Storage Giants’ Profits Soar but Valuations Languish, Have Memory Chips Really Entered a Supercycle?

AI Podcast

Memory chip giants like Samsung and SK Hynix are experiencing record profits driven by AI demand, outperforming even TSMC. Despite strong stock gains, their valuations remain low compared to AI chip leaders like Nvidia, sparking debate on industry cyclicality. Skeptics cite historical volatility, while bulls point to long-term supply agreements and co-design with AI accelerators as indicators of a structural shift, weakening traditional boom-and-bust cycles. Sustained structural growth over multiple periods is deemed necessary to convince the market of a valuation rerating.

TradingKey - Driven by robust AI demand, memory chip giants are seeing an unprecedented profit explosion; however, their capital market valuations stand in sharp contrast to those of AI chip leaders, sparking intense debate over whether the industry has entered a "supercycle" and moved past the historical pattern of alternating boom-and-bust cycles.

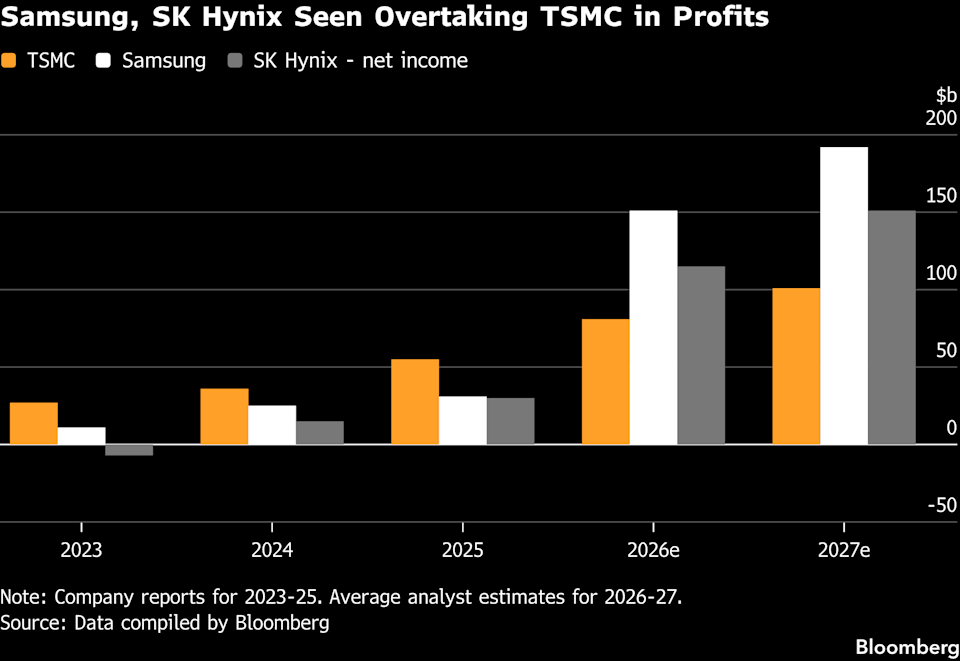

Market data shows that net profits for Samsung Electronics and SK Hynix are projected to surge by 400% and nearly 300% respectively this year, significantly outpacing Taiwan Semiconductor Manufacturing Co. ( TSM )'s growth of approximately 50%. In terms of profit scale, the full-year net profit forecasts for Samsung ($151 billion) and SK Hynix ($115 billion) both exceed TSMC's $81 billion.

Meanwhile, in terms of stock performance, memory stocks have shown strong gains. Over the past year, Samsung's stock price has risen by a cumulative nearly 300%, while SK Hynix has surged by more than 600%, compared to TSMC's gain of roughly 140% during the same period.

However, at the valuation level, the forward P/E ratios for these two memory giants are less than 6x, while U.S.-based Micron Technology ( MU) and Japan's Kioxia Holdings are also valued at less than 10x, whereas TSMC is near 20x and Nvidia is as high as 22x.

The Memory Chip Valuation Debate

Skeptics argue that the low valuations of memory chip stocks are justified, given that the industry's profitability has historically been volatile and tends to fluctuate with macroeconomic cycles.

"To some extent, we are in a new stage of development for the memory chip industry," commented Jorry Noeddekaer, London-based Head of Global Emerging Markets and Asia at Polar Capital, though he also admitted, "We do not agree with the view that the memory industry will henceforth break free from cyclical fluctuations."

Christine Phillpotts, an emerging markets equity portfolio manager at Ariel Investments in New York, pointed out that the core of the current market debate is how quickly the supply side can keep pace with demand growth. Reflecting on past cycles, supply often over-expanded during periods of weak demand, "so this is also a key risk factor we are monitoring."

Noeddekaer, who manages over $40 billion in assets, revealed that his funds have trimmed some positions during the strong rebound in the memory sector. In his view, the current risk-reward ratio for memory stocks is no longer as attractive as it was at the start of the cycle; by contrast, TSMC possesses a "more structural growth foundation" and faces less market competition.

Phillpotts maintains a similar level of vigilance, believing the essence of the market controversy is the alignment between the speed of supply expansion and demand growth. The lesson of supply expanding ahead of demand in previous cycles has led her to list the pace of supply as a key risk item for monitoring.

They believe the memory industry's profitability is highly dependent on macroeconomic cycles; once demand slows, the previously expanded supply often triggers a price collapse.

Even though Noeddekaer acknowledges that the memory industry is in "a sort of new paradigm," he still does not believe the sector can completely escape cyclical volatility. He further emphasized that TSMC's growth logic is more structural and its competitive pressure is lower, leading his portfolio to favor the latter.

However, investors bullish on a valuation rerating for the memory sector firmly believe that the rise of AI is reshaping the industry's underlying business model.

Dave Mazza, CEO of Roundhill Investments, pointed out that memory technology is now deeply integrated into the technological evolution of AI accelerators, with the co-design process directly established. He further mentioned that memory companies are increasingly signing long-term agreements with hyperscalers, a trend that is fundamentally weakening the industry's inherent cyclical characteristics.

Molly Pieroni, President of Texas-based Yacktman Asset Management, holds Samsung preferred shares but has not established a position in Nvidia due to its high valuation. In her view, even if Samsung's performance is mediocre, it is enough to support its current share price; even if its market value were to double, it would still have a significant valuation advantage over its peers.

Currently, strong AI-driven demand has spread from high-bandwidth memory (HBM) to broader memory categories such as DRAM and flash. Market conditions of supply shortages and rising prices have further strengthened the bulls' confidence in the sustainability of demand.

Reshaping the Cyclical Logic of the Storage Industry

Tom Tully, a portfolio manager at Aperture Investors in New York, noted that the cyclicality of earnings in the memory industry has persisted throughout its history, and the market requires sufficient time before it truly believes the current high returns are sustainable.

Many investors believe that once there is substantial evidence proving that earnings growth in the memory industry stems from structural drivers rather than cyclical dividends, its valuation is expected to converge toward those of AI chip leaders.

Dave Mazza, CEO of Roundhill Investments, stated that memory chips are now deeply tied to the technology roadmaps of AI accelerators, with co-design spanning the entire R&D process. More importantly, an increasing number of memory companies are beginning to sign long-term supply contracts with cloud service giants, a trend that is fundamentally weakening the industry's cyclical characteristics.

SK Hynix is currently in talks with Microsoft ( MSFT) and Google ( GOOGL) regarding multi-year DRAM supply agreements, which include prepayment clauses and are seen as a hallmark signal of the industry's business model transformation. Samsung Electronics has also explicitly stated that it is gradually shifting its supply contracts, previously based on annual and quarterly terms, toward long-term agreements of three to five years.

It is understood that while Samsung still retained some quarterly contracts last year, all new contracts for core customers starting this year have adopted a long-term structure of at least three years, showing a clear shift in operational strategy toward a long-term contract model.

SK Hynix's approach to long-term contracts is even more aggressive; it is currently negotiating a five-year general-purpose DRAM supply agreement with Google, aiming to improve capacity allocation efficiency and shipment stability by locking in long-term orders.

As the core supplier of Google's fifth-generation High Bandwidth Memory (HBM3E), SK Hynix also plans to use exclusive supply rights for next-generation HBM products as leverage to extend the existing partnership by another two years, further deepening their integration in the AI infrastructure space. Industry insiders expect contract details to be finalized in the first half of this year.

SK Hynix is set to release its earnings report on Thursday, while Samsung's report is scheduled for the end of the month. However, the market generally believes that data from just one or two reporting periods will still be insufficient to completely remove the cyclical label from the memory industry; only sustained structural growth over multiple rounds can truly reshape its valuation logic.

Tom Tully emphasized again that the historical inertia of memory industry profits fluctuating sharply with the cycle is very strong, noting that "the market needs time before it truly believes these high returns can continue."

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.