratings and significantly increased price targets for Arm, reflecting a strong bullish outlook on the company's expanded market opportunity and enhanced earnings power in the rapidly evolving AI landscape.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [1.63], indicating a buy signal. The RSI at 63.74 suggests neutral condition and the Williams %R at -19.17 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.01B, ranking 26 in the industry. The net profit is $792.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $149.70, a high of $205.00, and a low of $81.78.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- The accelerating adoption of the open-source RISC-V architecture poses a significant long-term competitive threat to Arm's proprietary licensing and royalty business model.

- Arm's substantial revenue exposure, estimated at 20-25% from Arm China, is subject to significant geopolitical risks and limited management control, potentially disrupting a critical revenue stream.

- Analyst concerns persist regarding slowing royalty growth and potential margin contraction, with Q4 guidance forecasting a deceleration to low-teens percentages, which could pressure the stock's high valuation.

- The strategic shift toward developing and selling its own silicon (compute subsystems) introduces execution risks, including potential channel conflict with long-time licensees and operational challenges in a new business area.