Tesla Q3 Earnings Report: How Far Is the Stock Price from Cathie Wood's $4000 Target?

Q3 Performance Review

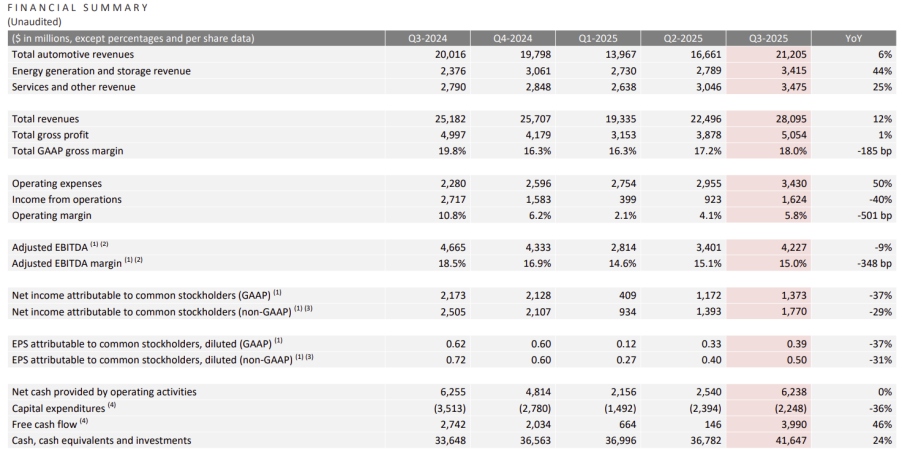

Revenue Exceeds Expectations, Earnings Fall Short

TradingKey - In Q3 2025, Tesla reported revenue of $28.1 billion, a 12% year-over-year increase, surpassing Wall Street expectations and setting a new company record. This growth was primarily driven by record vehicle deliveries, fueled by the launch of standard Model 3 and Model Y and a surge in purchases ahead of expiring tax credits. Additionally, the energy and services segments performed strongly, with revenues rising 44% and 25% year-over-year, respectively. However, adjusted earnings per share came in at $0.50, down 31% from the previous year and below market expectations, largely due to rising operating expenses, reduced regulatory credit income and higher tax rates.

Source: Tesla

Strong Operations Overshadowed by Profit Pressures, Stock Tumbles After Hours

Tesla’s operational performance in Q3 2025 was impressive, showcasing robust production and delivery capabilities. The company achieved record-breaking figures with 497,099 vehicle deliveries and 12.5 GWh of energy storage deployments, while gross margins improved to 18%, driven by strong growth in the energy and services segments. However, these operational successes did not translate into profit growth. Operating income fell 40% year-over-year to $1.6 billion, with the operating margin dropping 501 basis points to 5.8%. Key factors contributing to this include:

· Surging Operating Expenses: Operating expenses soared 50% to $3.4 billion, driven by $238 million in restructuring costs for new model production lines, significant R&D investments in AI projects (including the new AI5 chip), and a notable increase in selling, general, and administrative (SG&A) expenses.

· Tariff Headwinds: Tesla faced over $400 million in tariff costs across its automotive and energy businesses, significantly compressing overall profitability.

· Pressure on Automotive Margins: Excluding regulatory credits, automotive gross margins were only 15%, below market expectations and a key driver of the post-earnings stock price decline. The margin contraction stemmed from a year-over-year drop in one-time Full Self-Driving (FSD) revenue, rising tariff costs, and higher per-vehicle costs due to reduced fixed-cost absorption. Looking ahead, the absence of tax credit support and increasing production capacity may continue to pressure automotive margins in the coming quarters.

Robust Cash Flow Fuels Future Growth

Tesla generated nearly $4 billion in free cash flow this quarter, far exceeding analyst expectations of $1.25 billion, underscoring the strength of its core business despite margin pressures. This contributed to a $4.9 billion increase in cash and investments, bringing the total to $41.6 billion by quarter’s end. This substantial cash reserve provides Tesla with a strong financial foundation, enabling it to pursue capital-intensive AI strategies without heavily relying on capital markets.

-6317427f20514e6d8cbda00e3c55c4a3.jpg)

Source: Tesla

Is Tesla’s Stock Price Far from $4,000?

While Tesla’s automotive business remains its core pillar, its significance is gradually diminishing. The company’s 260x price-to-earnings (P/E) ratio is difficult to justify with traditional car manufacturing alone. Clearly, Elon Musk is steering market focus away from conventional automotive products toward an AI-driven software and services ecosystem. In the Q3 earnings call, discussions centered almost entirely on Full Self-Driving (FSD), Robotaxi, and Optimus robots, positioned as the company’s future growth drivers, with no mention of updates to existing models or new consumer vehicles.

Instead, Tesla is concentrating all efforts on a vertically integrated AI ecosystem encompassing autonomous driving, robotics, hardware, and energy, each representing trillion-dollar market opportunities:

· Cybercab: Scheduled for mass production in Q2 2026, Cybercab marks a significant shift in Tesla’s business model—from selling cars to consumers to operating a high-margin autonomous transportation network. Its value will be unlocked and enhanced through continuous AI software upgrades rather than traditional vehicle design refreshes.

· Optimus Humanoid Robot: Musk described Optimus as potentially “the greatest product ever,” unveiling a clear development roadmap: a V3 prototype in Q1 2026, with production scaling to millions of units annually by year-end. Complex hand design and manufacturing remain the primary technical and R&D focus.

· AI5 Chip: Management detailed the upcoming AI5 chip, which will offer 40x the performance of AI4. Through deep partnerships with Samsung and TSMC, Tesla will ensure the AI5 chip meets its needs for vehicles, robots, and data centers, establishing a platform-level efficiency advantage.

· Energy Business Synergies: Record energy business performance is increasingly aligning with Tesla’s AI strategy. The Megapack storage system not only serves grid storage but is now expanding to power AI data centers. The upcoming Megapack 4 will integrate substation components, streamlining deployment and boosting efficiency.

Tesla’s Next Steps

Tesla’s record deliveries in Q3 should have driven robust profit growth through economies of scale, yet operating income fell 40% year-over-year. The root cause lies in Tesla’s strategic shift, redirecting capital from its mature, high-margin automotive business to high-risk, high-reward AI initiatives. This indicates a deliberate sacrifice of short-term automotive profitability to fund the transformation into an AI-driven company. The automotive business now serves as a “cash cow,” providing financial support for the growth of AI, software, and autonomous vehicle fleets.

Tesla’s current stock price is over 800% below the $4,000 target. While the market is enthusiastic about Tesla’s AI vision, its lofty valuation and short-term profit pressures may lead to near-term stock price volatility. Long-term, successful commercialization of autonomous driving, Optimus, and other projects could undoubtedly propel Tesla’s market value higher.

Risk -- Musk Staying or Leaving

Tesla plans to discuss a $1 trillion, 10-year compensation package for Elon Musk at its shareholder meeting on November 6, 2025. The equity awards will vest only upon achieving milestones such as an $8.5 trillion market cap, 20 million annual vehicle deliveries, 1 million Robotaxi deployments, and $400 billion in core earnings. The package aims to secure Musk’s leadership for Tesla’s AI and autonomous driving transformation.

If not approved, uncertainty about Musk’s commitment could arise, potentially diverting his focus to xAI or SpaceX and weakening Tesla’s AI strategy execution. Additionally, opposition from proxy advisors ISS and Glass Lewis, as well as institutional investors like the New York State Pension Fund, could create shareholder divisions, undermine board authority, and heighten short-term stock volatility.

-6db47ded27a54057a172766785c04003.jpg)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.