Nvidia Earnings Are Coming: What Should Investors Focus on Most?

AI Podcast

NVIDIA's Q1 FY27 earnings are expected to show robust growth, with revenue around $78.9 billion and EPS of $1.77. Key focal points include data center revenue re-acceleration, driven by strong networking growth, and the impact of supply chain bottlenecks, particularly HBM memory and advanced process capacity. The successful ramp-up of Blackwell platform chips is crucial for future earnings certainty, with projections indicating it will dominate NVIDIA's AI chip shipments. Export controls on China continue to pose a structural challenge, impacting revenue and accelerating the shift to domestic alternatives. Despite these risks, Wall Street remains bullish, with valuation seen as rational relative to growth prospects.

TradingKey - After the market close on May 20, Eastern Time, NVIDIA ( NVDA.US) will announce its first-quarter financial results for fiscal year 2027. The market expects revenue of approximately $78.9 billion, a year-over-year increase of about 79%, and adjusted earnings per share of approximately $1.77.

Citi expects revenue to reach $80 billion, exceeding consensus estimates, primarily driven by the faster-than-expected mass production of B300 chips; Morgan Stanley expects revenue to beat estimates by approximately $3 billion; Bank of America analyst Vivek Arya expects NVIDIA's revenue this quarter to exceed sell-side consensus by 2% to 4%, or approximately $2 billion to $4 billion.

With the market reaching a consensus expectation that "NVIDIA will always exceed expectations," the biggest uncertainty for this report is no longer whether it will beat forecasts, but rather the magnitude of the beat and the structural health of core metrics. The following five dimensions are the key focal points of this earnings report.

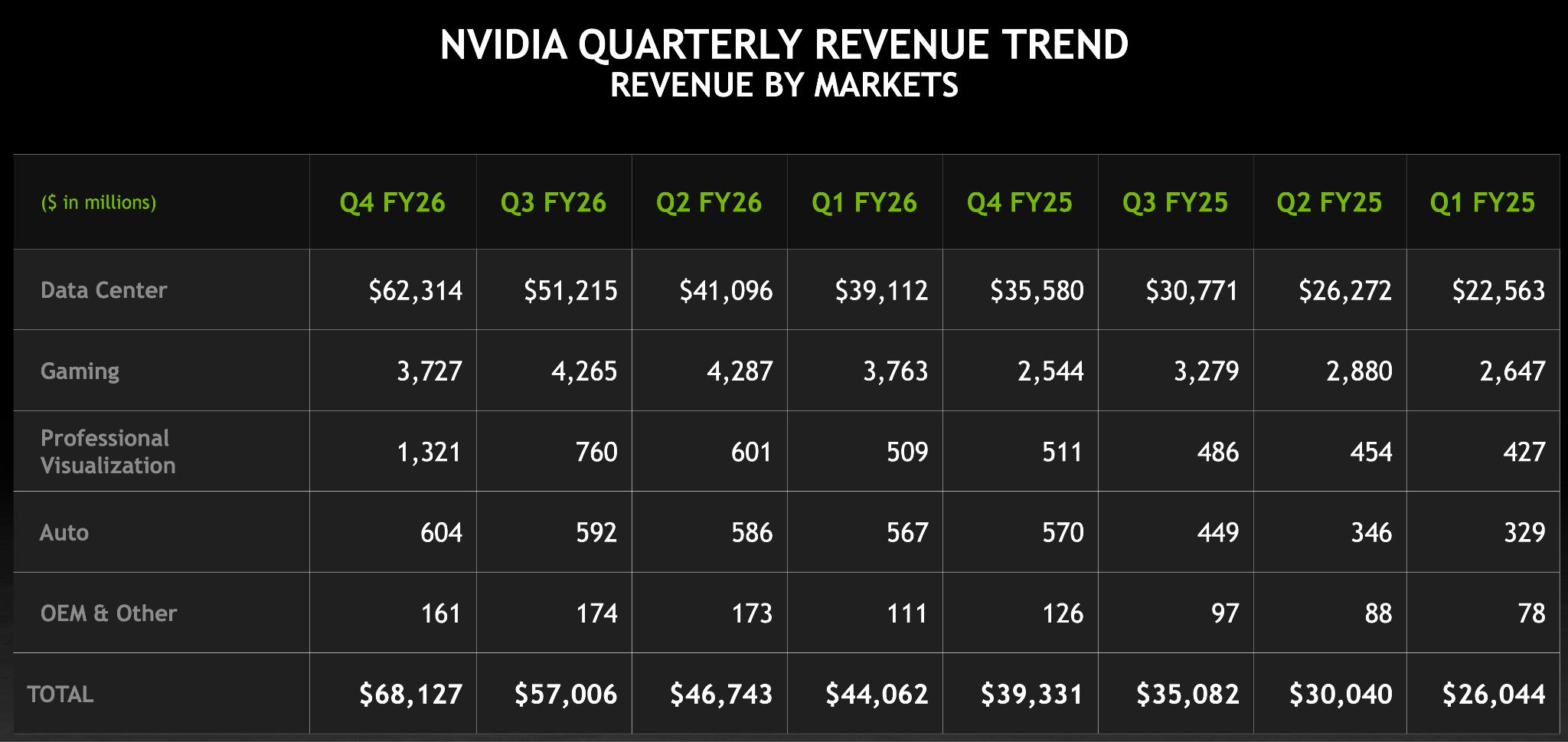

Can Data Center Revenue Deliver on "Re-acceleration" Expectations?

Institutions generally expect data center revenue to range from $73 billion to $74 billion, representing a year-over-year growth rate of approximately 88%. Networking growth is particularly striking; the market expects Computing revenue of about $60.95 billion, up 70.8% YoY, while Networking revenue is anticipated to reach approximately $12.75 billion—a massive 272.7% YoY increase that significantly outpaces the growth of GPU hardware itself.

AI training clusters are evolving toward hyperscale distributed architectures, leading to a continuous increase in the value proposition of interconnects within computing systems. Consequently, Mellanox (NVIDIA's networking solutions provider) is becoming NVIDIA’s second growth engine.

Market attention is centered on the fact that the combined annual capital expenditure of the four major hyperscalers (AWS, Microsoft Azure, Google Cloud, and Meta) has climbed to approximately $630 billion. Whether NVIDIA’s data center revenue growth can consistently exceed the growth of these providers' CapEx will be a key metric in validating the continued expansion of its market share.

Supply chain bottlenecks continue to constrain capacity release.

During a recent joint appearance with Dell, Jensen Huang noted that the primary supply bottleneck is currently memory (HBM), followed by advanced process capacity. While Nvidia has planned its supply chain two to three years in advance, global capacity still struggles to keep pace with the rapid growth of AI demand in the short term.

The timing of when this structural imbalance between supply and demand can be eased will directly determine the room for breaking through the earnings ceiling.

Whether the supply structure can be effectively improved will also be one of the key focuses of this earnings report.

The Blackwell platform is Nvidia's current-generation flagship product, and the actual progress from production ramp-up to customer deployment is the core basis for investors to assess earnings certainty.

Previously, according to the latest AI Server industry survey from TrendForce, the shipment structure of NVIDIA's high-end AI chips will undergo changes in 2026. Influenced by shifting international dynamics and the time required for supply chain calibration, the Blackwell series is projected to grow significantly from a 61% share to 71%, further consolidating its market dominance.

The market needs to monitor whether Blackwell products can secure effective factual validation orders to establish a more favorable market position.

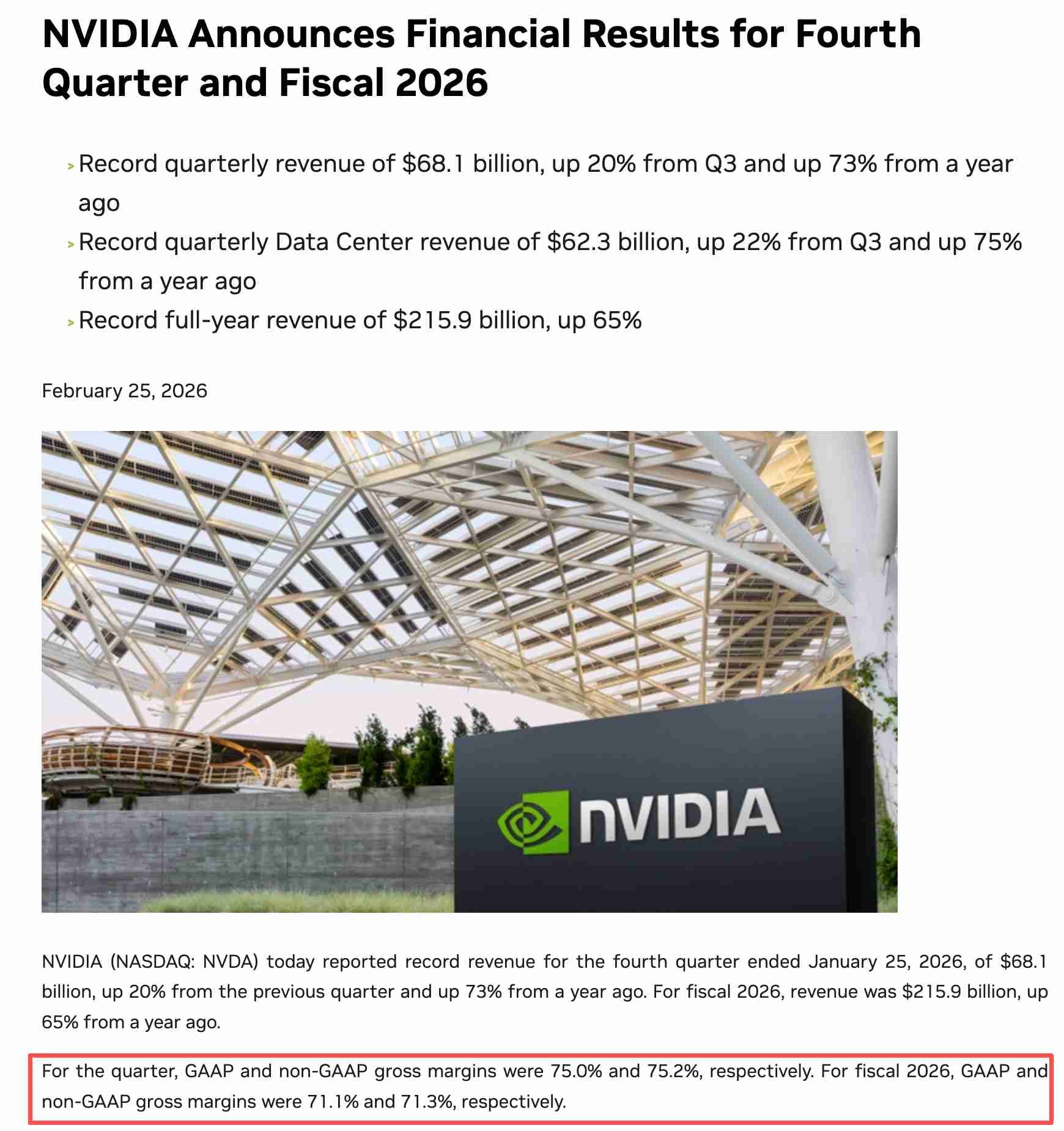

[NVIDIA Announces Financial Results for the Fourth Quarter and Full Fiscal Year 2026; Source: NVIDIA Official Website]

Regarding gross margin, the corporate figure for the previous quarter was 75%, with first-quarter guidance set at 71% to 72%; external expectations suggest that the actual gross margin for this earnings report will fall within the 73% to 75% range.

If the gross margin shows a significant downward shift, the market may interpret it as capacity bottlenecks or pricing pressures eroding profitability.

Structural Earnings Erosion from Export Controls on China

Despite earlier signals of easing restrictions on the H200 following Trump's visit to China, the Chinese market has yet to generate significant orders.

Export restrictions are evolving from a one-time loss into a continuous drain. In the previous quarter, H20 products recorded $4.6 billion in sales before new export licensing regulations took effect, but Nvidia recognized $4.5 billion in charges related to inventory write-downs and purchase commitments, with an additional $2.5 billion in orders left undeliverable.

Excluding the $4.5 billion non-recurring charge, non-GAAP gross margin would have reached 71.3%, compared to just 61.0% on a post-charge basis. Nvidia expects export bans to result in a cumulative revenue loss of approximately $15 billion over the next six months. In the long term, U.S. export controls are accelerating the shift among Chinese customers toward domestic alternatives.

According to the "2026 China AI Computing Chip Market Research Report," Nvidia's market share in China has plummeted from a near-monopoly two years ago to approximately 8%. The inference performance of Huawei's Ascend 950PR is now roughly three times that of Nvidia’s H20, and Huawei’s AI processor business reached $7.5 billion in revenue in 2025. This structural loss in the Chinese market is reshaping the global competitive landscape for AI chips.

Wall Street Bullishness and the Confirmation of Valuation Rationality

Wall Street consensus remains a "Buy." Most institutions still believe that NVIDIA's valuation is not significantly overstretched relative to its growth prospects. The current share price represents a forward P/E of approximately 45x, with a PEG ratio of only about 0.63, well below the conventional premium threshold for high-growth tech stocks.

Market analysis indicates that NVIDIA's immense pricing power has yet to be fully reflected in its stock price, and its current valuation does not adequately account for its central role in the ongoing AI revolution.

For investors, a key focus in this earnings cycle is whether the AI infrastructure cycle supporting NVIDIA's high valuation has reached a critical threshold of marginal deceleration.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.