- NFTs are evolving from collectibles into financial instruments via DeFi—enabling lending, staking, fractionalization, and insurance.

- These integrations enhance utility, liquidity, and yield, but they also introduce risks such as liquidations, brilliant contract exploits, and governance failures.

- Next waves include tokenized real-world assets, identity/reputation NFTs for under-collateralized lending, and cross-chain interoperability.

- Investors should treat NFTs like high-beta fintech: choose platforms selectively, diversify, and actively manage risk in a still-experimental market.

From Collectibles to Financial Instruments

TradingKey - When non-fungible tokens (NFTs) first went mainstream, they were handled as digital collectibles, art, music, and profile images with demonstrable scarcity. Although that early chapter attracted interest and funds, it also raised suspicion that NFTs were something more than speculative tokens. The next chapter, however, demonstrates that NFTs are anything but financial building materials. When paired with decentralised finance (DeFi), NFTs are concluding with utility, liquidity, and yield opportunities. The process has altered the nature of ownership investment in the digital economy.

DeFi has always thrived on composability, the ability of protocols to interconnect and build upon each other, much like digital Lego. NFTs, as a form of unique ownership rights, fit into that mix. And rather than languishing inactive in wallets, NFTs can be staked, used as collateral, fractionalized, and insured. These redescriptions of NFTs as active financial instruments are paving the way for a next-generation Web3 innovation.

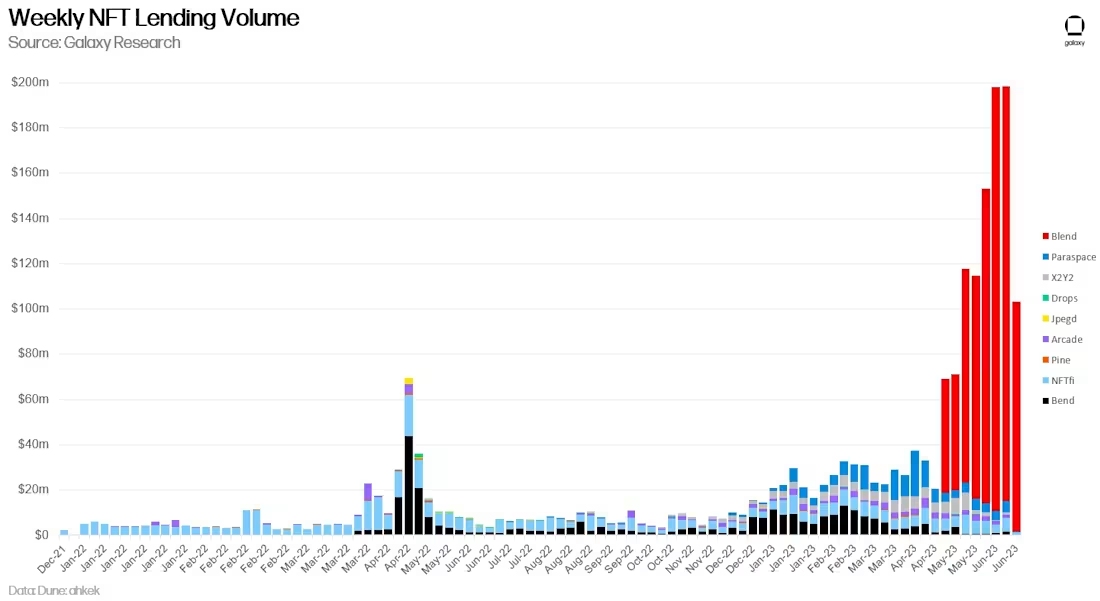

NFT Lending and Collateral

By far one of the most influential of these combinations is lending. Sites like NFTfi and BendDAO enable bearers of NFTs to borrow against their NFTs as collateral using ETH or stablecoins. What this does is rectify one of the most significant issues with the NFT marketplace: illiquidity.

Traditionally, investors with a desire for liquidity were forced to sell NFTs at unfavorable moments. Now they can borrow against them, just as homeowners can with their equity loans. For lenders, it develops a new asset class of collateral with verifiable ownership on-chain. And yet the model isn't risk-free. If the floor has a price collapse, borrowers get liquidated, and lenders are stuck with illiquid collateral. Nevertheless, the principle that NFTs can release capital without being sold is revolutionary.

Source: https://www.galaxy.com

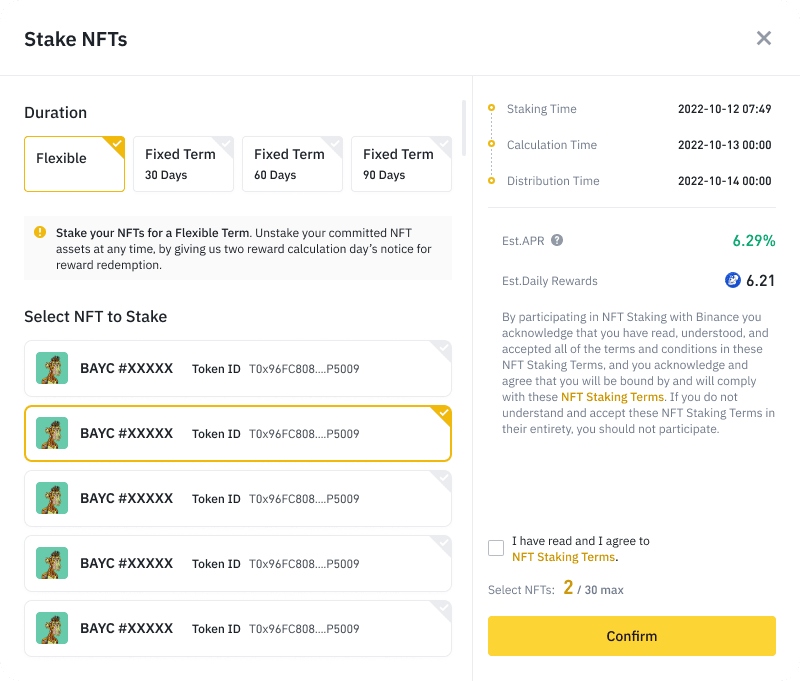

Staking and Yield Strategies

NFT staking has become yet another decentralised finance (DeFi) intersector. Projects compensate holders of locked-up NFTs with governance or utility tokens, transforming ownership into a revenue-generating process. In gaming worlds, NFTs of characters, land, or weapons may be staked or rented out with the goal of earning returns.

This reflects real-world ideas such as renting out real estate or machinery. Where a static image on a blockchain becomes a dead asset, the NFT is a productive asset. For investors, this transforms NFTs from speculative investments to income-generating tools, broadening their portfolio applications.

Source: https://www.binance.com

Fractionalization and Market Accessibility

Most retail investors are unable to afford high-value NFTs. Fractionalization fixes this by breaking one NFT into fungible ERC-20 tokens that can be sold in part. A CryptoPunk that goes for hundreds of thousands of dollars can be divided into thousands of slices, which you can sell through decentralized exchanges.

Fractionalization opens up access but also introduces liquidity. By making the NFT tradable in fractional parts, the stock-like nature with a broader base of buyers increases. Liquidity pools that combine fractionalized NFTs with tokens from the DeFi domain are being experimented with, promising a future where NFTs are exchanged through DeFi markets as fungible assets.

Insurance and Risk Management

With NFTs entering DeFi territory, risks are compounding. Bugs in smart contracts, price fluctuations, and oracle manipulation can lead to substantial losses. The advent of NFT insurance protocols is a direct result of this. These are where investors can hedge against technical or marketplace failures. Just as with how DeFi lending triggered the proliferation of insurance in DeFi, NFT finance has breeding ground-level safety nets.

For institutional investors to engage seriously with NFTs, such risk management frameworks are crucial. These professionalize the marketplace and bring it closer towards an honest-to-God financial sector and less of a Wild West speculation ground.

Real-World Assets and Identity

Ahead, the intersection of NFTs and DeFi has a lot further to go beyond art or digital game possessions. Physical assets, land deeds, high-end goods, even stocks and bonds, are able to become tokenized as NFTs and interfaced with DeFi mechanisms. Envision lending stablecoins against a tokenized real estate deed or fractioning portions of master art. It blurs the line of conventional finance and blockchain efficiency.

Identity and reputation also have a bright future. NFTs can serve as proof of credentials or a history of credits and be used to support undercollateralized lending in DeFi. Instead of overcollateralization only, protocols may consider an NFT of a borrower's digital reputation or a proven identity.

Chain and Cross-Protocol Synergies

NFT action is no longer Ethereum-only. Solana, Polygon, Avalanche, and other chains have flourishing NFT ecosystems. Cross-chain bridges and interoperability norms are materializing to permit NFTs to pass effortlessly from one blockchain to another. Why this matters for DeFi is that liquidity diversified across chains needs to converge and limit inefficiencies sooner or later. Future DeFi products could combine NFTs as collateral across various blockchain systems, establishing universal lending markets.

The more interoperable the systems are, the greater the financial prominence of NFTs will grow. Investor Considerations With investors, this convergence presents opportunities and risks. Notably, NFTs are evolving into financial assets with diversified utility, enhanced liquidity, and yield streams. Front-running protocols of NFT lending, staking, and insurance could rapidly expand if adoption increases. Negatively, sophistication heightens danger. Liquidations, exploits of intelligent contracts, and governance breaks continue to be omnipresent. The experimental aspect remains the synthesis of NFTs and DeFi. Volatility investor behavior anticipates one should be. Selective platform choice, diversified exposure, and constant danger supervision are imperative.

Source: https://www.coindoo.com

Conclusion: A Monetary Future Ahead of NFTs

NFTs, which were once considered cultural assets, are slowly transitioning into the world of finance. When paired with DeFi, they are no longer merely tectonic badges of ownership but instruments of access to capital, yield creation, and interaction with deeper economic systems. Lending, staking, fractionalization, and insurance suggest a world where NFTs become a part of the piping of the world of decentralized financing. Over the next ten years, we can expect real-world assets, identity, and cross-chain systems to continue to enhance this interoperability further. Winners will be those projects that effectively combine innovation with risk management, building scalable and reliable platforms. For investors, the trick is seeing NFTs as anything other than static collectibles and viewing them as active tools of the changing Web3 financial landscape.