Electric Vehicle War: Who Will Get the Future Ticket

Authors: Mario Ma, Viga Liu, Zico Xiao

TradingKey - Driven by the goals of global carbon peaking and carbon neutrality, the Electric Vehicle (EV) market has become an irreversible long-term structural trend. This trend transcends short-term economic cycle fluctuations, rooted in climate change policies, technological progress, and a profound shift in consumer preference toward sustainable energy. As transportation is one of the main sources of carbon emissions, EVs provide the core momentum for achieving an earlier emissions peak by reducing reliance on fossil fuels and improving energy efficiency.

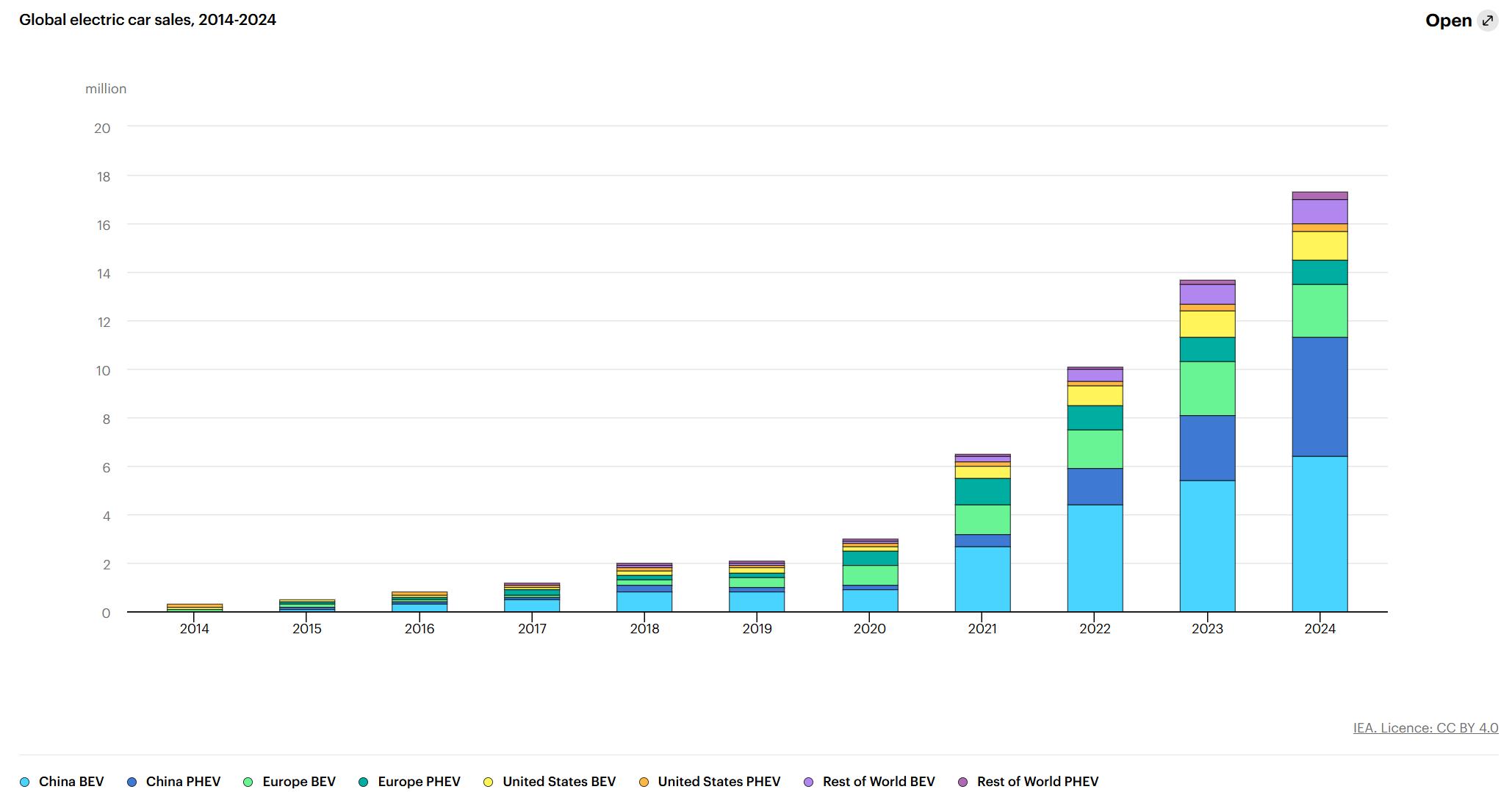

Over the past decade, the global EV market has experienced exponential growth, especially the explosive development after 2020, which can be called the "policy-driven phase." During this stage, strong government intervention and technological maturity formed a positive feedback loop, significantly shortening the popularization cycle of EVs. The rapid decline in battery costs was particularly crucial, enabling EVs to gradually move from a high-end niche to the mass market. China is undoubtedly the leader of this wave, contributing nearly two-thirds of global sales, with market penetration expected to reach 60% in 2025. More importantly, Chinese-made EVs, relying on their cost advantage, occupy approximately 70% of global production capacity. In contrast, the European market experienced a brief growth stagnation in 2024, with its market share stabilizing around 20%, but thanks to the European Union's impending tightening of carbon dioxide emission standards, it is expected to rebound to 25% in 2025. The US market, due to policy fluctuations and fragmented consumer preferences, saw its growth rate plummet from 40-50% in the previous two years to 8-10% in 2024. Although absolute sales are still growing (projected to reach 1.6 million units in 2025), the market share remains below 10%.

Looking ahead to 2025, global EV sales are projected to break the 20 million unit mark for the first time, accounting for over 25% of the new car market. Of this total, China is expected to contribute over 60%, while Europe and the US contribute approximately 25% and 10%, respectively. What is more noteworthy is that the EV market is transitioning from mere electrification to intelligence. The penetration rate of Advanced Driver-Assistance Systems (ADAS) is expected to exceed 70% in 2025, and the proportion of L3+ level autonomous driving models is projected to reach 15%. This marks the transformation of EVs from "green transportation tools" to "intelligent mobility platforms." Looking further into the future, the International Energy Agency (IEA) and Bloomberg New Energy Finance (BNEF) predict that the compound annual growth rate (CAGR) of EV sales will exceed 30% from 2025 to 2030, with sales reaching 40.1 million units by 2030 and market share approaching 50-60%. By 2035, the global EV fleet is estimated to exceed 380 million vehicles, and the market size will grow from $698.6 billion in 2025 to $1.19 trillion. Intelligence will become the dominant trend: by 2030, 90% of new EVs will be equipped with L4+ level autonomous driving features, and 80% of vehicles will achieve interconnectivity, completely reshaping the transportation ecosystem.

Therefore, the rise of the EV market is not just a victory for technology and policy, but also a microcosm of the global shift towards sustainable and intelligent transportation. This trend provides a broad stage for leading companies in the industry, especially companies like Tesla, Xiaomi, BYD, Nio, Li Auto, and Xpeng, each with unique characteristics in technological innovation, market deployment, and brand strategy. The following analysis will delve into the positioning, competitive advantages, and potential challenges of these companies in the global EV wave, helping investors to more clearly grasp the opportunities in this sector.

Source: IEA

1. Tesla

Tesla is, without a doubt, the benchmark for the entire electric vehicle industry. Founded in Silicon Valley in 2003, it has led the global EV revolution with disruptive innovation, dedicated to accelerating the world's transition to sustainable energy. Tesla has redefined the automotive industry with its disruptive electric vehicle models (such as the Model S, Model 3, Model Y, and Cybertruck), integrating cutting-edge technology, superior performance, and environmental concepts. The company also offers solar products, energy storage solutions, and autonomous driving technology, leading the revolution in smart mobility and clean energy. Through innovation and global influence, Tesla continues to shape the new landscape of future transportation and energy.

1.1. Market Share and Sales Volume

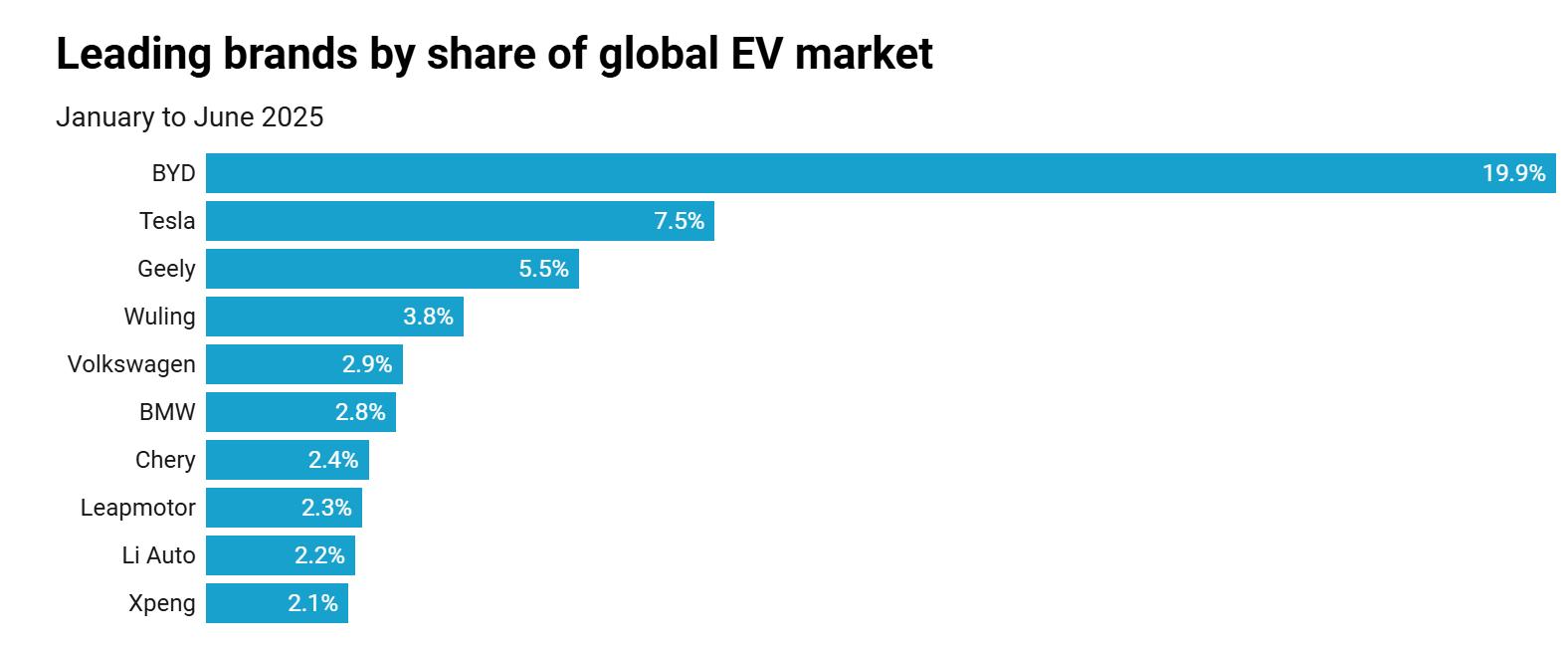

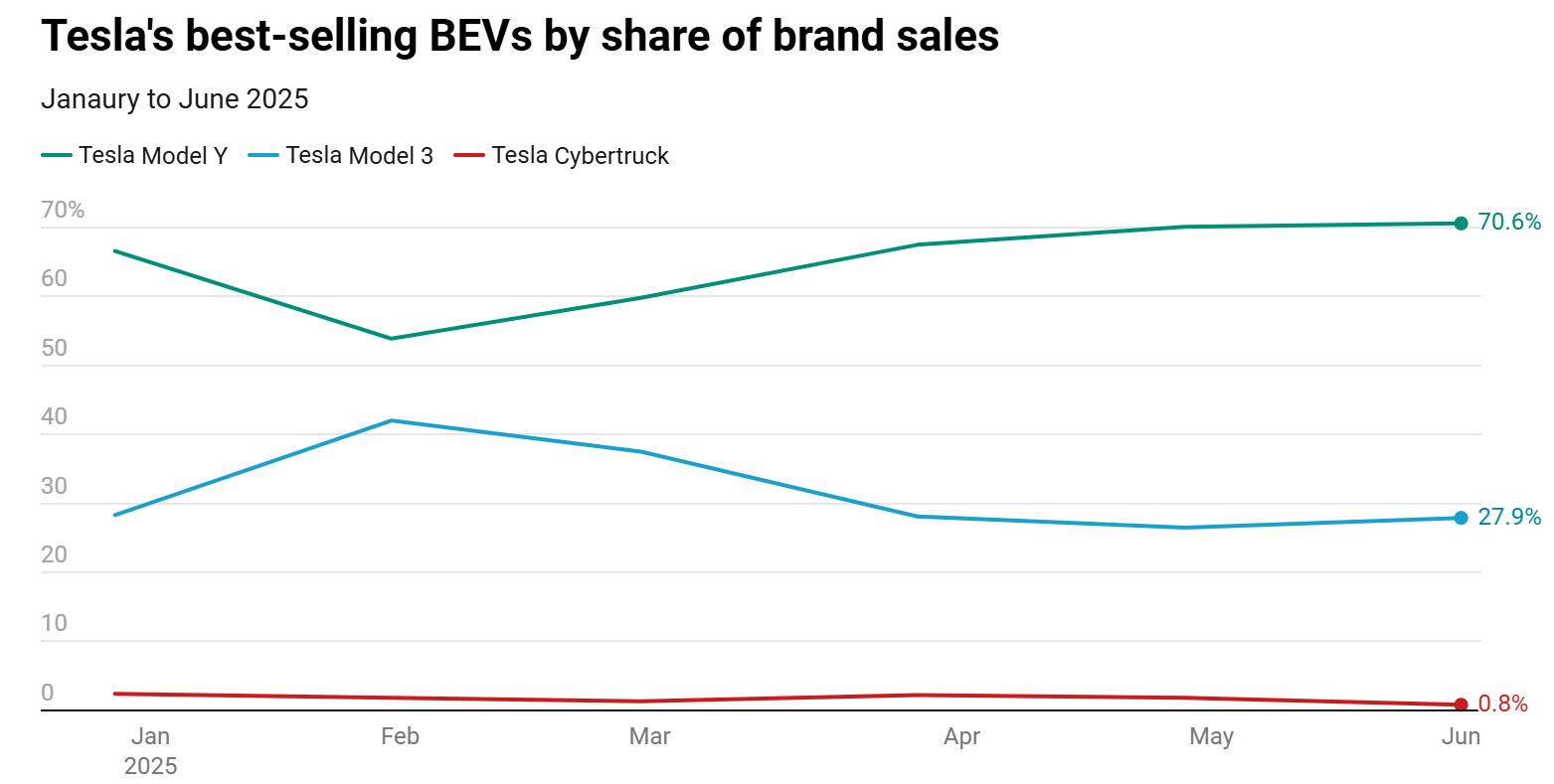

As of the first half of 2025, Tesla continues to maintain a leading position in the global electric vehicle market but faces increasingly fierce competition. According to the latest data, Tesla delivered 719,325 Battery Electric Vehicles (BEVs) globally, a year-over-year decrease of 13.1%. Of these, the Model Y accounted for 65.2% (469,143 vehicles), the Model 3 accounted for 31.6% (227,210 vehicles), and the Cybertruck accounted for 1.6% (11,225 vehicles). In the global electric vehicle market (including BEVs and Plug-in Hybrid Electric Vehicles, with total sales of 9,535,141 units, a year-over-year increase of 34.3%), Tesla's market share was 7.5%, a year-over-year decrease of 4.2 percentage points, ranking second globally, only behind BYD (19.9%). Nevertheless, thanks to its technological innovation and brand influence, Tesla remains a core player in the pure electric vehicle segment.

Source: autovistagroup

Source: autovistagroup

1.2. Cost and Profit Analysis

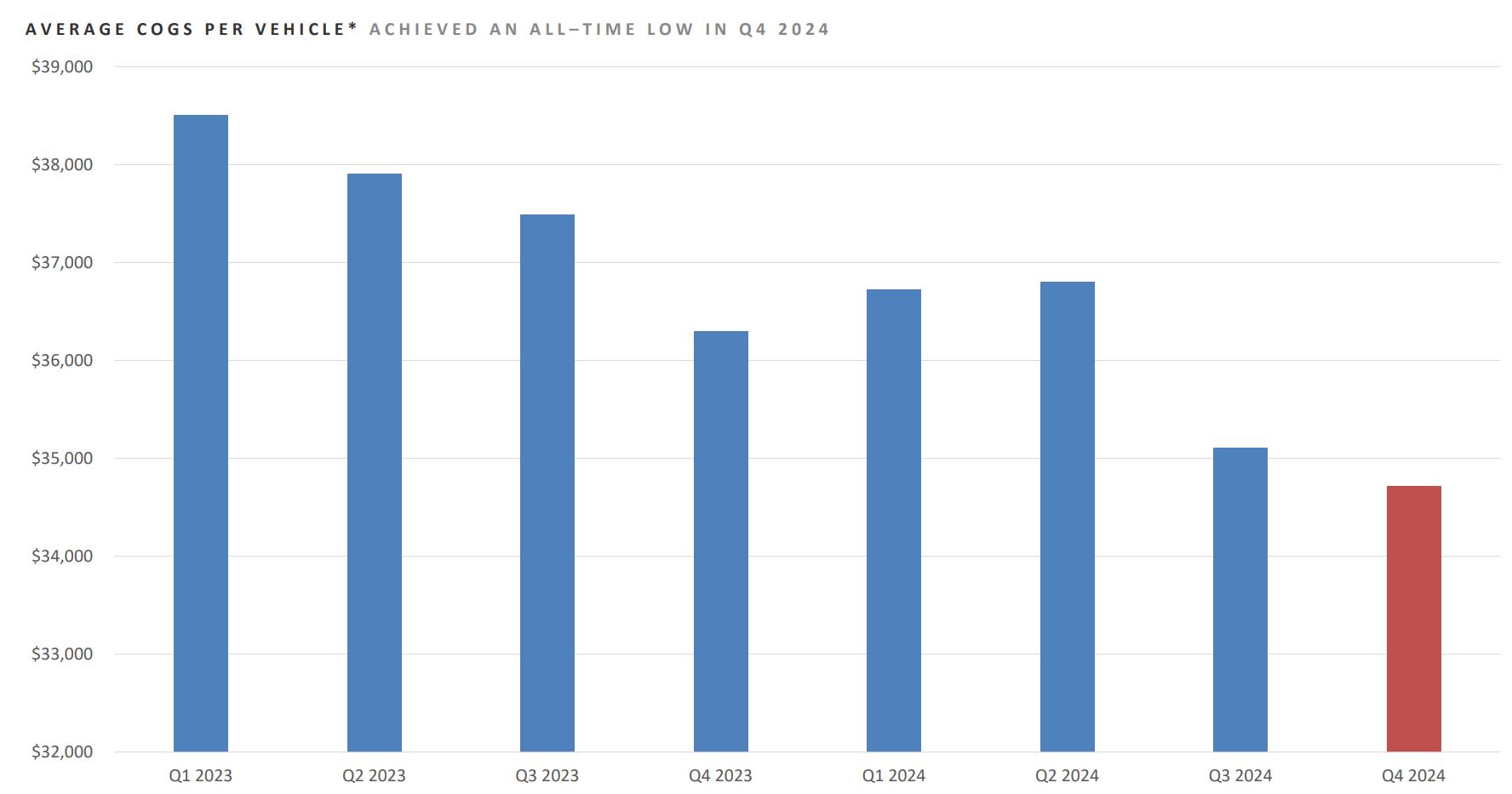

Supporting Tesla's market position is not only its sales volume but also its exceptional cost control and profitability. The cost per vehicle production is approximately $35,000, with the main components being the battery (30-40%), motor and drive system (15-20%), and software and electronics (10-15%). The highest proportion is the battery, highlighting the critical role of technological innovation. Thanks to the expansion of Gigafactory and the 4680 battery technology (with cost dropping from $128/kWh to $56/kWh, a 56% decrease), the cost per vehicle is continuously declining. As of Q3 2025, Tesla's average selling price per vehicle is approximately $43,000, with a gross profit per vehicle of $7,700, and a gross profit margin of about 17%, which is higher than the industry average (10-15%).

In the future, Tesla plans to deepen vertical integration, launch four variants of the 4680 battery and a new factory in Mexico in 2026, and further reduce battery costs by 20-30% and single-vehicle costs to below $25,000 by reducing supply chain dependence. These measures are expected to push the gross profit margin above 20%, facilitate the launch and mass production of the $25,000 model, double profits, and solidify its advantage in the competitive market.

Source: Tesla

1.3. Financial Status Analysis

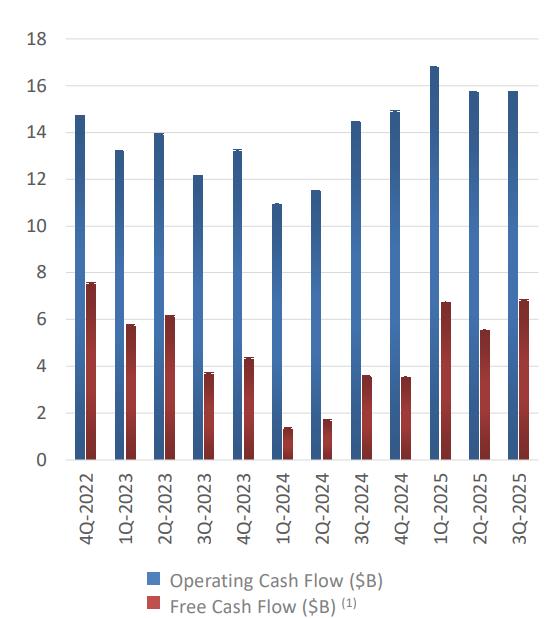

Tesla's market position is not only supported by its electric vehicle technology leading the industry, but also by its strong financial engine. Tesla's debt mainly stems from customer vehicle leases and financing leases for solar projects, rather than corporate bonds or bank loans. Total liabilities are approximately $13.8 billion, the debt-to-equity ratio is stably below 0.2, and the interest coverage ratio is nearly 14, demonstrating solid debt conditions with no significant interest burden. Operating cash flow is about $16 billion, and free cash flow is as high as $7 billion, reflecting strong profitability in its core business. Existing short-term liquidity is approximately $42 billion (including cash equivalents), and the current ratio is 2.1, which is sufficient to cover short-term liabilities and support future investments.

Looking ahead, with new factory production coming online and battery costs decreasing, Tesla is expected to continue optimizing its debt structure, and cash flow will be further strengthened. Combined with a low debt ratio, this provides flexibility for its investments in autonomous driving and robotics. Even with market fluctuations, the cash reserves are sufficient to cover all debt, solidifying its financial advantage.

Source: Tesla

1.4. Financing Capability

Tesla's financial stability (such as $42 billion in cash reserves and a debt-to-equity ratio of less than 0.2) provides it with a solid foundation, but its financing capability would become crucial should it encounter a cash flow crisis due to declining demand or intensifying competition. Currently, Tesla has obtained investment-grade ratings from major global credit rating agencies, which provides strong support for its fundraising in the global capital markets. Elon Musk, as the CEO and largest shareholder, possesses a net worth of $410 billion and the influence of over 200 million followers on the X platform, making him a "super fundraising machine." He has previously collateralized Tesla stock for loans (approximately $13 billion in loans in 2023), and should a crisis occur, he could further collateralize or sell a portion of his shares to inject cash into Tesla.

Musk's other ventures further reinforce this support: SpaceX (valued at $350 billion, with Musk holding 54% stake) could issue new equity or provide loans to indirectly inject capital; xAI (which secured $6 billion in funding) could share AI computing resources; Neuralink and The Boring Company could also collaborate across sectors, with their combined valuations potentially exceeding $400 billion. Although "blood transfusions" of this nature might spark shareholder controversy, Musk's inter-company synergy and innovative financing could help Tesla turn crisis into opportunity, thus solidifying its position as the industry leader.

1.5. Degree of Intelligence

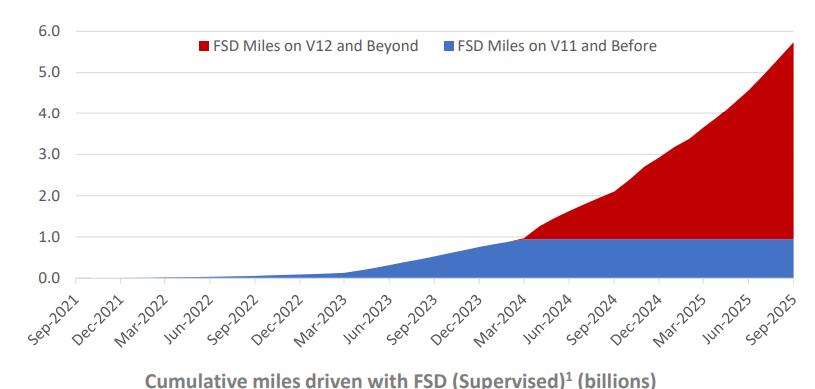

Tesla is at the critical inflection point of intelligent transformation, accelerating its evolution from an electric vehicle manufacturer into a leader in the AI era. This strategic leap is underpinned by its powerful financial strength and excellent financing capability, which provide solid support for its AI-driven long-term strategy. The technology ecosystem, centered on Full Self-Driving (FSD), is reshaping the global mobility landscape. Relying on an end-to-end neural network architecture and daily real-world fleet data accumulation of 15 million miles, Tesla integrates visual perception, decision planning, and execution control, leading a revolutionary breakthrough in the application of AI in the physical world.

1.5.1. FSD: The Core of Intelligence, Autonomous Leap Driven by End-to-End Neural Networks

FSD is the absolute engine of Tesla's intelligent transformation. The Beta v14 version, launched in 2025, fully adopts an end-to-end neural network architecture, completely breaking the traditional modular design and seamlessly integrating perception, planning, and control into a single AI model. This architectural change marks a critical leap for the system from Level 2 (supervised driver assistance) to Level 4 (high autonomy in specific scenarios). By the end of 2025, the cumulative driving mileage of FSD will exceed 6 billion miles, building the world's largest and most realistic training dataset. Safety data further demonstrates its leadership: the Autopilot accident rate is only once per 6.3 million miles, significantly lower than the human-driven accident rate reported by the US National Highway Traffic Safety Administration (NHTSA) (once per 700,000 miles), representing an approximately 9-fold improvement in safety. The end-to-end model in version v14 achieves the ability to process complex dynamic scenarios in real-time, including high-difficulty tasks such as unprotected left turns, yielding to emergency vehicles, and navigating around construction zones. Early tests show that the average intervention mileage reached 1,454 miles, a significant improvement from previous versions, with system behavior being more natural and closer to intuitive human driving.

Source: Tesla

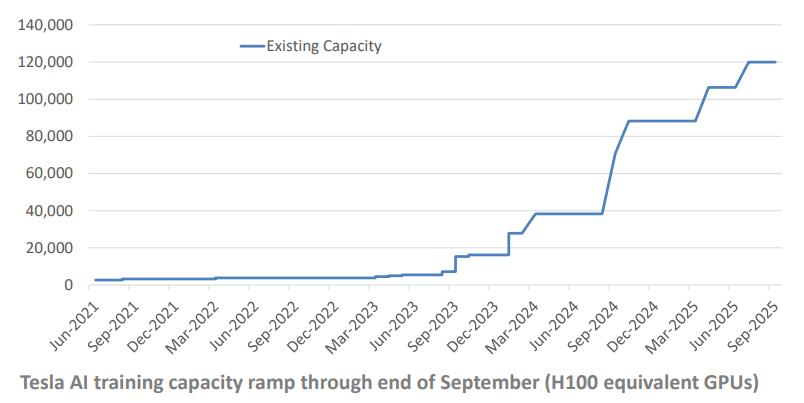

1.5.2. AI Infrastructure: Self-Developed Computing Power and Closed-Loop Chip Ecosystem

Tesla's AI capability is built upon self-developed infrastructure. In 2025, training compute power increased by 4 times, equivalent to deploying approximately 81,000 H100 graphics cards, for extracting high-value complex scenarios from 15 million miles of daily fleet video. Data compression efficiency reached 20 times, and the scene recognition accuracy stabilized at 97%. The self-developed AI5/6 chips boosted inference speed by 40 times, significantly reducing reliance on external suppliers, and establishing a complete closed-loop AI ecosystem from training to inference. This capability not only accelerates FSD iteration but also applies intelligent technology deeply into the production process—for example, increasing battery manufacturing efficiency by 10%, thereby reducing overall costs, and supporting the research, development, and mass production of the $25,000 entry-level model, thus solidifying Tesla's comprehensive competitive barrier in price, technology, and scale.

Source: Tesla

1.5.3. Autonomous Driving Taxi (Robotaxi): From Technical Verification to Commercial Implementation

The maturity of FSD technology directly empowers the Robotaxi strategy. In 2025, Tesla launched the Cybercab, specifically designed for autonomous driving, adopting a fully autonomous architecture without a steering wheel or pedals, and featuring a range of 300 miles. Currently, Cybercab has initiated limited commercial operation in the California Bay Area and Austin, Texas, with fleet sizes exceeding 1,000 and 500 vehicles, respectively, providing tens of thousands of safe rides, all equipped with safety supervisors to ensure stability during the transition period. FSD v14's neural network has integrated real-time navigation optimization, dynamic path planning, and emergency response mechanisms, paving the way for future unsupervised operation. Tesla plans to commence mass production of the Cybercab in the second half of 2026 and expand the Robotaxi service to more than 10 major cities by the end of 2025. This business model is expected to contribute significant new revenue to the company, becoming another high-gross-margin growth engine following FSD subscriptions.

2. BYD

BYD Co., Ltd. was established in 1995 and is headquartered in Shenzhen, China. It is a global leading new energy vehicle manufacturer. The company follows the philosophy of "Build Your Dreams" and focuses on the research, development, and production of new energy vehicles, power batteries, and energy storage systems.

BYD's story is almost a microcosm of Chinese manufacturing's upward breakthrough. In its early years, it relied on Shenzhen's local advantageous industrial policies, manufacturing environment, and multiple explicit and implicit supports from the government upstream and downstream. From a battery foundry in 1995 to ranking 91st on the Fortune Global 500 in 2025, the company took 30 years to complete the leap from OEM to defining standards. Its most prominent characteristic is vertical integration: batteries, motors, electronic controls, and even semiconductors are almost all produced in-house.

2.1 Market Share and Sales Volume

At the market share level, BYD has been extremely aggressive. From 2022 to 2024, BYD first surpassed Tesla in the Chinese market with a strong pricing strategy, a rich product lineup, and vast channels, securing the top spot in global sales. In the first half of 2025, BYD delivered an almost crushing report card, with cumulative sales of 2.146 million units, up 33.0% year-over-year, continuing to claim the championship in China and global new energy vehicle sales. In the Chinese market, BYD's new energy vehicle market share climbed to about 32%.

From a global perspective, BYD's share in the electric vehicle market is about 22%, firmly holding the world No. 1 position. Overseas markets are the new engine of the company's growth, with first-half sales reaching 470,000 units, up 132% year-over-year, already exceeding the full-year total for 2024. Among them, the Thailand market share is 41%, Brazil 66%, Colombia 45%, strongly replacing Toyota and Volkswagen in emerging markets.

BYD's global dominance is not driven by a single hit model, but by a systematic "car sea" tactic. From the 70,000-yuan Seagull to the million-yuan Yangwang, from plug-in hybrids to pure electrics, from sedans to SUVs, it covers almost all market segments. It crushes most competitors with scale and channel advantages, and quickly penetrates emerging markets like Southeast Asia and Latin America with mid-range pricing, strong supply chains, and high reliability. In terms of high-end breakthroughs, the Yangwang brand is the core vehicle for BYD's strategic upgrade. Yangwang Auto uses models like the U8 and U9 to directly challenge BMW, Mercedes, and Audi, targeting the million-yuan market. BYD spares no expense on major events: such as the Yangwang fleet paying tribute to the Hong Kong-Zhuhai-Macao Bridge project, Speed customized cars parading in Shenzhen, etc., but in the high-end market (especially Europe), brand recognition remains a shortcoming—some local consumers still don't know how to pronounce "BYD" correctly.

2.2 Cost and Profit Analysis

In the first half of 2025, BYD's profit core faced significant pressure. The gross margin for the vehicle business dropped to about 18.7%. Gross profit per vehicle fell to 26,000 yuan, while net profit per vehicle was only about 5,000 yuan.

The core reasons for the gross margin decline are three: sustained price wars, insufficient contribution from high-end brands, and rising R&D and intelligentization costs. The company's per-vehicle manufacturing cost rose to 112,000 yuan, an increase of about 10,000 yuan quarter-over-quarter, with key factors including upgrades to intelligent driving systems, dealer rebates, and marginal management cost increases due to capacity expansion.

Despite short-term profit pressure, this low-profit, high-volume model is BYD's classic strategy. It seizes market share through cost suppression, using core technologies like blade batteries and the e-platform 3.0 to drastically cut production costs, enabling A0-class electric vehicles to be produced for 90,000 yuan while still breaking even at a 70,000-yuan selling price. This extreme efficiency logic makes BYD nearly invincible in price competition.

Unlike Tesla, which relies on high premiums and software subscriptions, BYD adheres to the industrial era's mass production philosophy: first lock in market scale, then extract profits from supply chain efficiency. This strategy may appear self-squeezing in the short term, but in the long run, it could form scale barriers, giving it the ability to raise prices and eliminate competitors. However, the price-for-volume model also harbors hidden risks. The cash flow pressure from high capacity makes BYD's profit quality increasingly dependent on supply chain finance and payment term management, rather than real consumption growth. If industry subsidies fully exit or capacity expansion becomes excessive in the future, profitability could be squeezed to the limit.

2.3 Financial Status Analysis

On the surface, BYD's financial condition is remarkably solid. As of the end of June 2025, the company had cash reserves of 156.1 billion yuan, total liabilities of approximately 601.6 billion yuan, and an asset-liability ratio of 71.1%. Financial leverage is not aggressive, and the structure is very attractive: interest-bearing debt is only 41.6 billion yuan, accounting for 6.9%, with cash reserves roughly four times the interest-bearing debt. Operating cash flow is equally impressive, with a net inflow of 31.8 billion yuan in the first half, up 124% year-over-year, including a single-quarter inflow of 23.2 billion yuan in the second quarter, a nearly fivefold surge. At first glance, BYD appears to be one of the rare cash machines in the automotive industry.

However, behind BYD's abundant cash lies a complex capital chain logic. Its ample liquidity is partly built on delayed payments to the supply chain and commercial bill financing, which is also the root of external concerns about the company's structural risks. BYD's accounts payable reached 236.69 billion yuan, accounting for nearly 40% of total liabilities. Over the past few years, its supplier payment terms have been extended from an average of 200 days to 300 days—three times that of Tesla. Although the company promised in June 2025 to compress payment terms to 60 days, execution has been incomplete, with a large volume of commercial acceptance bills still circulating in the market.

In the first half of the year, BYD's financing through bill endorsement and discounting reached 159.2 billion yuan, accounting for about 40% of operating revenue. In other words, nearly half of sales

payments are settled with bills rather than cash. This structure may optimize reported cash flow, but it outsources credit risk to suppliers: BYD enjoys ample funds on its books, while upstream component companies bear the liquidity pressure. If discount rates rise or the financial environment tightens, this supply chain finance model could backfire on the automaker.

BYD has leveraged its strong cash flow to wage unmatched price wars and expansion. While other automakers rely on financing transfusions, BYD can sustain a prolonged battle through self-generated cash. This is its moat—and its double-edged sword. It is not without debt; rather, it has hidden the debt within the supply chain.

2.4 Financing Capability

Unlike the new forces that rely on external financing, BYD's financing is known for its multi-channel, low-cost, and balanced structure. The company's main financing channels currently include:

· Offshore equity financing: In March 2025, BYD completed a HK$43.5 billion (approximately US$5.6 billion) lightning placement of H-shares, the largest equity refinancing in the global automotive industry in nearly a decade, with funds used for overseas capacity construction, intelligent R&D, and liquidity replenishment. This issuance attracted long-term capital including Goldman Sachs, the Abu Dhabi sovereign fund, and Middle Eastern strategic investors.

· Bonds and short-term financing bills: In the first half of 2025, ultra-short-term financing bills and sci-tech innovation bonds were issued to optimize the debt structure and reduce overall financing costs. These direct financing tools allow BYD to retain extremely high capital flexibility amid interest rate environment fluctuations.

· Internal financial system: Through BYD Auto Finance and international financing leasing subsidiaries, the company has established a self-circulating capital system in vehicle sales and supply chain segments, enhancing capital usage efficiency.

· Supply chain financialization: Using commercial bills and discounting mechanisms to transform upstream payables into quasi-financing channels—this is BYD's most controversial and most covert capital method.

This hybrid financing model gives BYD both industrial leverage efficiency and strong liquidity buffers. BYD is more like a manufacturing enterprise that understands finance.

2.5 Degree of Intelligence

Entering 2025, the company's investment in the intelligence field reached an unprecedented scale: R&D expenditure in the first half reached 30.88 billion yuan, up 53% year-over-year, with the investment ratio ranking among the top in the automotive industry. The most core technological achievement is the "Eye of Heaven" intelligent driving system, which pushes high-level intelligent driving functions down to 100,000-yuan models, truly promoting the popularization of intelligent driving for all.

Unlike Tesla's pursuit of pure vision autonomous driving, BYD has chosen a steady path of multi-sensor fusion + algorithm optimization. The Eye of Heaven system is equipped with a multi-perception solution including lidar, millimeter-wave radar, ultrasonic radar, and high-definition cameras, and uses the self-developed Xuanji architecture and high-computing DiPilot chip platform as the core to achieve 360-degree full-dimensional perception and efficient data processing. The algorithm does not pursue an unmanned driving revolution but focuses more on energy-saving scheduling, driving safety, and commuting efficiency.

As of the end of May 2025, the cumulative sales of intelligent driving models equipped with the Eye of Heaven exceeded 710,000 units, generating more than 44 million kilometers of driving data daily, building for BYD the largest and most data-intensive self-learning system among new energy vehicle companies.

Overall, BYD is a typical engineering-oriented company and possibly the most pragmatic electric vehicle enterprise. Cheap and high-volume, technologically self-consistent, financially sound, and restrained expansion are its four keywords. Its ambition is not to tell innovation stories but to build an industrial empire.

3. Xiaomi

Xiaomi's car-making story is an example of internet logic invading traditional manufacturing. Founder Lei Jun, this entrepreneurial godfather who dominates half of the brand's influence, is like Musk with his own halo and traffic, but even better at continuously empowering products with personal narratives. From kneeling at press conferences to nationwide self-driving live streams, Lei Jun's charisma and IP have almost become Xiaomi Auto's biggest brand, giving Xiaomi a fan economy similar to Tesla's person-company unity. Since officially announcing car-making in 2021 and launching the first SU7 in 2024, Xiaomi Auto has quickly risen with an "ecosystem integration + data-driven" strategy. The company leverages the technology, supply chain, and traffic dividends accumulated from its phone, IoT, and AI ecosystems to position the car as a mobile super terminal—the next entry point connecting people, phones, and homes.

By 2025, Xiaomi Auto has become the most imaginative segment within the group: the Suzhou factory rolls off a car every 76 seconds, the Beijing Yizhuang Phase 1 has an annual capacity of 320,000 vehicles, and Phase 2 plans for 500,000. Unlike traditional automakers' steady advancement, Xiaomi uses software-style logic to drive hardware factory operations, with its core competitiveness lying in rapid trial-and-error and data accumulation.

But precisely because of the brand's high personalization and rapidly accumulated hype, Xiaomi Auto has also faced some PR crises. Under the rapid sales climb, product quality control and safety systems have endured unprecedented pressure in a short time. In the second half of 2025, a series of unexpected safety accidents and public opinion events erupted, with the market questioning Xiaomi's car-making safety.

3.1 Market Share and Sales Volume

The 2024 launch of the first SU7 model strongly ignited the Chinese new energy vehicle industry and nationwide social buzz. In the first month, cumulative reservations exceeded 240,000 units, setting the record for the fastest to break 100,000 sales in Chinese new energy vehicles. The SU7 became a trendy icon tailored for young people. Behind this hit model logic is Xiaomi's blitzkrieg on the market, achieved through extreme supply chain efficiency, internet marketing tactics, and exceptional configuration-to-price ratio—owning a Xiaomi SU7 became social currency for trendy youth and geek circles.

In the first half of 2025, the Xiaomi SU7 series delivered 157,000 new vehicles, ranking fourth among new forces, behind Li Auto, XPeng, and Leapmotor, with a market share of about 3.5%. Benefiting from the sustained hype of the SU7 and the launch of the high-end SU7 Ultra version, the company's new vehicle business revenue reached 20.6 billion yuan in the first half, with an average price of about 253,000 yuan, up 10.9% year-over-year. Although the YU7 SUV series was only released in the second quarter, it secured 240,000 locked orders on the first day, laying the groundwork for second-half growth.

From a regional perspective, sales are mainly concentrated in the Yangtze River Delta and Pearl River Delta, with Hangzhou, Shanghai, and Shenzhen as the largest consumer markets. This means Xiaomi Auto has not yet gone mass-market, and its user base remains the mid-to-high-end consumer group loyal to tech brands.

3.2 Cost and Profit Analysis

Xiaomi Auto's achievement lies more in profitability: in the first half of 2025, gross margin reached 26.4%, with gross profit per vehicle at about 67,000 yuan—surpassing mainstream automakers like Tesla and BYD.

This impressive performance stems from the victory of an internet-style focused strategy. Xiaomi concentrated all resources on creating a single hit model—the SU7—reducing manufacturing costs by about 25% through vertical supply chain integration and hardware parameter transparency.

However, this high gross margin may be a phased dividend: concentrated resources, relatively high pricing, and high-end models supporting the average price. As the YU7 gains volume and Xiaomi expands to lower-priced vehicles, its profitability is expected to converge.

3.3 Financial Status Analysis

As of mid-2025, Xiaomi Group had cash reserves of 208.7 billion yuan, with an overall group liability ratio of about 47%, placing it at an absolute leading safety level among domestic tech manufacturing enterprises. Long-term liabilities are mainly concentrated in bonds and industrial financing, while the short-term liquidity liability structure is relatively healthy, mostly consisting of accounts payable and supply chain finance.

Notably, Xiaomi has consistently maintained high net cash, avoiding systemic risks from excessive leverage. In the first half of 2025, Xiaomi Group's operating cash flow net amount was 18.2 billion yuan, achieving doubled growth year-over-year. Although the automotive segment is still in the incubation phase, with a slight loss of 300 million yuan in the first half, the loss has significantly narrowed compared to the end of 2024 and is fully covered by the positive cash flow from consumer electronics, IoT, and internet businesses.

3.4 Financing Capability

Xiaomi's capital strategy is essentially "self-hematopoiesis + industrial synergy." On one hand, relying on strong free cash flow, the core segments of mobile phones, IoT, and internet continuously transfuse cash to the automotive business, building an internal blood supply mechanism. On the other hand, Xiaomi actively co-invests with upstream and downstream giants like CATL and BOE in automotive core components and ecosystem projects, creating a joint investment body that locks in the supply chain while sharing early risks.

In terms of overseas financing, the company plans to issue special new energy bonds on the Hong Kong

Stock Exchange and introduce long-term strategic capital through international industrial funds. This layout enables Xiaomi to have sufficient financial resilience even in the early loss-making and high R&D investment stages, without frequent reliance on high-risk external leverage. As Lei Jun said, raising cars relies on phones—Xiaomi's project cycle confidence comes from the group's cash flow and independent capital operation capabilities, which is also the biggest difference from new forces and traditional automakers.

3.5 Degree of Intelligence

Compared to building cars, Xiaomi is more like building a connected ecosystem. In 2025, R&D investment in automotive and AI businesses reached 12 billion yuan, accounting for over 22%, with full integration of AI large models and the self-developed HyperEngine control chip into the intelligent driving system.

Xiaomi's intelligent driving solution adopts lidar + multi-modal fusion perception, with its advantage lying in aggregating user data through cloud AI to achieve iterative driving behavior. Unlike Tesla's end-side learning, Xiaomi's intelligent driving strategy is more like the MIUI of phones: rapid OTA updates, agile data feedback, and continuous experience optimization. Intelligent driving is not just a feature but an algorithm service that keeps evolving. At the same time, the SU7 seamlessly interconnects with the Xiaomi HyperOS system, fusing "human-car-home" into a unified ecosystem. This design not only reflects Xiaomi's systemic thinking but also strengthens its marketing narrative: intelligence is a way of life.

The essence of Xiaomi Auto is injecting internet speed into manufacturing logic. It does not pride itself on extreme engineering but uses user mindset and data feedback as weapons.

4. NIO

NIO Inc., founded by William Li in 2014, stands as one of China's leading electric vehicle companies. NIO's development trajectory closely mirrored that of Tesla, with its first vehicle being a supercar. William invited the president of Maserati to help create NIO's inaugural supercar, the EP9, and even formed a Formula E racing team, claiming the driver's championship in its first year. However, despite a price tag of $1.2 million per vehicle, only six units of the EP9 were sold. Although the EP9 was not designed for ordinary consumers, it significantly elevated NIO's brand awareness.

Since its inception, NIO has focused on the high-end SUV market with prices starting from 400,000 RMB, directly competing with mid to high-end models from luxury brands like BMW, Benz, and Audi (BBA). Beyond vehicle sales, Li Bin also established 176 NIO Houses, akin to the Hong Kong Jockey Club, indicating NIO's ambition to create a high-net-worth community that integrates car ownership with an app and service-based foundation.

4.1 Market Share and Sales Volume

Sales data shows that in the first half of 2025, NIO's cumulative deliveries reached 114,150 vehicles, marking a 30.6% year-over-year increase. In Q2 alone, deliveries soared to 72,056 units, achieving a remarkable quarter-over-quarter growth of 71.2%, demonstrating a robust recovery momentum.

Since 2022, NIO has confronted various challenges, yet its annual vehicle deliveries have consistently increased—from just 122,000 units in 2022 to 114,000 in the first half of 2025. The company has also announced a Q3 2025 delivery target reaching 87,000 units. This growth can be attributed to its multi-brand strategy, with contributions from the NIO brand, the ONVO brand, and the FIREFLY brand.

In terms of market share, despite steady yearly growth, NIO maintains only approximately 1.6% of the market in China, primarily due to its pricing strategy leaning towards high-net-worth consumers and high-end SUVs.

4.2 Cost and Profit Analysis

In addition to delivery volumes, gross margin is a core metric that the market closely scrutinizes, as it reflects the company's operational efficiency and strategic effectiveness.

According to NIO's financial report, over the past five years, its gross margin has exhibited a downward then upward trend and is now in a recovery phase, surpassing 9% in the first half of 2025. The company is actively implementing cost reduction measures and adjusting its product strategy to focus on high-margin SUV models, such as the ES8 and L90, in hopes of further enhancing profitability. Li's previously set goal of achieving breakeven by Q4 2025 mandates that vehicle gross margins exceed 17% with monthly deliveries surpassing 70,000 vehicles. Currently, delivery numbers seem assured, but gross margin remains a considerable concern. Particularly, the two sub-brands ONVO and FIREFLY target more affordable markets and have significantly lower gross margins than NIO's main brand, potentially dragging down the overall profitability levels in the short term.

4.3 Financial Status Analysis

As of H1 2025, NIO held 7.1 billion RMB in cash and cash equivalents, a significant decline over the past two years. The company's short-term interest-bearing loans continue to trend upwards. Although there is no immediate liquidity risk, its debt-to-equity ratio is among the highest in the automotive industry, indicating substantial future risks that depend on either the company's or Li Bin's ability to secure financing for continued support.

As one of the most cash-intensive new automakers, NIO has seen negative net cash flow from operating activities in the past few years.

Although NIO currently has sufficient cash reserves to support short-term operations, persistent operating losses and a high debt structure imply a strong reliance on external financing. The absence of operational cash flow data complicates external assessments of its core business's capacity for "self-funding."

4.4 Financing Capability

Despite facing profitability challenges, NIO continues to showcase robust fundraising capabilities in the capital markets, gaining support from sovereign funds, local Chinese governments, and well-known companies and investors like Xiaomi, Li Auto, and CATL. This reflects a degree of confidence from capital markets in NIO's long-term technological vision, brand value, and market potential.

In addition to equity financing, NIO also relies on debt financing. The financial reports indicate its cash flow from operations, equity financing, and borrowing capacity, alongside established loan agreements with multiple banks in China. The company has also planned to issue convertible bonds to supplement its capital.

4.5 Degree of Intelligence

NIO's autonomous driving system, NAD (NIO Autonomous Driving), aims for L4-level full-scene autonomous driving in the long term. However, it is currently regarded as being at the L2+ level, which qualifies as advanced driver assistance.

4.6 Unique Advantages and Risks

The battery swap model and energy service network represent NIO's most distinctive moat, difficult for competitors to replicate quickly. Yet, it is also a double-edged sword, with each battery swap station costing around 1.5 million RMB, impacting NIO's balance sheet if sales do not sustain upwards momentum.

Through innovative channels like NIO House and the NIO App, the company has established a highly engaged user operation model. The rarity of its community's activity and brand loyalty in the automotive industry has fostered a significant word-of-mouth effect and brand cohesion, with this “user-centric” positioning at its core soft power.

Ultimately, selling cars is the most crucial thing for survival. NIO's premium services are predicated on high-net-worth customers paying a premium for high-end models. In order to sell more cars, future product prices will tend to fall to lower levels, reducing profit margins per vehicle. The increase in the number of service users may place a greater burden on existing service teams and costs, which may alienate high-net-worth customers who previously paid a premium for more expensive models.

5. Li Auto

Li Auto was founded in 2015 by Li Xiang, a prodigious entrepreneur who achieved success and financial independence before establishing the Li brand. His previous ventures, including two famous websites called “Paopao” and “Autohome”, were both in the automotive industry, providing invaluable experience for crafting vehicles. Arguably, among new energy brands, Li Xiang is the most knowledgeable about cars.

In 2018, Li Auto unveiled its first electric vehicle, the Li ONE, designed to be an "intelligent electric vehicle without range anxiety," utilizing a range-extended electric system to alleviate the common range concerns associated with pure electric vehicles. Li is the only new force that has prioritized creating range-extended hybrid vehicles over pure electric ones.

5.1 Market Share and Sales Volume

After launching the Li ONE, the model helped the brand secure the sales championship for medium and large SUVs in China for 15 consecutive months, with cumulative sales exceeding 210,000 units over two years, confirming that the strategy of range-extended hybrids as a transitional technology was correct. This marked the beginning of an important product matrix for Li, known as the L series, leading the company into a rapid growth phase. In 2022, Li launched the family-oriented flagship SUV, the Li L9, targeting high-end family vehicles. Inspired by Russian nesting dolls, Li also introduced the L8, L7, and L6 models.

Starting in 2022, Li's sales and deliveries accelerated rapidly from 130,000 units to 370,000 units, becoming the first new energy brand to exceed annual deliveries of 500,000 vehicles.

Boasting a range-extended technology and relatively clear user positioning, Li Auto has maintained its leading position in China's SUV segment priced above 200,000 RMB. The latest data reveals that for January to July 2025, in the 200,000 RMB and above SUV market, Li Auto ranked at the top with almost 230,000 cumulative sales, capturing a market share of 12.31%, surpassing traditional luxury brands like BMW, Benz, and Audi, and even Tesla.

5.2 Cost and Profit Analysis

Li Auto's unique technology advantage and relatively “focused” product matrix, along with Li Xiang’s rigorous pursuit of operational cost efficiency, have allowed the company to maintain a consistently high gross margin, exceeding 21% over the past three years, outpacing Tesla. Li's pursuit of strict cost control does not hinder significant investments in R&D. This approach reflects a strategic focus on steady progress; Li has always believed in spending money wisely.

Over the past year, Li has increased funding significantly. Acknowledging the need to transition from range-extended vehicles to pure electric ones, Li Auto has constructed more charging stations in China than Tesla currently operates to pave the way for pure electric vehicle sales. Concurrently, the brand has ramped up investments in AI, including developing a large language model and an in-car intelligent assistant, Li Xiang's classmate, alongside high investments in autonomous driving technology.

By the second half of 2025, Li Auto plans to launch pure electric models, i8 and i6, which differ from the L series. The i6 targets a younger demographic and families without children, with a price point under 250,000 RMB, representing the most competitive segment in the market, facing competitors like the Tesla Model Y and Xiaomi Yu7. However, due to Li Auto's aggressive strategy and the brand's transitional growing pains this year, the costs have surged, and the gross margins for the new electric models will likely drop significantly below the 20% threshold that the company has maintained.

5.3 Financial Status Analysis

Historically, Li Auto's cash flow situation ranks among the most stable within the automotive sector, bolstered by strong sales volumes and gross profits coupled with low manufacturing costs. Although cash reserves of around 50 billion RMB have decreased from the previous two years (due to investments in new vehicle R&D), they remain healthy. By the first quarter of 2025, free cash flow recorded a negative 2.5 billion RMB, expanding to negative 3.8 billion RMB in the second quarter. The continuous negative free cash flow indicates the company is in a rapid expansion phase, investing heavily in production capacity and technology R&D. However, considering its strong financing capabilities and cash reserves, Li is not expected to face liquidity crises in the short term.

In terms of debt structure, the company primarily carries current liabilities, but repayment pressure remains manageable. Current liabilities amount to 71.23 billion RMB, comprising 81.3% of total liabilities, mainly including payables and short-term loans. Importantly, the firm has a relatively healthy debt structure, with a low proportion of interest-bearing debt, relying mostly on operational liabilities for liquidity.

5.4 Financing Capability

Since 2023, Li Auto has not engaged in large-scale equity financing, with funding primarily sourced from operating cash flows, marking the shift from "externally dependent financing" to "self-reliant" financial stability.

Moreover, the company is listed on both the US and Hong Kong stock exchanges, ensuring smooth access to capital. It boasts ample bank credit lines and has successfully issued bonds, demonstrating strong trust from various financial institutions. Even in less favorable market conditions, the company has managed to secure the necessary funding.

5.5 Degree of Intelligence

Li Auto places a significant emphasis on automotive intelligence and autonomous driving, steadily investing heavily in R&D. The company follows a fully self-developed approach, managing end-to-end from perception, prediction, planning, and control. Notably, it leads the industry in applications of AI large models, with the upcoming VLA (Vision Language Action) driver model in 2025 representing Li Auto's latest achievement in AI. This model enhances the user experience around six primary dimensions: "choosing the right road, maintaining speed accuracy, comfort, security, communication capability, and efficiency," featuring speed memory capabilities that allow it to recall user preferences on specific routes. Surveys indicate that an increasing number of vehicle owners have chosen to let VLA take over driving, with the usage of autonomous driving time exceeding their manual driving time.

6. XPeng Motors

XPeng Motors, co-founded by He Xiaopeng, Xia Heng, and He Tao in 2014, is headquartered in Guangzhou. From its inception, XPeng set its sights on young consumers in first-tier cities, emphasizing a strategy that combines intelligence with cost-effectiveness.

The company's developmental trajectory is characterized by a "rapid iteration + technology implementation" ethos. In 2017, it produced its first batch of vehicles, with the G3 model delivered in 2018, making it one of the first in the internet-based automotive sector to achieve mass production. Through models like the G3 and P7, XPeng rapidly established market recognition for its intelligent driving features, which became key differentiators in its early competitive landscape.

6.1 Market Share and Sales Volume

In the first half of 2025, XPeng Motors experienced explosive growth, with cumulative deliveries reaching 198,000 vehicles, representing an astounding year-over-year increase of 245.3%, significantly outpacing industry averages. In Q1, 94,000 units were delivered—up 331% year-on-year—securing the top sales position among new energy vehicle manufacturers. In Q2, deliveries rose to 104,000 units, reflecting a robust quarter-on-quarter growth of 10.6%.

This surge in deliveries and revenue is largely attributable to two of the company’s latest hot-selling products: the XPeng Mona M03 and the P7+. The former, priced at an average of 120,000 RMB as an entry-level model, features XPeng's self-developed advanced driving system—Turing AI, which is powered by dual Orin-X chips that enhance its computing power to 508 TOPS, improving the integration of perception, decision-making, and control, thereby enriching the driving experience.

The combination of exceptional cost-performance and leading-edge smart technology enabled the Mona M03 to accumulate over 100,000 deliveries within just eight months of launch. The mid-range model P7+, launched five months later, saw nearly 50,000 deliveries. Meanwhile, the 2025 models G6 and G9 collectively achieved over 7,500 deliveries in April alone, ensuring full coverage across all price segments. As the third quarter approached, the all-new generation P7, which debuted at the end of August, broke the 10,000-unit mark in just seven minutes during pre-orders, setting a record for the fastest new model to reach this figure, attesting to market confidence in its product strength.

Benefiting from this rapid sales growth, XPeng has significantly improved its market share in China's new energy vehicle sector. This success stems from its precise market positioning—catering to the mainstream price range of 150,000 to 350,000 RMB—allowing it to sidestep intense competition in the high-end market while capturing the rising demand for intelligent features among consumers.

6.2 Cost and Profit Analysis

The ongoing improvement in gross margins is one of XPeng's core highlights for the first half of 2025. According to financial reports, the company's gross margin surged from 13.5% in the same period of 2024 to 16.5%, with automotive gross margins showing even greater strength, rising from 6.0% to 12.6%. This figure has seen continuous improvement over eight consecutive quarters and further escalated to 14.3% in Q2 2025, marking a historical high.

This enhancement can be attributed primarily to two factors: first, the realization of scale effects, as doubling sales helps dilute fixed R&D and production costs; second, effective cost control facilitated by the SEPA 2.0 platform, which improved the interchangeability of components across different models to over 80%. He Xiaopeng revealed during the earnings call that the company's objective is to achieve breakeven by the end of 2025, requiring automotive gross margins to stabilize above 15% and monthly deliveries to maintain above 35,000 units. Currently, both targets are nearing this threshold.

However, challenges remain, especially with the strong sales of the entry-level M03 model, which has lowered the overall average selling price from 253,900 RMB in Q1 2024 to 152,900 RMB in Q1 2025. While service revenues, with 1.72 billion RMB and a margin of 60.1% in the first half, have partially offset this impact, the increasing proportion of lower-priced models still constrains profit margin growth.

6.3 Financial Status Analysis

As of June 30, 2025, XPeng reported total current assets of 54.771 billion RMB, with cash and cash equivalents and short-term investments amounting to 45.28 billion RMB—a steady increase from 41.96 billion RMB at the end of 2024. This reflects a healthy liquidity position. Concurrently, total liabilities reached 62.09 billion RMB, showing a slight increase compared to the end of 2024; however, the debt structure is primarily based on long-term project financing, with short-term interest-bearing debt accounting for less than 30%, resulting in a low liquidity risk profile.

The company's cash flow situation has seen significant improvement this year, with Q1 2025 free cash flow exceeding 3 billion RMB—marking the best performance for the same period in its history. This represents XPeng's first instance of positive free cash flow in a single quarter since its establishment. XPeng now has sufficient cash reserves to support R&D investments and market expansion over the next 1-2 years. The emergence of positive free cash flow indicates that its core business has begun to develop initial self-sustaining capabilities, significantly reducing reliance on external financing.

6.4 Financing Capability

Despite its improved cash flow foundation, XPeng continues to demonstrate strong appeal in the capital markets. Early investors included Alibaba, Foxconn, and IDG Capital, and in 2019, Xiaomi Group became a strategic investment partner. Since 2024, the company has raised over 8 billion RMB through stock issuance and green bonds in the Hong Kong market, bolstering its funding for technology R&D.

6.5 Degree of Intelligence

At the core of XPeng's intelligence is the XNGP smart assisted driving system, which aims for L4l full-scenario autonomous driving in the long term. Currently, it has evolved to a L2+ advanced driving assistance stage, leveraging advantages from its "full-stack self-development + data closed loop" approach. By mid-2025, XNGP had achieved road coverage across all cities nationwide, including capabilities in areas lacking high-definition maps, with a user penetration rate exceeding 70%, significantly above the industry average.

6.6 Unique Advantages and Risks

Full-Stack Self-Development Technology: XPeng is the only new automaker that has achieved full self-development of chips, large models, and algorithms. The successful one-time tape-out of Turing AI chips in 2024 boasts an AI computing power 3-7 times that of mainstream products, with installations planned for Q2 2025. The 72 billion parameter cloud-based large model continues to evolve, providing foundational support for intelligent driving capability upgrades, creating a technological barrier that is challenging to replicate rapidly.

Intelligent Equality Strategy: By reducing technology costs, XPeng has introduced advanced features such as urban assisted driving and 500 TOPS capabilities into models priced around 150,000 RMB (e.g., MONA Max), achieving widespread accessibility of smart technology. While this strategy boosts sales, it raises concerns about potential downward pressure on brand positioning—over-reliance on products priced below 200,000 RMB could affect pricing power for high-end models.

Balancing R&D Investment and Profitability: In Q1 2025, R&D expenses hit 1.98 billion RMB, marking a 46.7% increase year-on-year. Continued high investment is essential for maintaining technological leadership but also increases profitability pressure. The challenge lies in finding a balance between technological iteration and profit growth, an ongoing long-term concern for the company.

EV Investment Strategy: Flagship Leadership, Growth Escort, Global Deployment

Driven by the strong impetus of the intelligent transformation wave in the 2025 electric vehicle market, global sales are rapidly approaching the 20 million mark, with China's market penetration nearing 60% and the popularization rate of advanced technologies like ADAS exceeding 70%. Starting from multiple dimensions such as market competitiveness, per-vehicle profitability, financial stability, financing potential, and intelligence level, we assist investors in building a comprehensive investment strategy for the electric vehicle industry. This strategy not only focuses on selecting individual stocks but also extends to grasping key time nodes and risk diversification mechanisms, thereby steadily capturing sustainable returns in this EV market with a long-term growth trend.

Firstly, in the core flagship allocation strategy for the electric vehicle industry, prioritize locking in leading players with high barriers to construct a stable base position for the portfolio. Among them, Tesla stands out with comprehensive advantages: FSD data accumulation of 6 billion miles, safety leading the industry by 9 times, continuously decreasing battery costs, thereby achieving a strong financial backing of $7,700 gross profit per vehicle and $42 billion in cash reserves. It is suitable as a main allocation to fully capture the long-term potential of AI-driven software subscription services and Robotaxi. BYD, in contrast, demonstrates excellent balanced strength, with a market share as high as 22% and overseas sales growing by 132%. It relies on its "sea of cars" strategy and Blade Battery technology to build scale barriers and is recommended for inclusion in the core layer to balance defensive attributes with expansion opportunities in emerging markets. The core logic of this strategy lies in the high complementarity of the two: Tesla represents high-premium innovation, while BYD focuses on low-cost penetration, effectively avoiding single-reliance risk and ensuring the portfolio moves steadily forward in the wave of intelligence.

Secondly, in the growth scenario complement strategy for the electric vehicle industry, select Xiaomi and Li Auto as satellite allocations, targeting specific user needs to supplement the high-end positioning of the core flagships. Xiaomi, with a gross profit margin of approximately 23%, person-car-home ecosystem interconnection, and rapid OTA iteration, along with hot locked orders for the SU7 series and strong potential for the YU7 SUV, and over 200 billion RMB in cash reserves supporting self-sustaining development, is suggested for the growth layer. This placement bets on the democratization of intelligence down to the 150,000 RMB vehicle segment. Li Auto maintains a gross profit margin steadily above 20%, leads the 200,000+ RMB SUV market share, and its VLA large model significantly boosts the takeover rate. Having transitioned to the pure electric i-series and built over 3,000 charging stations, it is also suitable for the growth layer. The core of this strategy is scenario-driven: Xiaomi targets the young tech-savvy demographic, and Li Auto focuses on family upgrading needs. Both are projected to have a compound annual growth rate exceeding 30% by 2026, effectively balancing the flagships' high-end bias and enabling diversified coverage and growth relay in the mid-to-low-end markets for the portfolio.

Thirdly, in the dynamic timing adjustment strategy for the electric vehicle industry, integrate macroeconomic trends and event-driven factors to achieve flexible position management. In the short term, closely track quarterly delivery catalysts: regulatory progress and widespread rollout of Tesla's FSD v14 series, BYD's $5.6 billion H-share financing for capacity expansion, and the mass delivery of the Xiaomi YU7 SUV. If actual performance exceeds expectations, opportunistically increase the allocation of growth stocks to amplify returns. The long-term outlook to 2030 (when the EV market size reaches $652.4 billion and intelligence penetration exceeds 80%) should include setting clear take-profit and stop-loss mechanisms: reduce holdings to preserve capital when the per-vehicle gross profit margin declines by over 5%, and increase investment when cash flow turns positive. Simultaneously, prudently avoid XPeng and NIO (despite their intelligence leadership, they have high financial debt ratios and continuous reliance on external capital infusion), only maintaining a small watching position to capture potential rebounds.

The overall framework maintains a higher proportion of active allocation and retains a certain cash buffer to cope with fluctuations in the interest rate environment. The logic of this strategy is progressive: starting with the selection of flagships based on high individual stock barriers, moving to scenario-driven complementary growth stocks, and extending to dynamic timing adjustments, ultimately forging a resilient portfolio. In the wave of EV transition from electrification to intelligent platforms, insisting on the optimal selection of core players not only captures the sales explosion and technology dividends but also achieves steady value appreciation through multi-dimensional hedging. Investors can thus secure the "future ticket," reaping generous risk-adjusted returns when the market size doubles by 2030.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.