Lam Research Corp Stock (LRCX) Moved Up by 3.33% on Mar 13: What Investors Need To Know

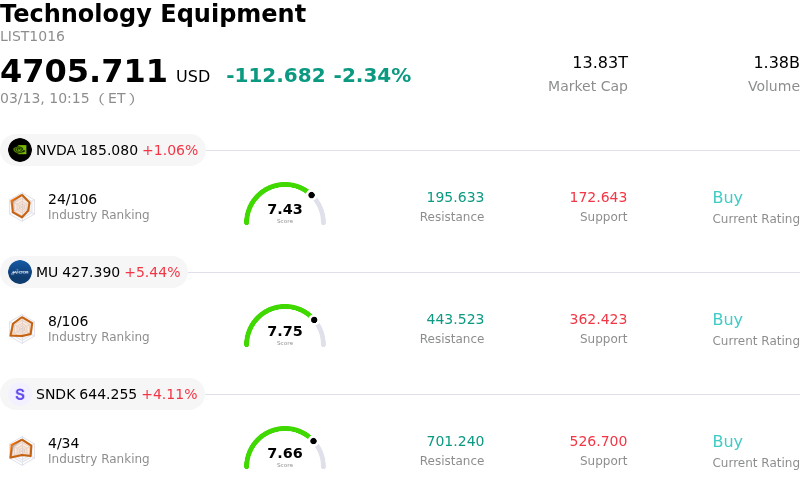

Lam Research Corp (LRCX) moved up by 3.33%. The Technology Equipment sector is down by 2.34%. The company outperformed the industry. Top 3 stocks by turnover in the sector: NVIDIA Corp (NVDA) up 1.06%; Micron Technology Inc (MU) up 5.44%; SanDisk Corporation (SNDK) up 4.11%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research (LRCX) experienced positive stock movement today, driven by a confluence of favorable analyst sentiment, robust industry tailwinds, and strategic company developments.

Multiple analyst firms have recently reiterated positive ratings and raised price targets for Lam Research. For instance, Barclays adjusted its price target upward earlier this week, maintaining an "Equal-Weight" rating. This follows a trend of several analysts from firms like Morgan Stanley, Needham, Evercore ISI Group, and Susquehanna revising their price targets higher and issuing "Buy" or "Outperform" recommendations in recent months. This consistent optimism from the analyst community suggests a belief in the company's continued growth trajectory and strong market position.

The broader semiconductor equipment industry is also experiencing a significant boom, largely fueled by the escalating demand for Artificial Intelligence (AI) infrastructure. Industry forecasts predict record-breaking sales for global semiconductor manufacturing equipment in the coming years, with wafer-fab equipment (WFE) expanding substantially. This expansion is driven by the need for advanced logic nodes and memory components crucial for AI accelerators and high-performance computing. As a leading provider of wafer fabrication equipment, Lam Research is well-positioned to capitalize on this secular growth trend.

Adding to the positive sentiment are reports indicating Lam Research's potential interest in acquiring BE Semiconductor (BESIY). Such a strategic move would allow Lam Research to enhance its capabilities in critical chip-packaging technology, further strengthening its competitive advantage and technological offerings in an evolving market. This type of M&A activity often signals proactive management and a commitment to future growth, which can be viewed favorably by investors.

Furthermore, institutional investors have shown increased confidence in Lam Research, with entities like Employees Retirement System of Texas and Entropy Technologies LP recently increasing or initiating significant stakes in the company. This institutional buying activity underscores a positive outlook on the company's prospects. These factors collectively contributed to the upward movement observed in LRCX's share price.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [0.06], indicating a neutral signal. The RSI at 42.76 suggests neutral condition and the Williams %R at -75.38 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $270.39, a high of $325.00, and a low of $116.32.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Significant insider selling pressure was observed in recent regulatory filings, with a director reducing their stake by over 12% and the CFO selling $11.2 million in stock within the last 72 hours, signaling cautious sentiment.

- The company faces ongoing scrutiny from the US House Select Committee on the CCP regarding its sales practices in China, compounded by a projected decline in revenue contribution from China due to export controls and increased geopolitical risks.

- Lam Research is experiencing a negative outlook due to a decline in gross margin, attributed to a less favorable customer mix and demand volatility from leading-edge clients, alongside planned capital expenditure cuts by Intel.

- Analyst valuation models suggest the stock may be significantly overvalued, with InvestingPro analysis indicating overvaluation relative to its fair value and GuruFocus estimating a potential downside of over 34%, implying a risk of price correction.