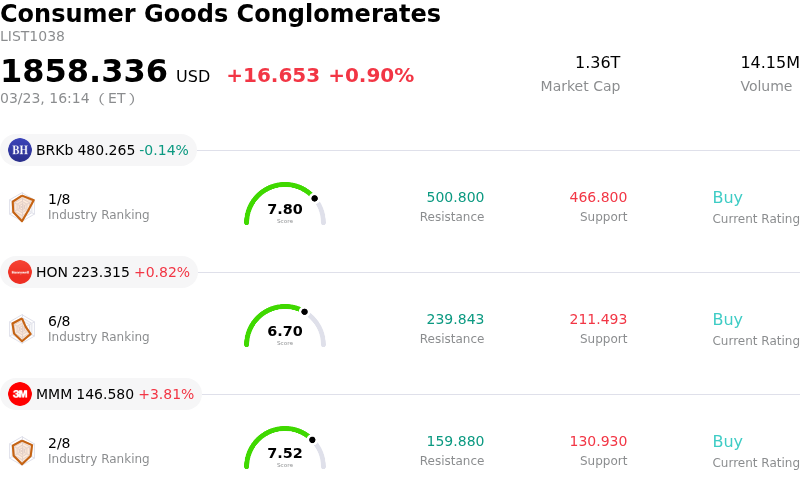

3M Co Stock (MMM) Closed Up by 3.81% on Mar 23: Key Drivers Unveiled

3M Co (MMM) closed up by 3.81%. The Consumer Goods Conglomerates sector is up by 0.90%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Berkshire Hathaway Inc (BRKb) down 0.14%; Honeywell International Inc (HON) up 0.82%; 3M Co (MMM) up 3.81%.

What is driving 3M Co (MMM)’s stock price up today?

The upward movement in 3M (MMM) stock with significant intraday volatility on March 23, 2026, appears to be influenced by several recent positive developments and a generally improving outlook for the company. These factors collectively contributed to increased investor confidence.

A notable catalyst is the company's strategic decision to enhance its portfolio and financial flexibility. Just days prior, on March 19, 2026, 3M announced a partnership with Bain Capital to acquire Madison Fire & Rescue for $1.95 billion, forming a new joint venture. This move is expected to broaden 3M's safety portfolio, enhance margins, and generate strong free cash flow, with 3M contributing its Scott Safety business and receiving $700 million in cash proceeds while retaining majority ownership. This indicates a focused strategy on optimizing its industrial segments for future growth and profitability.

Investor sentiment has also likely been buoyed by recent financial and strategic communications. At the JPMorgan Industrials Conference on March 17, 2026, 3M management outlined strategic priorities, including a target of 3% organic growth for 2026 and an aim for a 25% operating margin by 2027. The company also highlighted plans for significant product launches and investment in high-growth areas like Expanded Beam Optical interconnect technology for AI data centers. These forward-looking statements suggest a path toward improved operational performance.

Furthermore, a recent dividend increase and positive analyst commentary have likely played a role. On February 3, 2026, 3M declared a quarterly dividend of $0.78 per share, an increase from its previous payment, demonstrating a commitment to returning capital to shareholders. Although the overall analyst consensus remains a "Hold," some firms, like UBS, reiterated a "Buy" rating and a $190 price target in mid-March, expressing optimism about mid- and longer-term opportunities. The company's fourth-quarter 2025 adjusted earnings per share also surpassed analyst expectations when reported on January 20, 2026, along with initiating full-year 2026 guidance for adjusted EPS that, despite being initially perceived as modest, includes projections for strong adjusted operating cash flow and operating margin expansion.

Finally, ongoing progress in resolving significant legal liabilities, such as the earplug and PFAS settlements, continues to mitigate long-standing overhangs, allowing investors to increasingly focus on the company's core operational strengths and strategic direction post the Solventum spin-off, which was completed in April 2024. These cumulative positive developments have likely contributed to the stock's appreciation.

Technical Analysis of 3M Co (MMM)

Technically, 3M Co (MMM) shows a MACD (12,26,9) value of [-3.84], indicating a sell signal. The RSI at 26.87 suggests sell condition and the Williams %R at -91.71 suggests oversold condition. Please monitor closely.

Fundamental Analysis of 3M Co (MMM)

3M Co (MMM) is in the Consumer Goods Conglomerates industry. Its latest annual revenue is $24.95B, ranking 4 in the industry. The net profit is $3.25B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $174.56, a high of $205.00, and a low of $122.11.

More details about 3M Co (MMM)

Company Specific Risks:

- Over 15,000 personal injury PFAS lawsuits remain pending, with bellwether trials anticipated in 2026, creating significant ongoing financial uncertainty and potential for substantial future liabilities despite prior municipal settlements.

- JPMorgan recently downgraded the stock due to lingering PFAS valuation risks, highlighting that substantial net pre-tax cash payments ($3.5 billion in 2025) for litigation continue to weigh heavily on the company's financial outlook.

- A Special Master's report in early March 2026 detailed "serious failures" and "reckless indifference" by a law firm handling claims in the Combat Arms Earplugs settlement, indicating potential reputational damage and persistent oversight challenges related to managing large-scale legal resolutions.

- The significant disparity between 3M's adjusted and GAAP earnings, driven by persistent and substantial litigation costs, reveals that operational improvements are being heavily masked by ongoing legal financial burdens, impacting true reported profitability.