Is Broadcom's Earnings Report a Golden Opportunity or a Bull Trap?

AI Podcast

Broadcom's stock has surged on strong demand for custom AI ASICs, with fiscal Q3 results expected to show robust revenue and EPS growth. This momentum is driven by hyperscalers prioritizing specialized compute infrastructure. Despite increasing revenue, Broadcom faces margin pressure due to a product mix shift and rising infrastructure costs. While facing competition, Broadcom holds a dominant market share. High valuation suggests significant good news is priced in, but consistent performance could support continued holding for existing investors. Supply chain and cyclical risks remain factors to monitor.

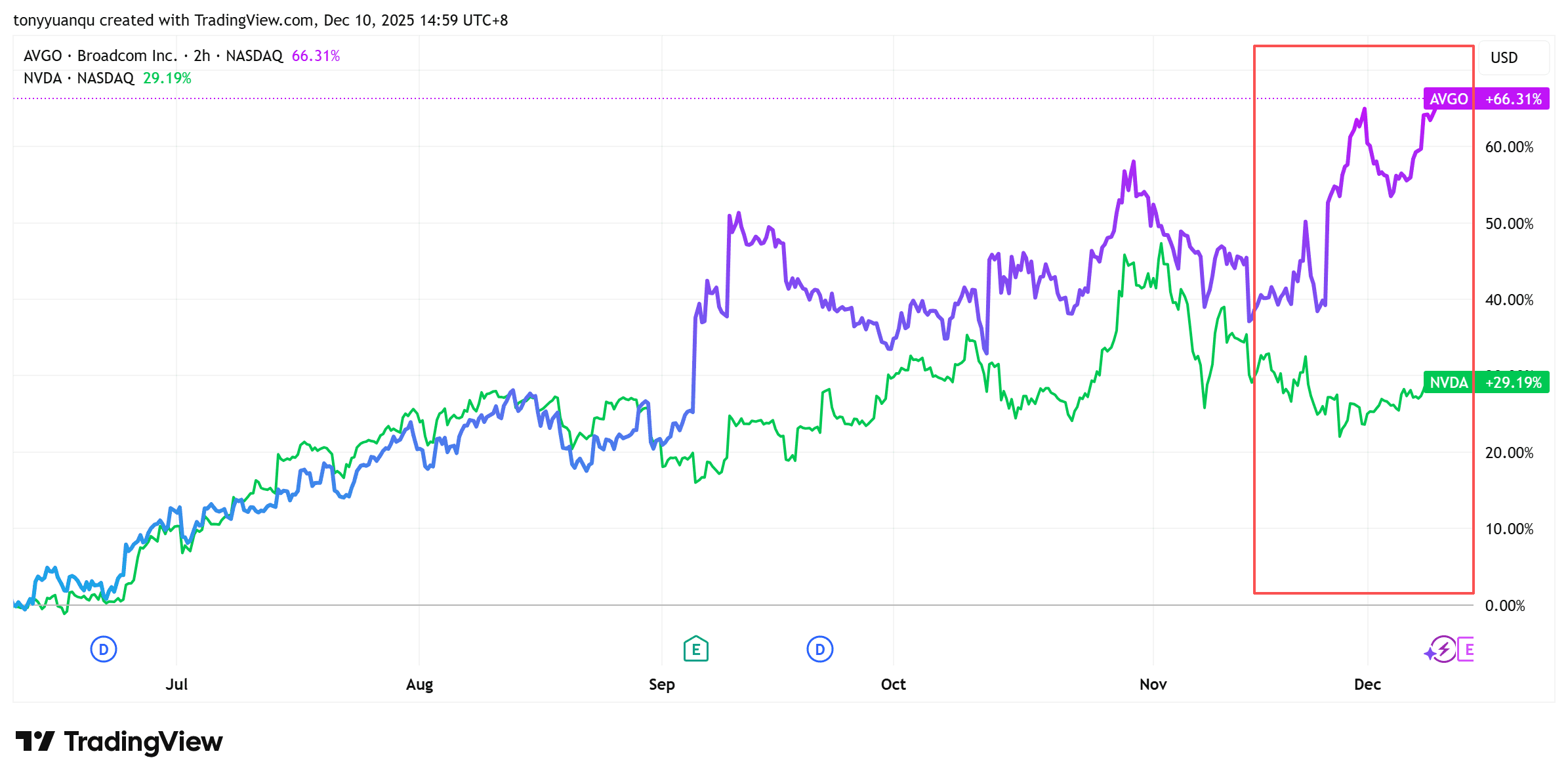

TradingKey - Over the past few quarters, investor attention toward the ASIC market has surged—and Broadcom (AVGO), the clear leader, has been riding that momentum. Since September, its stock has outperformed most tech peers. At times, its relative strength even eclipsed NVIDIA—a rare feat in the current AI chip cycle.

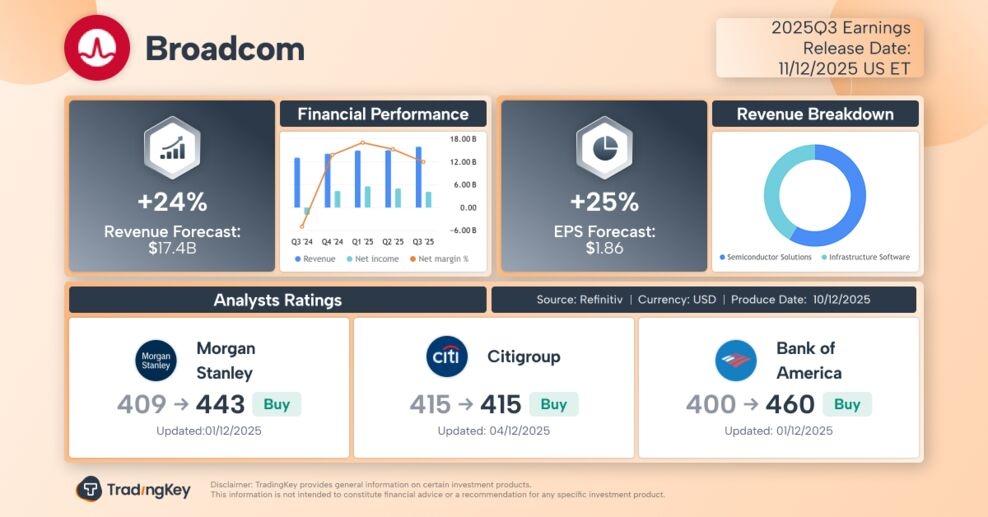

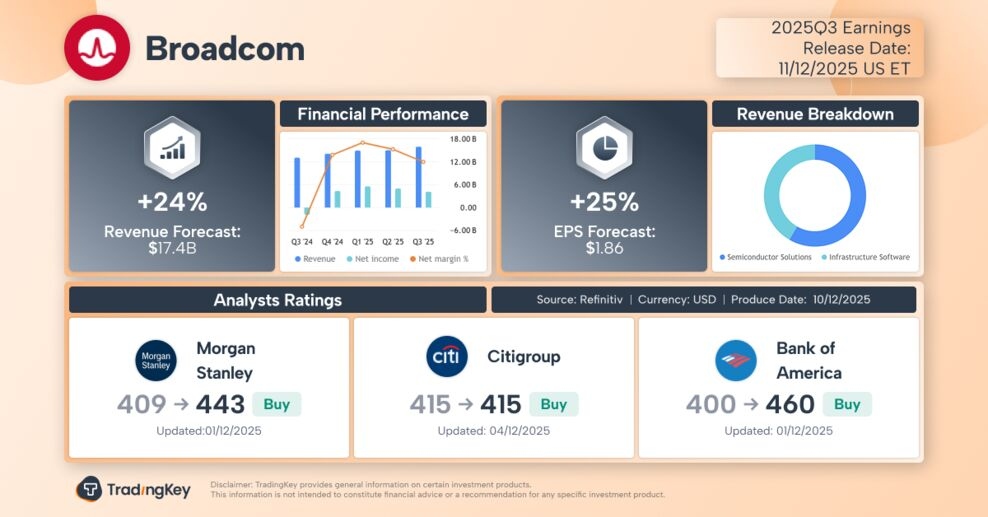

Now, all eyes are on this Thursday’s earnings, when Broadcom will report fiscal Q3 results for 2025. Wall Street expectations are already sky-high: consensus forecasts call for $17.4 billion in revenue (up 24% YoY) and $1.49 in EPS (up 25% YoY). If those numbers land, it could mark the strongest quarter in the company’s history.

But therein lies the risk. With expectations fully priced in, investors are left asking: is this the next leg higher—or has Broadcom already topped out?

Market Share Rising with the Shift to Specialized Compute

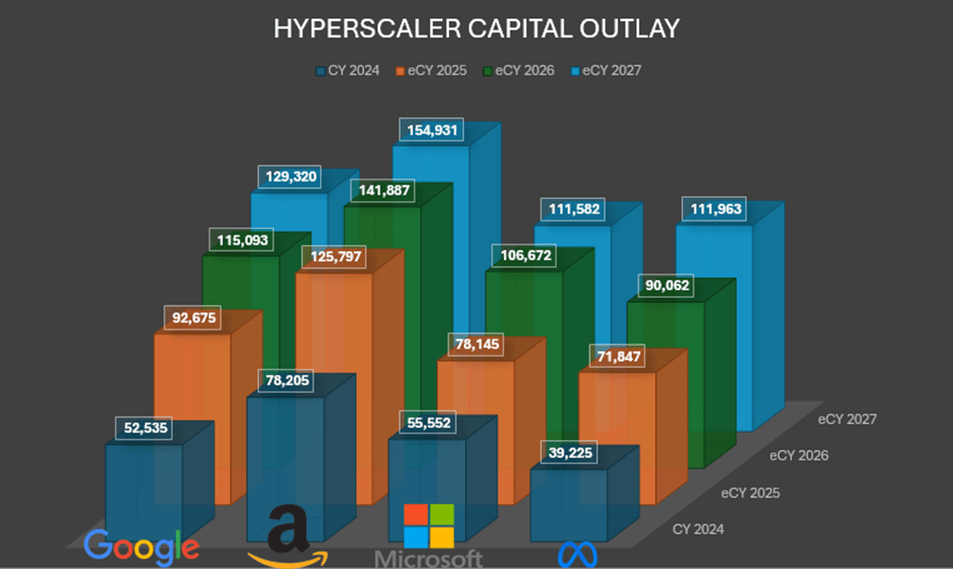

Q3 earnings season is packed with CSP (cloud service provider) results, and for custom AI chip players like Broadcom, that's a structural tailwind. Across the board, hyperscalers have signaled that their 2025 capex will increase materially—especially in infrastructure like XPUs and networking hardware.

Microsoft, for example, continues to emphasize that its AI infrastructure strategy is moving beyond just GPUs and CPUs. Building custom compute (XPUs) and purpose-built interconnects is now a strategic priority—designed to cut model cost and energy use in key inference workloads.

That spells opportunity for Broadcom. The market is already pricing in that shift. Google is doubling down on its custom TPU stack (now at Ironwood / v7), and plans to scale that across its own Gemini model ecosystem. Crucially, Google Cloud and Anthropic are expected to deploy up to 1 million TPUs in the coming years. Reports also indicate that Meta may begin using Google TPUs as early as 2027.

Whether Alphabet can reclaim GPU share from NVIDIA remains to be seen. But the shift is real—and it supports CEO Hock Tan’s long-term goal of growing Broadcom toward $120B in annual revenue.

And Alphabet isn’t the only strategic partner.

Microsoft is reportedly in discussions with Broadcom on next-gen custom silicon—illustrating how Broadcom’s ASIC design capabilities are gaining traction. Meanwhile, Amazon’s in-house Trainium and Inferentia chips show it too is investing in custom AI compute for tighter workload fit and lower cost.

Broadcom also recently signed a direct partnership with OpenAI to co-develop and deliver next-gen AI accelerators across a massive 10GW build. The deal includes both compute and networking components packaged at the rack level.

Seeking Alpha analyst estimates these contracts could ultimately generate over $1000 billion in cumulative revenue.

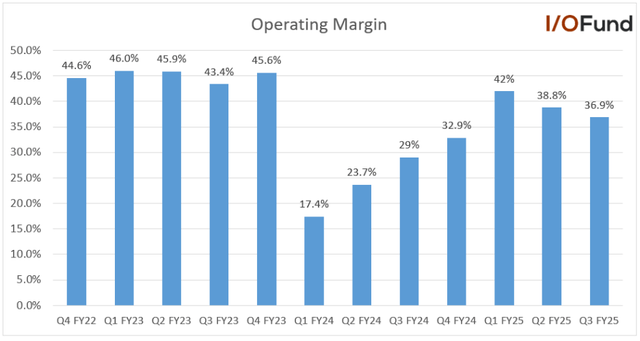

Faster Revenue, Weaker Margins?

Despite the bullish demand drivers, there’s one thing Broadcom hasn’t escaped: margin pressure.

In Q3, gross margins declined slightly—driven by a shift in product mix toward lower-margin AI accelerators (XPUs) and wireless components, as well as continued softness in non-AI semiconductors.

This makes sense. XPUs are designed to be cheaper alternatives to high-margin, general-purpose GPUs. For hyperscalers, they lower total compute cost (TCO), including chips, energy, and data center footprint. For providers like Broadcom, that means thinner per-unit pricing and less scope for premium margins.

Still, Broadcom appears willing to trade individual gross margin for multi-year volume visibility—especially across complex custom contracts. In doing so, it secures long-term revenues and more predictable cash flow at scale.

That said, infrastructure costs are rising. Expansion of the XPU product line involves advanced packaging, leading-edge process nodes, and network stack integration. Operating margins may continue to compress in Q4 on a year-on-year basis.

Management has acknowledged these near-term pressures but maintains that margins should begin to stabilize once product mix normalizes.

Competition Isn’t Idle—But the Market Favors the Leader

Broadcom currently controls roughly 70% of the custom AI ASIC market.

Its closest challenger, Marvell, recently reported a Q3 in line with expectations—highlighting 36.8% YoY revenue growth and reiterating a $10B FY target. Management expects custom and interconnect business momentum to carry through 2028.

Still, not everyone is convinced. Deutsche Bank’s Ross Seymore questioned Marvell’s ability to sustain that growth trajectory. Meanwhile, a recent report from The Information suggests Microsoft is in talks with Broadcom for future custom chip designs—potentially replacing its partnership with Marvell altogether.

That would represent a notable loss for Marvell—and a quiet vote of confidence for Broadcom.

To be clear, none of this means Broadcom is immune to risk. As a semiconductor company, it remains vulnerable to cyclical swings in volume and ASPs. The company’s software and networking revenue segments help mitigate volatility, but future cycles may behave differently from past ones.

There’s also key supply chain exposure. Broadcom depends heavily on TSMC for fabrication, and any capacity constraints or advanced-node delays could clip its ability to meet hyperscaler demand—especially in light of orders tied to OpenAI, Google, and more.

Valuation

According to Seeking Alpha, AVGO trades at ~94x forward earnings—well above its historical range and even above NVIDIA. A lot of good news is priced in.

But if revenue keeps compounding across the next 6–8 quarters, valuation could normalize as P/E multiple gradually compresses back into a sustainable range.

Where does that leave investors?

Broadcom has beaten EPS for 16 straight quarters and outpaced revenue expectations in 15 of them. But the bar is getting higher. Even an in-line report might trigger a “sell-the-news” reaction.

Since April, AVGO is up more than 160%. In the three weeks following the public rollout of Google’s TPU progress, the stock added +16%.

Against that backdrop, Broadcom isn’t cheap. But if you already own it, holding may still be the prudent bet.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.