Amazon Earnings Preview: When AWS Demand Is Real, Is the Market Underestimating AI Capital Expenditure Returns?

AI Podcast

Amazon's Q4 earnings report on February 5th will be critical in assessing its new earnings cycle. Analysts project revenue near $211.44 billion, with potential for a beat if AWS capacity constraints ease. Demand for generative AI is high, but supply is limited. Amazon's massive capital expenditures, projected to exceed $150 billion in FY26 for AWS expansion, are viewed as necessary for AI infrastructure competition despite short-term free cash flow concerns. Cost controls and restructuring have improved operating profits, suggesting margin expansion potential. While macroeconomic risks exist, the market's focus will be on AWS demand, AI investment returns, and FY26 guidance, which could trigger a significant stock re-rating.

TradingKey - Amazon (AMZN) will report earnings after the market close on February 5, Eastern Time. Following several quarters of performance recovery, the market is beginning to re-examine a key question: as AWS demand accelerates again and AI capital expenditures enter a realization phase, is Amazon standing at the beginning of a new earnings cycle?

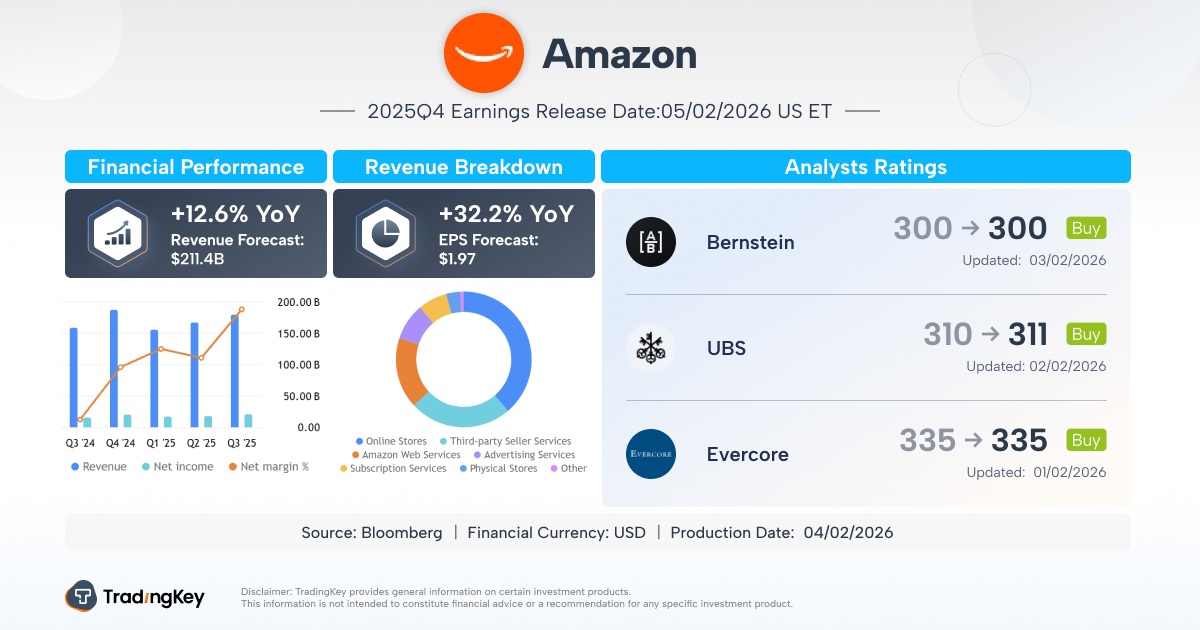

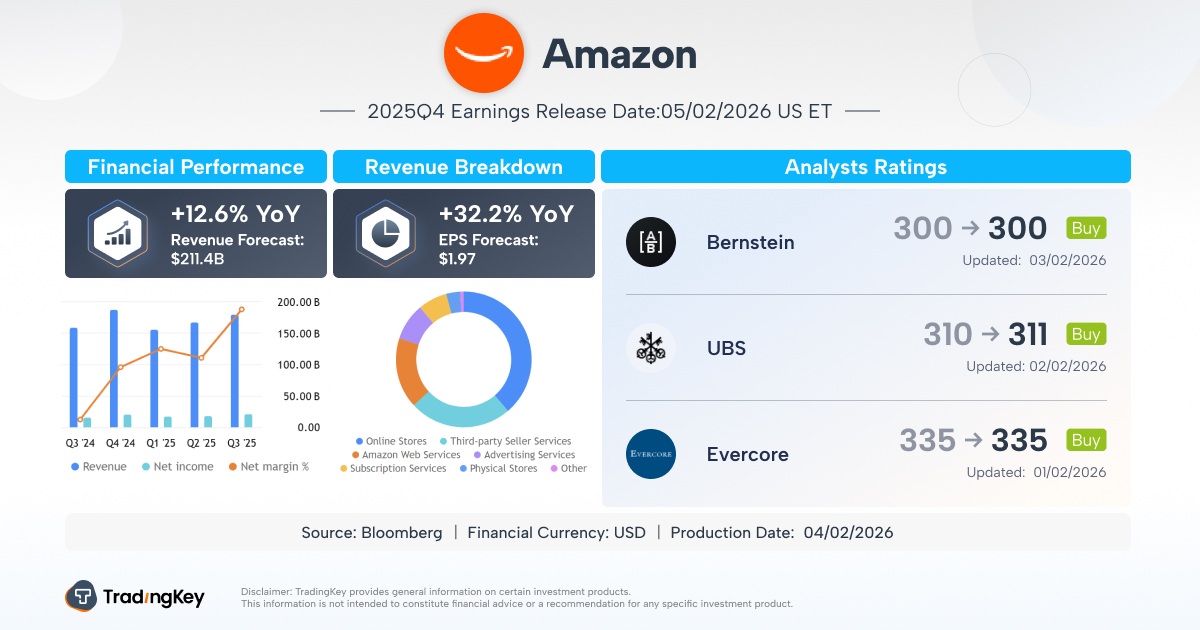

Market analysts expect the company's Q4 fiscal 2025 revenue to be approximately $211.44 billion, near the lower end of management's previous guidance range of $206 billion to $213 billion, representing a year-over-year increase of over 12%. This relatively conservative expectation leaves room for an earnings beat.

The Supply-Demand Structure of Aws Remains the Most Critical Variable in This Earnings Report

As Amazon's highest-margin business and strongest valuation anchor, AWS is currently facing a situation where demand exceeds supply. Demand from generative AI, model training, and enterprise cloud migration continues to be released, but the pace of bringing computing power and data center capacity online has become a short-term bottleneck.

This means that AWS's growth is not due to a lack of demand, but rather a "passive slowdown" caused by capacity constraints. If some new capacity is successfully released during Q4 and backlogged orders are converted more quickly, AWS revenue growth and profit contributions could exceed current market assumptions.

Directly related to this is the unprecedented capital expenditure cycle Amazon is currently pursuing. Market opinion on this is clearly divided. On one hand, massive investments erode free cash flow in the short term, which can easily be interpreted as financial pressure; on the other hand, this is the price of admission for the AI infrastructure competition.

According to market estimates, Amazon's capital expenditures for fiscal year 2026 could exceed $150 billion, ranking first among the "Magnificent Seven" tech giants, with the vast majority directed toward expanding AWS's computing power, networks, and data centers.

Changes on the cost side are also worth noting. Over the past year, Amazon has continued to advance organizational and workforce restructuring, compressing non-core costs through layoffs, process reengineering, and the introduction of more AI tools.

The effectiveness of this strategy is already reflected in the financial data: operating profits have surged over the past twelve months, indicating that economies of scale are re-emerging. If the Q4 report further validates the sustainability of cost controls, margin improvements will serve as a significant amplifier for EPS upside as revenue regains elasticity.

Current market concerns regarding free cash flow largely stem from capital expenditures in the AI sector. However, from a cyclical perspective, these concerns may be a misjudgment. Amazon's cash flow fluctuations have historically been highly correlated with its investment cycles.

Nova Capital believes, that market concerns over the deterioration of Amazon's free cash flow are therefore exaggerated, as future investment returns will be realized through the monetization of backlogged orders as capacity expands. Once the market recognizes this, the stock price will undergo an upward re-rating.

When capacity construction is completed and order realization accelerates, free cash flow often sees a significant rebound. Therefore, management's explanations regarding cash flow trends and investment return cycles in the Q4 report will directly influence the direction of market sentiment.

Management Guidance for Fiscal 2026 Could Trigger a Valuation Re-Rating

If the company expresses stronger confidence in AWS growth, AI commercialization, and margin improvement during the earnings call, the current relatively low forward valuation is expected to rise.

Based on market expectations of approximately $10.8 in EPS for fiscal 2027, applying a P/E ratio of about 29x suggests that the corresponding fair stock price still has nearly 30% upside potential. Such a combination of "growth leadership and low valuation" is rare among mega-cap tech stocks.

Of course, risks also exist. If the pace of returns on capital expenditures is slower than expected and free cash flow remains under pressure, the stock price may face short-term volatility; meanwhile, macroeconomic uncertainty could also affect the pace of enterprise cloud spending. However, from a longer-term perspective, these factors are more likely sources of volatility rather than signals of a trend reversal.

This Q4 report is not just a performance announcement; it is a critical window for the market to reprice Amazon's AI strategy.

The authenticity of AWS demand, the long-term return logic of capital expenditures, and the clarity of the growth path for 2026 will collectively determine the next direction for the stock price.

For investors, while noting short-term volatility, it is essential to remain focused on Amazon's commitment to AI investment and whether its future returns can be realized.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.