Adobe Spends $25 Billion on Stock Buybacks to Counter AI Disruption Anxiety, Should Investors Buy?

AI Podcast

Adobe announced a $25 billion share buyback program, valid through April 2030, to address market concerns regarding AI disruption. Despite a significant stock decline over two years due to AI-native competitors, Adobe reported record Q1 fiscal 2026 revenue and operating cash flow. Structural challenges include AI's impact on its business model and CEO transition uncertainty. The company is accelerating its AI strategy with new platform launches and partnerships. Analysts maintain a 'Buy' consensus with a price target of $321.38, though some institutions have lowered targets. Long-term investors may find the current valuation attractive given strong cash flows and identifiable catalysts, but caution is advised regarding growth slowdowns or leadership uncertainties.

TradingKey - On April 21 local time, software giant Adobe (ADBE.US) announced a share buyback program of up to $25 billion, which will repurchase up to $25 billion of company stock over the next four years, with the authorization valid through April 2030.

[Adobe announces buyback program, Source: Adobe investor relations]

As of that day's close, Adobe shares were trading at $247.18, with a total market capitalization of approximately $110 billion. The $25 billion buyback represents about 23% of its market value. Boosted by the news, Adobe rose nearly 3% in pre-market trading on Wednesday.

Funding Buybacks to Address "AI Disruption" Anxiety

This plan is Adobe's latest move to counter the impact of AI. Adobe's stock price has fallen for more than two consecutive years, dropping approximately 25% and 21% in 2024 and 2025, respectively. So far in 2026, it has already fallen by more than 29%, representing a cumulative decline of nearly 60% from its 2024 peak. On April 10, the share price touched $224.13, its lowest level since January 2019.

This sustained sell-off stems from deep market concerns regarding AI-native companies disrupting traditional software business models. Adobe's business model, built over four decades, was founded on the 'scarcity of professional expertise,' which the explosion of AI tools is rapidly eroding, dealing a continuous blow to Adobe's moat.

Tools such as OpenAI's Sora and Midjourney allow users to generate high-quality visual content without relying on Adobe's high-priced professional software; Figma has also released several AI-driven tools that directly compete with Adobe's core product lines.

Against the backdrop of the continuous impact of AI tools, Adobe Chief Financial Officer Dan Durn stated in a release:

'This new buyback authorization directly underscores our confidence in the company's strong cash flow and our commitment to creating long-term value for our investors.'

[Adobe Q1 earnings disclosure, source: Adobe Investor Relations]

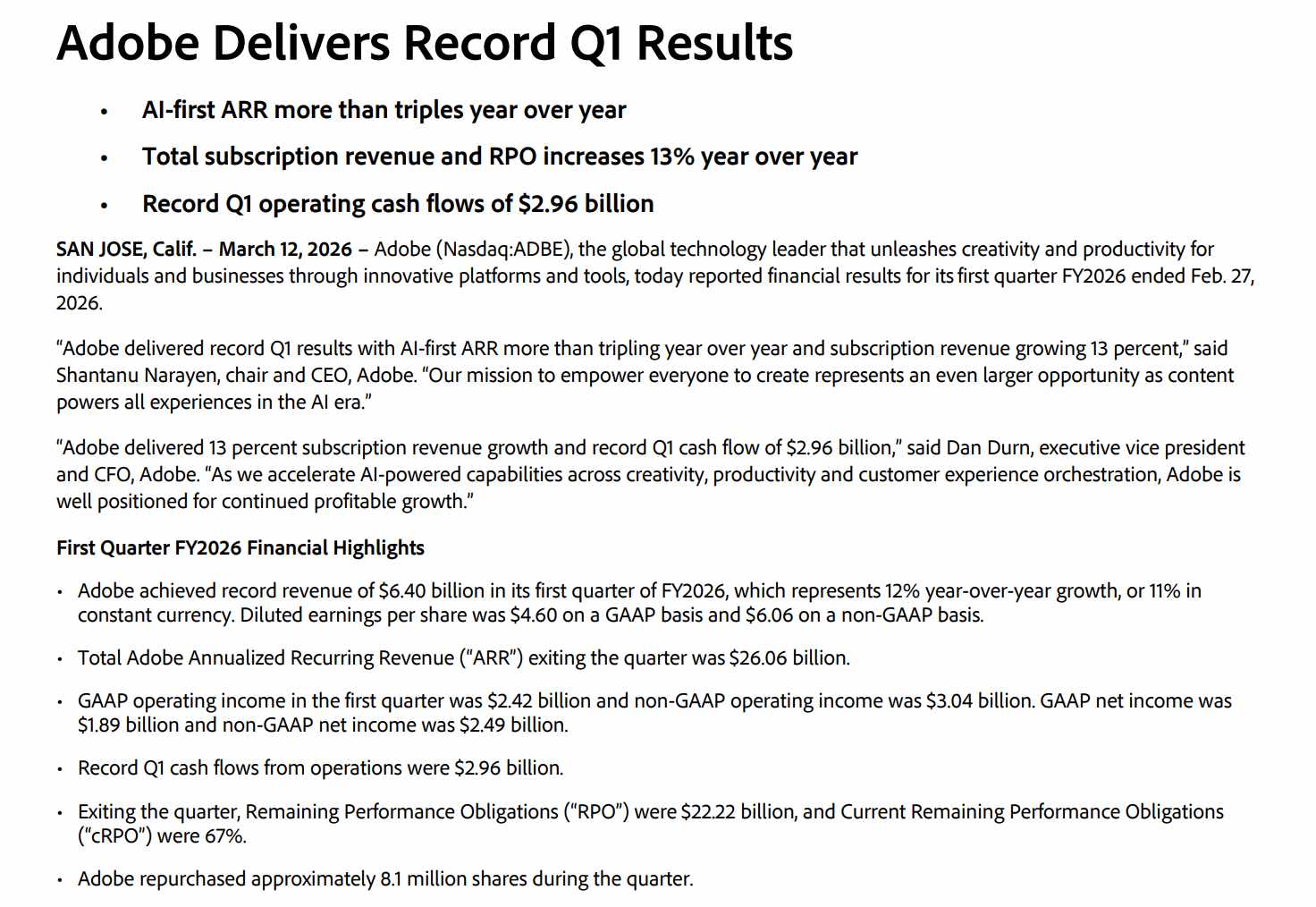

Dan Durn's confidence is backed by solid financial data: in the first quarter of fiscal 2026, Adobe reported revenue of $6.4 billion, up 12% year-over-year, setting a new single-quarter record; operating cash flow reached a record $2.96 billion, and total annualized recurring revenue reached $26.06 billion.

Uncertainties Surrounding Structural Challenges Persist

While the scale of its buyback program may soothe the market, the structural challenges facing Adobe remain unresolved, namely the narrative of AI disruption and the CEO transition.

The AI paradox is the core dilemma for Adobe. Although the company's proprietary generative AI model, Firefly, has generated some asset-related gains, it has not translated into higher subscription revenue for its traditional tools.

The paradox lies in the fact that as AI becomes more powerful, the value of each unit of work decreases; as AI tools become more ubiquitous, the premium for professional expertise diminishes.

The CEO transition is another source of strategic uncertainty. On March 12, Shantanu Narayen, who has served as CEO for 18 years, announced he would officially step down once a successor is named. Market research analysts noted that the transition raises questions regarding the company's strategic continuity and its pace of innovation.

[Analyst Ratings and Price Targets, Source: TradingKey, Refinitiv]

According to Refinitiv data, the analyst consensus rating is a 'Buy.' The average price target is approximately $321.38, implying an upside of about 30% from current levels.

However, some institutions have recently lowered their price targets; TD Securities cut its target from $400 to $310 on April 22, while UBS lowered its target from $290 to $260, reflecting a degree of divergence on Wall Street regarding Adobe.

Beyond buybacks, Adobe is accelerating its AI strategy to prove its long-term value. On April 21, at the Adobe Summit in Las Vegas, the company launched 'CX Enterprise,' a next-generation AI platform that integrates AI agents and development tools. It has established partnerships with Amazon, Anthropic, Google, Microsoft, OpenAI, and NVIDIA, aimed at helping customers automate and personalize digital marketing functions.

Is Now a Good Time to Buy Adobe?

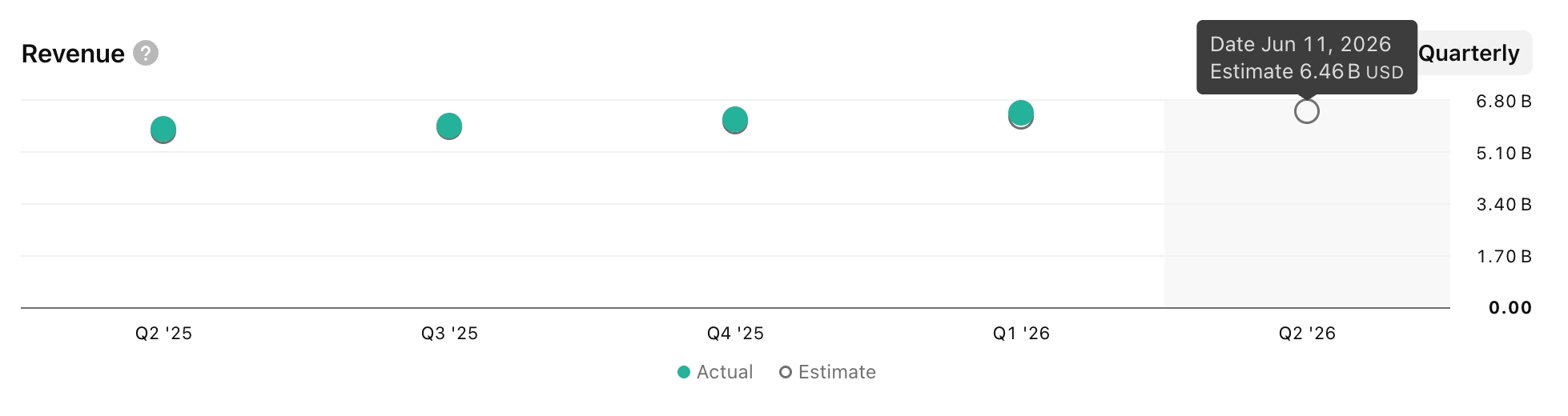

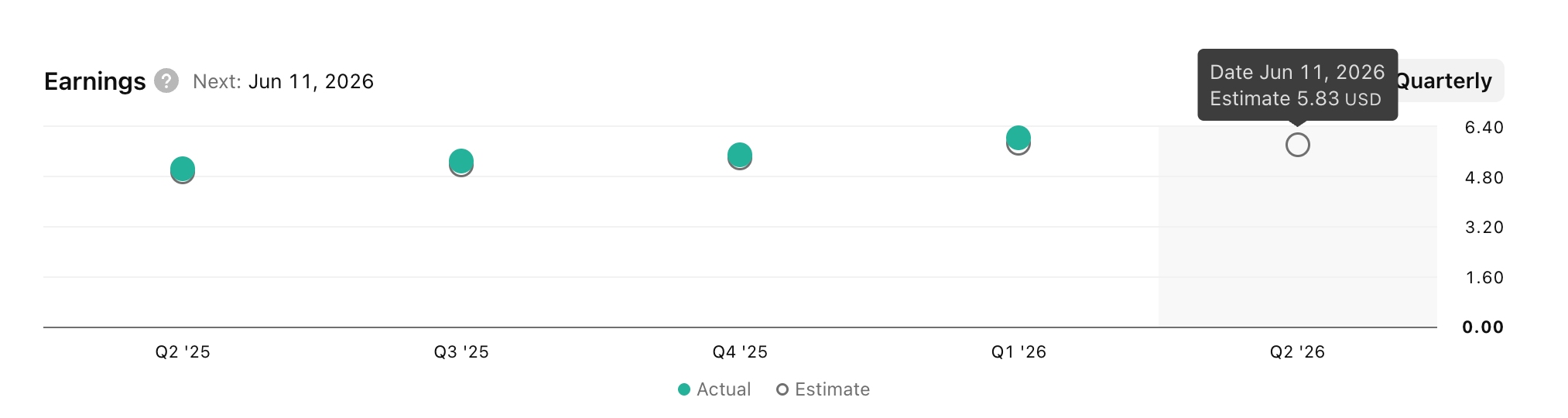

On June 11, ET, Adobe is set to release its Q2 2026 earnings report, with estimated revenue of $6.46 billion and expected earnings per share (EPS) of $5.83. Judging from past reports, unless results significantly beat expectations or provide relatively clear guidance, performance that merely meets expectations is unlikely to gain market approval.

[Adobe Q2 Earnings Forecast, Source: TradingView]

Previously, lackluster results have led to declines in Adobe's stock price, suggesting that the market has already priced in the new growth drivers brought by the company's AI initiatives.

Adobe's stock price is currently at multi-year lows, and market expectations for its future prospects appear far worse than its current condition. Over the past two years, earnings misses combined with high uncertainty have provided long-term investors—who are willing to wait for returns—with an attractive entry point into this cash-rich company.

Long-term investors expect Adobe to maintain double-digit growth and integrate AI capabilities into its products, thereby enhancing customer engagement and increasing average revenue per user (ARPU). Consequently, compared to its peers, Adobe is well-positioned for a positive valuation rerating driven by sustained growth and stable revenue over the coming years.

However, caution is advised if growth slows for several consecutive quarters or if there is uncertainty regarding corporate leadership.

Overall, the investment thesis for 2026 remains constructive, based on historically low valuation multiples, strong cash flows, and easily identifiable catalysts that outweigh the known risks in current investment decisions.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.