End of an Era: Warren Buffett Hands Over the Reins of Berkshire Hathaway — Can the Trillion-Dollar Empire Sustain Its Brilliance?

AI Podcast

Warren Buffett has stepped down as CEO of Berkshire Hathaway, succeeded by Greg Abel, while retaining his Chairman role. Over 60 years, Buffett transformed Berkshire, delivering a 6,100,000% total return, significantly outperforming the S&P 500. His value investing strategy, leveraging insurance float and focusing on quality businesses like Apple and Coca-Cola, defined his success. Abel's more pragmatic management style will guide Berkshire, though replicating Buffett's extraordinary investment returns presents challenges due to Berkshire's scale and current market valuations.

TradingKey - On December 31, 2025, local time, Warren Buffett, the 95-year-old 'Oracle of Omaha,' officially stepped down as CEO of Berkshire Hathaway (BARa), with Greg Abel, long considered his designated successor, formally taking over the CEO role. This colossal holding group, with a market capitalization exceeding one trillion U.S. dollars, officially embarked on a new chapter.

Although he has transitioned from the CEO position, Buffett will continue to serve as Chairman of the Board and retain a 'significant stake' in the company.

As ever, he emphasized his confidence in the company's future prospects, stating, 'Who knows what the future holds? But I think Berkshire is more likely to be around in 100 years than any company I can think of.'

A Sixty-Year Investment Legend

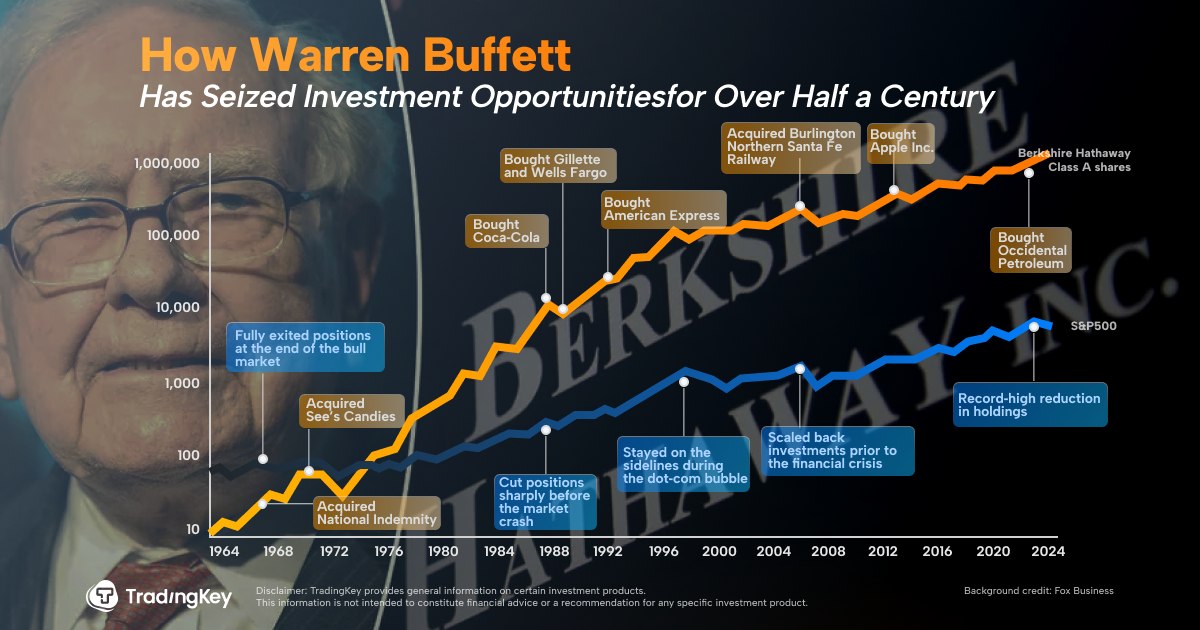

Since taking the helm of Berkshire in 1965, Buffett transformed a failing textile mill into a business empire encompassing multiple sectors, including insurance, railroads, utilities, technology, manufacturing, and consumer goods, boasting dozens of subsidiaries and nearly $400 billion in assets.

Under his sixty-year stewardship, the company's Class A shares soared from an initial $19 per share to over $750,000 by the end of 2025, delivering an astonishing cumulative return of approximately 6,100,000%.

According to statistics, since 1965, Berkshire has generated a total shareholder return of 6,100,000%, significantly outperforming the S&P 500 index, which recorded a gain of approximately 46,000% including dividends over the same period.

Comparing their annualized performance, Berkshire achieved an average compound annual growth rate of 19.9%, notably surpassing the S&P 500's 10.4%.

Buffett steered the company through countless market fluctuations, financial crises, and shifts in macroeconomic policy, consistently maintaining robust growth. Such sustained superior performance over such an extended period is a rarity in global investment history.

“If it was that easy to do again, somebody would be doing it,” Bill Stone, chief investment officer at Glenview Trust Company and a Berkshire shareholder, said. “You think about the duo that having Charlie Munger as your partner, it’s just hard to imagine that coming together again anytime soon.”

Core Investment Philosophy

Throughout his strategy, Buffett consistently adhered to the principles of value investing.

By acquiring high-quality insurance companies such as Geico and National Indemnity, he secured a stable and low-cost source of capital—known as 'float'—which became a crucial lever for deploying into other assets.

Utilizing this 'free capital,' Buffett focused on businesses with strong cash flow, stable business models, and reliable management. For instance, he invested in railroad giant BNSF, utility provider MidAmerican Energy (now Berkshire Hathaway Energy), and the ice cream brand Dairy Queen, which boasts a global network of stores.

Concurrently, his stock investments also astounded the market.

Between 2016 and 2018, Berkshire invested approximately $36 billion in Apple (AAPL) Inc., a position that subsequently appreciated to around $170 billion, becoming one of the largest technology stock holdings in history.

This transaction not only extended Buffett's successful logic of long-term quality asset portfolio construction but also further solidified his influence in the digital economy era.

Another highly emblematic example is his entry into Coca-Cola (KO) in 1988. An initial investment of nearly $1.3 billion at the time has now seen that holding's market value approach $30 billion, while simultaneously generating hundreds of millions of dollars in annual dividend income.

Similarly, his purchase of American Express (AXP) in the 1990s, also with an initial investment of $1.3 billion, now boasts a market value exceeding $45 billion and remains a core holding. Furthermore, Bank of America (BAC), Chevron (CVX), and rating agency Moody's (MCO) have all delivered consistent and substantial returns for Berkshire.

Proving Mettle Amidst Market Volatility

Buffett's success lay not only in identifying quality assets but also in his rational approach to market volatility.

In 1999, as the tech stock frenzy swept the market and the S&P 500 surged 21%, Berkshire's stock price fell by 20%. Confronted with skepticism, Buffett adhered to his principle of 'only investing in businesses he understood,' maintaining caution towards the dot-com bubble. This prudent stance was ultimately vindicated.

Similar scenarios played out multiple times throughout his career. He rarely chased fads, yet he consistently managed to replicate his successful model— strategically overweighing businesses with the highest probability of success and implementing small stop-losses on failed investments, and adeptly learning lessons from every mistake.

Buffett often emphasized that the goal isn't perfect judgment, but rather avoiding 'fatal mistakes'—especially refraining from rash actions when knowledge is limited or an industry is not fully understood.

“Warren, as chairman, will be an advisor to Greg, a cultural anchor, and a real long term thinker,” said Ann Winblad, managing director at Hummer Winblad Venture Partners and longtime Berkshire shareholder. “Will the company fundamentally change in its strategies? No. ..The culture of Berkshire Hathaway, which is what I’ve invested in, which is patient, long term, careful and decisive investing, will probably still remain.”

While Buffett's transition from the front lines indeed signals the formal end of an era, his influence will endure for a long time.

Lisa Schreiber, Associate Portfolio Manager at Gradient Investments, noted: 'He not only shaped Berkshire's operating philosophy but also profoundly influenced the mindset of global investors. Even today, the insights he offered decades ago remain highly relevant.'

The Handover Moment: Challenges and Opportunities for Abel

Since 2021, Greg Abel has progressively assumed responsibility for Berkshire's daily operations, earning him the moniker of 'behind-the-scenes COO' within the industry. As a manager with significant achievements in the energy sector, Abel has garnered widespread recognition for his development strategies in the utility and electric power industries. His management style is notably more pragmatic and proactive, a stark contrast to Buffett's 'hands-off' approach.

Cathy Seifert, an analyst at CFRA Research, pointed out: 'Abel employs a relatively traditional yet pragmatic and systemically supported development approach. He actively intervenes in senior personnel matters across multiple subsidiaries and pursues cross-divisional synergies. In the context of leading a large group with over 400,000 employees, this style may be more suitable for the new era's demands than a 'completely hands-off' approach.'

Abel, 63, was born in Edmonton, Canada, and graduated from the University of Alberta in 1984 with a Bachelor of Commerce degree. Early in his career, he worked for PwC, spending several years in its San Francisco office. He joined Berkshire in 1999 when the company invested in MidAmerican Energy and quickly rose through the ranks. In 2018, Buffett appointed him Vice Chairman of non-insurance operations; by 2021, Buffett formally announced that Abel would succeed him as CEO.

Analysts note that while Abel possesses excellent operational capabilities, replicating the extraordinary investment performance of the Buffett era will not be an easy task.

On the one hand, Berkshire's current immense size means that large, high-quality investment targets suitable for its scale are scarce.

As of the end of the third quarter of 2025, Berkshire held a record-high $381.7 billion in cash and equivalents. The judicious allocation of this enormous sum presents a significant challenge for Abel.

When global high-quality asset prices are generally elevated, large-scale position building becomes more cautious and complex. Furthermore, if the capital remains uninvested for an extended period, it will inevitably trigger a new round of market discussions regarding the company's capital efficiency and shareholder return policies.

On the other hand, replicating past 'Coca-Cola' or 'Apple'-esque miracles is even more challenging in the current environment of high valuations and rising interest rates.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.