Pop Mart Revenue Tops 30 Billion Net Profit Surges 284%, Why Did Stock Price Plummet 15%?

AI Podcast

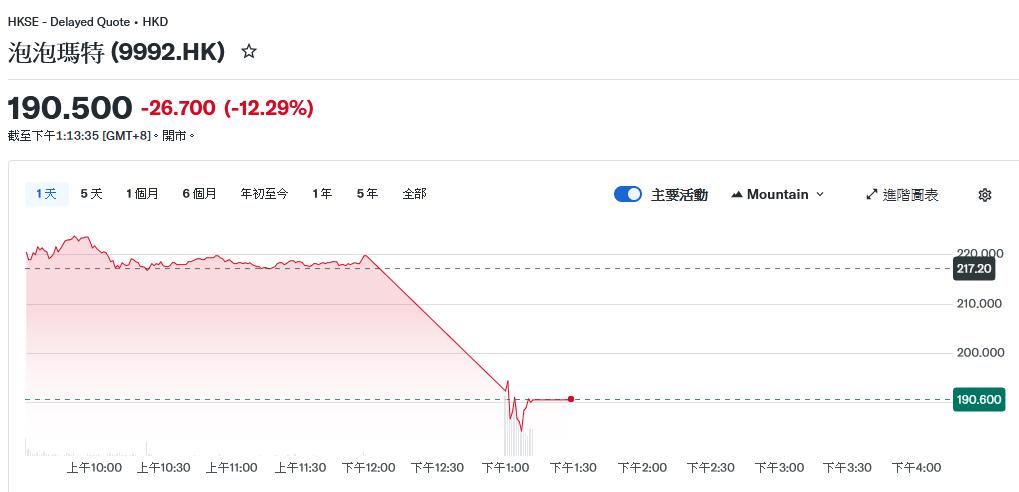

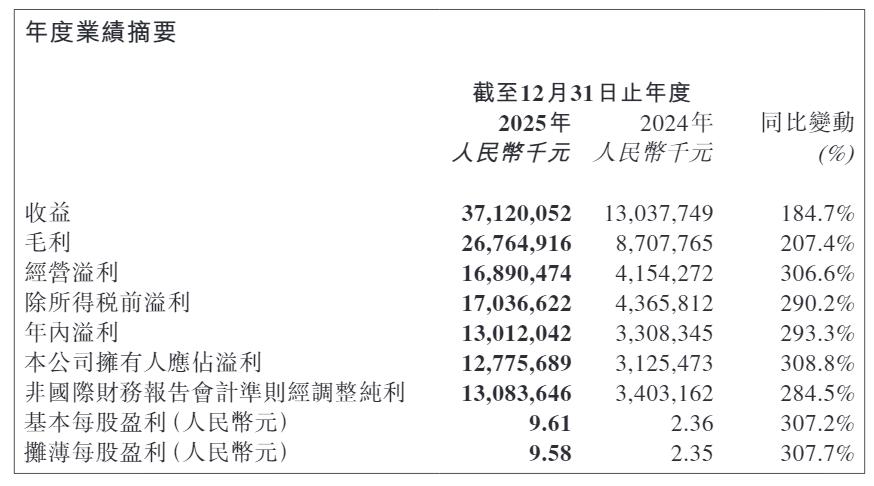

Pop Mart's 2025 annual report showed revenue of 37.12 billion yuan, up 184.7%, and adjusted net profit of 13.08 billion yuan, up 284.5%. Despite strong financial growth and revenue exceeding 10 billion yuan from the Labubu IP, its shares fell 15% intraday. Investors expressed concern over the company's over-reliance on Labubu, questioning its revenue diversification and growth momentum beyond this single IP. While other IPs showed growth, none rivaled Labubu, highlighting the challenge of establishing a sustainable growth curve.

TradingKey - Following the release of Pop Mart’s 2025 annual report on March 25, its Hong Kong-listed shares plunged as much as 15% intraday. Despite stellar full-year financial data that generally met market expectations, investor dissatisfaction was directly reflected in the share price. The core reason is that the report failed to sufficiently demonstrate revenue diversification and growth momentum beyond the Labubu IP, further heightening market concerns over the company's over-reliance on a single core IP.

As the "backbone" driving Pop Mart's growth, THE MONSTERS series, to which Labubu belongs, became a global sensation in 2025. Revenue surpassed the 10-billion-yuan mark for the first time, reaching 14.16 billion yuan, a staggering 365.7% year-on-year increase. Consequently, Labubu became the first designer toy IP to join the "10-billion-yuan club."

Driven by this performance, Pop Mart's total annual revenue reached 37.12 billion yuan, a significant year-on-year increase of 184.7%. Adjusted net profit surged 284.5% to 13.08 billion yuan, while the gross margin reached 72.1%, slightly exceeding the previous market estimate of 71.6%.

Looking at the performance structure, the company's global expansion and multi-IP operation strategy have begun to yield results. In addition to Labubu, six IPs—including SKULLPANDA, CRYBABY, MOLLY, DIMOO, and Starman—each recorded annual revenue exceeding 2 billion yuan. Another 11 IPs surpassed the 100-million-yuan revenue mark, bringing the total number of IPs with over 100 million yuan in revenue to 17, an increase of four compared to the first half of 2025.

By regional market, all segments achieved high-speed growth. Revenue from the Chinese mainland reached 20.85 billion yuan, up 134.6% year-on-year, with a net increase of 14 offline stores to 445. The Asia-Pacific market recorded 8.01 billion yuan in revenue, a 157.6% year-on-year increase, with a net addition of 31 stores to reach a total of 85.

The Americas market, centered on the U.S., expanded rapidly, with annual revenue skyrocketing 748.4% to 6.81 billion yuan and a net increase of 42 stores to 64. In the European market, through expansion into core cities in countries such as the UK, Denmark, and the Netherlands, revenue reached 1.45 billion yuan, a 506.3% year-on-year increase, with a net addition of 22 stores to reach 36.

Despite the glowing financial performance across the board, investor concerns have not dissipated.

The dominance of the Labubu series has led to market concerns that the company lacks a "second pillar" for growth; should the IP's popularity fade, the company's financial performance could face significant volatility.

Previously, the company proposed a strategy to build a multi-IP matrix in the first half of 2025. While this report shows multiple IPs with revenues exceeding 100 million yuan, there is still a significant gap before a second growth engine capable of rivaling Labubu can be established.

How to build a sustainable growth curve beyond its core IP has become a critical challenge for Pop Mart and remains the central focus for investors moving forward.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.