Nvidia Q4 Earnings Preview: AI-Driven Growth Versus Market Expectations

AI Podcast

NVIDIA's Q4 FY2026 earnings report, due February 25, is a key indicator for the AI boom. Consensus forecasts revenue of $66.11 billion and EPS of $1.53, up 68% and 72% YoY respectively. Demand for AI infrastructure, next-gen chips like Blackwell, and data center spending are expected to drive strong results. Analysts note investor focus is shifting to 2027 revenue visibility, competitive pressures, and the pace of capacity expansion for new chips. While stock performance post-earnings has been mixed, long-term trends remain positive, with analysts maintaining "Buy" ratings and high price targets.

TradingKey - NVIDIA ( NVDA) will release its fourth quarter fiscal 2026 earnings report after the U.S. market closes on February 25. Currently, the world is in a period of rapid AI development, and market discussions regarding a capital expenditure bubble are intensifying.

Against this backdrop, NVIDIA's earnings report is not just a test of its business performance but is also seen as a core bellwether for the sustainability of the global AI boom.

Due to growing demand for AI infrastructure, increased shipments of next-generation chips, and sustained momentum in data center spending, the market generally predicts that NVIDIA will deliver another stellar earnings report and issue optimistic future guidance.

According to FactSet forecasts, NVIDIA's fourth-quarter revenue is expected to reach $66.11 billion, a 68% year-over-year increase, while earnings per share (EPS) is projected at $1.53, up 72% from last year. These figures indicate that the company continues to maintain robust growth within the industry.

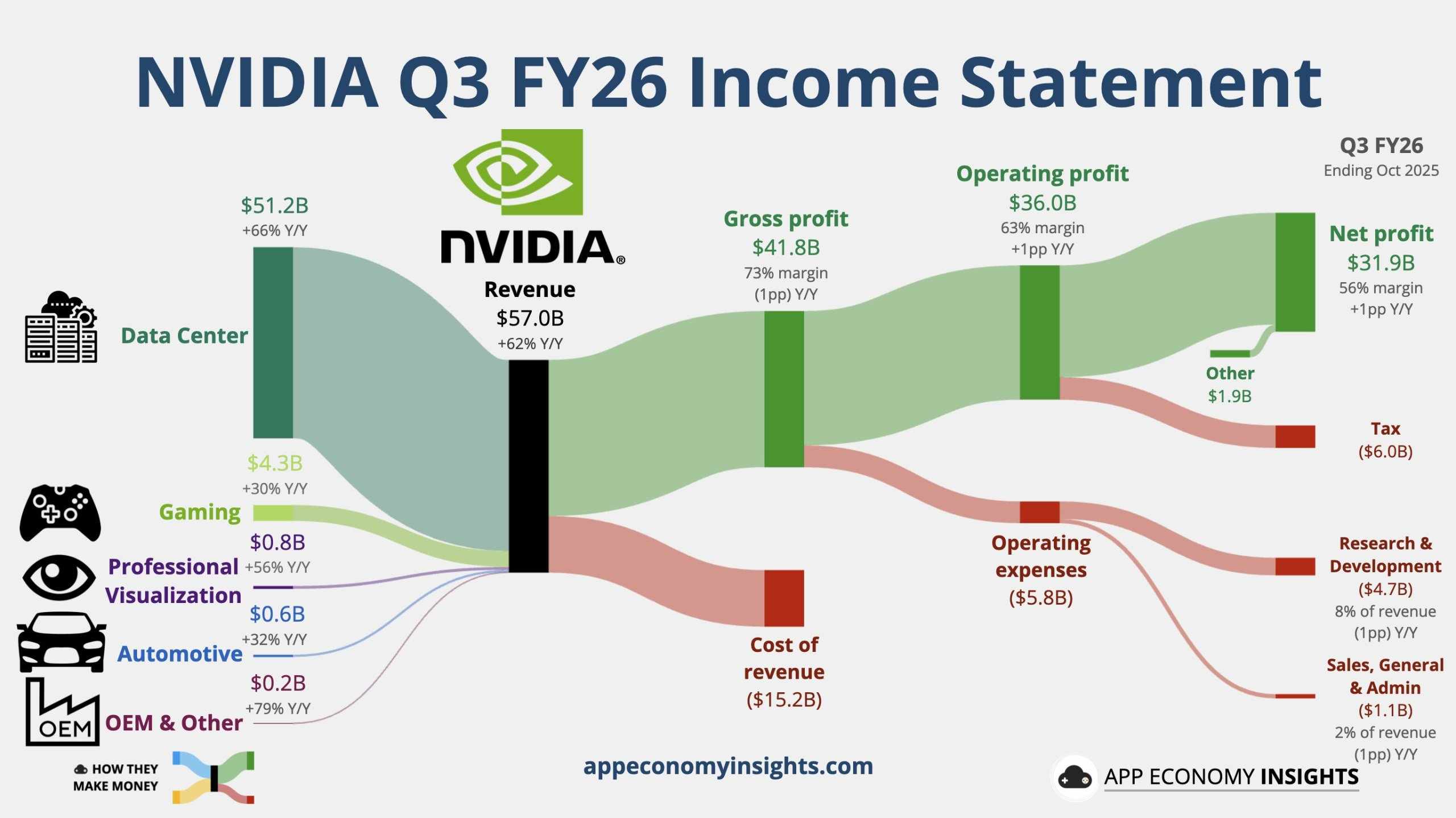

Third Quarter Performance Review

In the previous quarter, NVIDIA achieved revenue of $57.01 billion, a 62% year-over-year increase. The company's earnings guidance was $52.92 billion to $55.08 billion, while actual performance exceeded analyst expectations. Adjusted earnings per share (EPS) reached $1.30, up 60% year-over-year and higher than the $1.26 expected by analysts. The adjusted gross margin was 73.6%, slightly below the 74.0% analyst estimate.

In addition, data center revenue soared to $51.2 billion, a 66% year-over-year increase, while gaming and AI PC business revenue reached $4.3 billion, up 30%. Other segments, such as professional visualization and autonomous robotics, also achieved significant revenue growth.

Innovative Chips Driving Growth

The Blackwell chip, hailed as NVIDIA's "most powerful AI chip" ever, offers inference speeds 25 times faster than the previous generation. Since its launch, order volume has grown steadily, with total orders for fiscal 2026 reaching $500 billion. It now accounts for two-thirds of NVIDIA's data center revenue, becoming the core driver of the company's performance growth.

UBS expects Blackwell to contribute approximately $9 billion in revenue this quarter, providing significant support for a potential earnings beat. However, cost control remains key; if cost increases exceed market expectations, it could lead to a decline in gross margins, thereby heightening concerns over profitability.

Meanwhile, the Rubin chip represents NVIDIA's latest generation architecture and is seen as a vital pillar for growth over the next 2-3 years.

At the previous CES exhibition, NVIDIA announced that the Rubin chip has entered the production phase and is expected to gradually ramp up output in the second half of 2026.

Goldman Sachs expects initial shipments of the Rubin chip in the third quarter, with production significantly increasing in the fourth quarter and beyond. The market will focus on the speed of capacity expansion. Goldman Sachs noted that current stock prices already relatively fully reflect 2026 earnings growth, and further outperformance will depend on strengthening revenue expectations for 2027.

Analyst Perspectives

Goldman Sachs ( GS) noted that investor focus is shifting from short-term performance to the visibility of 2027 revenue. Meanwhile, Goldman Sachs is closely tracking changes in demand from non-traditional customers, the competitive landscape with ASICs and AMD ( AMD ), and potential contributions from the Chinese market.

Based on the strong performance of TSMC ( TSM) and SK Hynix, as well as upward revisions in capital expenditure forecasts by U.S. cloud companies, Goldman Sachs maintains a "Buy" rating on NVIDIA with a price target of $250. Although Goldman Sachs expects this quarter's results to potentially beat estimates and lead to a guidance hike, it also cautioned that market expectations are already quite high, raising the bar for a positive surprise.

UBS ( UBS) raised its price target for NVIDIA from $235 to $245 and reiterated a "Buy" rating. Analyst Timothy Arcuri noted that while skepticism regarding the sustainability of growth and margins persists, supply chain signals are optimistic, complemented by the positive backdrop of the upcoming GTC conference.

KeyBanc analyst John Vinh reiterated an "Overweight" rating with a price target of $275, noting that improvements in the Chinese market could provide significant support for quarterly results. He emphasized that continued shipments of Blackwell and H200 to China, along with memory shortages, are key factors affecting performance. The sustained demand growth for Blackwell is a major driver of the quarterly performance.

Stifel analyst Ruben Roy also stated that his outlook for NVIDIA's fourth quarter of fiscal 2026 is largely consistent with three months ago.

Roy noted that despite concerns about the sustainability of AI infrastructure spending, NVIDIA remains in a "clear trend of accelerating demand." Based on communications with management and hyperscale cloud service providers, he expects potential upward revisions to market estimates following the fourth-quarter report.

Post-Earnings Stock Performance

Current options pricing suggests that traders estimate NVIDIA's stock price could see swings of up to 6% this week, clearly influenced by the upcoming earnings release.

However, despite NVIDIA's typically excellent performance, its stock price does not always rise accordingly. As the market becomes accustomed to "surprises," their marginal effect is diminishing.

Jay Woods, Chief Market Strategist at Freedom Capital Markets, stated that the market's reaction to the earnings report may be "more of a shift in market psychology."

In the past four quarters, even with three earnings beats, NVIDIA's stock price has typically fallen the day after the earnings release. However, in the following months, the stock price often continues to recover and reach new highs.

David Morrison, Senior Market Analyst at Trade Nation, optimistically predicts that the latest earnings report could drive NVIDIA's stock price higher. He stated that the market will focus on data center revenue, cloud computing spending, and margins.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.