Robinhood Q3 Earnings: Revenue Doubles, Profit Triples. So Why Did Markets Remain Cold?

TradingKey - Robinhood (HOOD), the mass-market online brokerage platform known for commission-free trading, delivered a record Q3 2025 earnings report. The company crushed peers with a 100% surge in revenue and nearly 300% growth in net profit, driven by robust trading activity and diversified business efforts. However, Robinhood's stock declined following the impressive results.

According to Robinhood’s third-quarter earnings report released after the U.S. market close on November 5, the internet investment platform, popular with retail investors, saw its revenue jump 100% year-over-year to a record $1.27 billion, surpassing the expected $1.21 billion. Net profit soared 271% year-over-year to $556 million, with diluted earnings per share (EPS) rising 259% to $0.61, beating the $0.53 consensus estimate.

All three of Robinhood’s core business segments demonstrated strong growth in Q3. Transaction-based revenue surged 129% year-over-year, net interest income increased by 66%, and other revenue, including subscription services, grew 100%.

The expansion into Prediction Markets and the Bitstamp acquisition, aimed at deepening its presence in crypto trading, underscore Robinhood's efforts to reduce reliance on transaction revenue. These initiatives have enriched Robinhood's product matrix and have already achieved initial encouraging results, with management projecting they will collectively generate at least $100 million in annualized revenue for Robinhood.

Robinhood's trading revenue is increasingly diversified, with 90% now derived from non-stock sources, ranging from cryptocurrencies to event contracts. David Bartosiak, an analyst at Zacks Investment Research, noted that Robinhood is evolving into a fintech giant.

Despite the strong Q3 performance, Robinhood's shares fell in after-hours trading following the earnings release, at one point dropping 5%.

Analysts generally attribute this to concerns that Robinhood's Q3 performance may reflect an unsustainable speculative fervor, coupled with cryptocurrency trading revenue missing expectations, and its elevated valuation demanding even higher future growth.

Will the Retail Trading Boom Last?

Transaction-related revenue remains Robinhood’s primary revenue driver, accounting for 57% of total revenue. Robinhood reported that Q3 cryptocurrency revenue more than quadrupled year-over-year to $268 million, options revenue rose 50% to $304 million, and equities revenue increased 132% to $86 million.

However, Robinhood's cryptocurrency revenue growth still fell short of market expectations. According to Zacks Investment data, analysts had anticipated over 400% growth in Q3 crypto revenue, benefiting from a cryptocurrency bull market and a more lenient regulatory environment.

The significant growth in the cryptocurrency business reflects retail investors' strong appetite for these highly speculative assets. Similarly, its nascent Prediction Markets, which contributed $25 million in Q3 revenue, align with this trend.

Piper Sandler found that prediction markets tied to future events are a burgeoning industry trend. This is particularly evident following the 2024 U.S. presidential election, with trading volumes for platforms like Kalshi and Polymarket expected to double in October.

Robinhood executives also indicated a strong start to October, with monthly trading volumes for stocks, options, prediction markets, and futures reaching all-time highs.

Eric Clark, CIO of Accuvest Global Advisors, remarked that the market is becoming more like a casino, and Robinhood is a direct beneficiary of this environment.

Nonetheless, many industry observers question whether this cyclical speculative frenzy can sustainably contribute to Robinhood's revenue.

Charles Bendit, an analyst at Rothschild & Co Redburn and the only one on Wall Street with a "Sell" rating on Robinhood, stated that while Robinhood has demonstrated excellent product execution, he remains concerned that its fundamentals reflect a cyclical boom, and the current valuation implies a cross-cycle sustainability that the company has not yet proven with actual results.

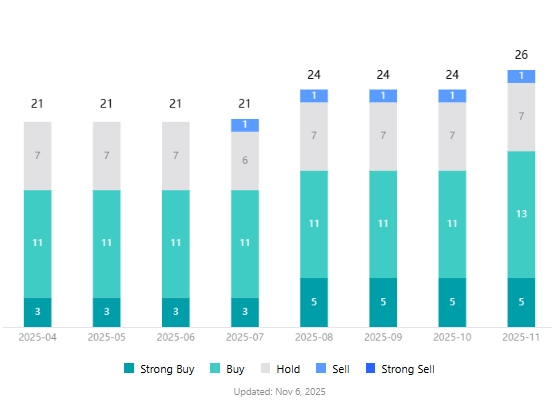

【Robinhood Analyst Ratings, Source: TradingKey】

Bendit assigned Robinhood a price target of just $78, implying a 45% downside from the latest price of $142.48.

Is Robinhood's Valuation Ahead of Itself?

HOOD shares have surged over 280% year-to-date, making it the top-performing stock among S&P 500 components this year.

According to SeekingAlpha data, Robinhood's non-GAAP price-to-earnings (P/E) ratio over the past 12 months stands at 64.44, significantly higher than peers like Interactive Brokers (IBKR) at 33.42, Charles Schwab (SCHW) at 19.60, and LPL Financial (LPLA) at 18.86.

Jay Woods, an analyst at Freedom Capital Markets, noted that the key question now is how much positive momentum has already been priced in by the market, and how significantly a company needs to beat expectations to further drive its stock price.

Woods' answer: "Probably by a lot."

TradingKey analyst Petar Petrov compared Robinhood to traditional brokerages like Charles Schwab and Interactive Brokers, as well as crypto exchanges such as Coinbase and Binance. He found that Robinhood maintains a significant advantage in the online brokerage industry due to its Gen Z-dominated user base, massive user count, multi-asset business model, and aggressive product expansion strategy. However, amid intense competition, the ultimate winner remains uncertain.

Petrov highlighted that a complex competitive landscape is a primary risk for Robinhood stock. If the growth in the number of funded accounts stalls or declines, Robinhood's stock could face significant pressure. Furthermore, a potential bear market poses a risk to transaction-based revenue, while volatile products like options and cryptocurrencies could still face regulatory constraints.

Given the reduced attractiveness of HOOD’s forward P/E ratio, Petrov, while acknowledging Robinhood's competitive advantages, advises investors to await a more attractive buying opportunity.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.