Tesla Q3 Earnings Preview: Record Deliveries “Burn Out,” Growth Path Filled With Uncertainty

TradingKey - Riding on improved market sentiment and Elon Musk’s renewed focus on his role as Tesla CEO, Tesla’s stock has rebounded over 85% in the past six months — the strongest recovery among the Magnificent Seven. Tesla is set to report its Q3 2025 earnings after market close on October 22, and while record-breaking delivery numbers may impress, Wall Street remains cautious about its strategic pivot toward AI, robotics, and autonomous driving.

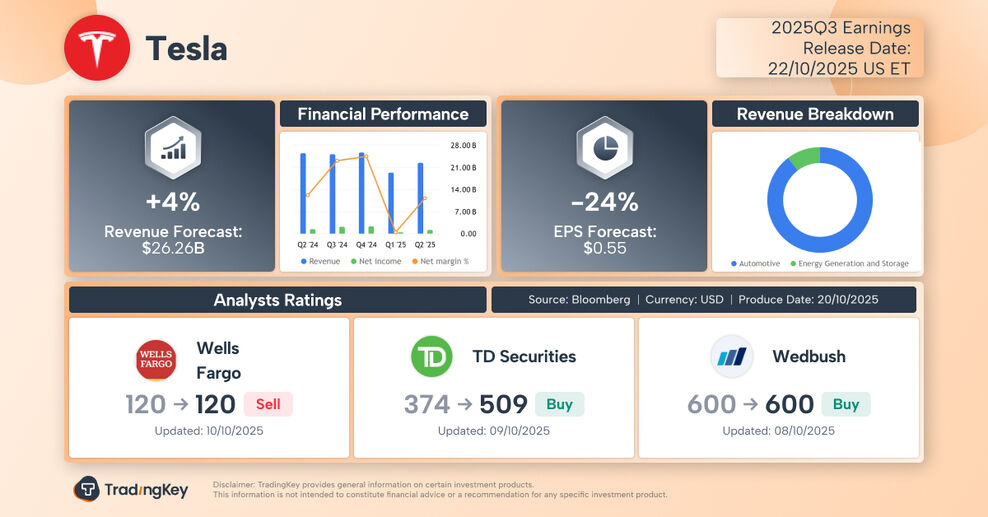

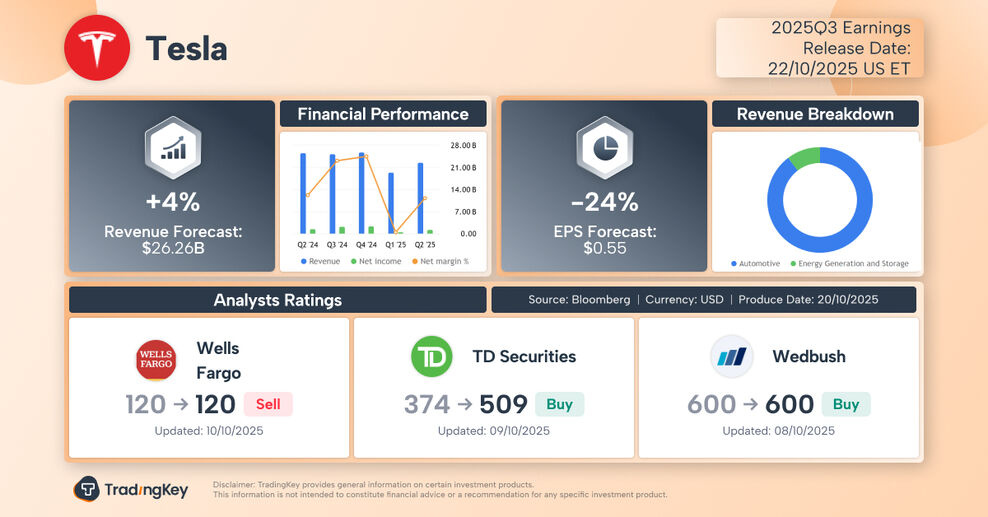

According to Bloomberg data, analysts expect:

- Revenue: $26.26 billion, up 4% YoY

- Net Profit: $1.89 billion, down 24% YoY

Compared to the previous quarter — when both revenue and EPS declined — Q3 appears to be a case of “growing sales but shrinking profits.” But is this financial trend truly cause for celebration?

The revenue increase was primarily driven by:

- A pre-deadline buying surge ahead of the expiration of U.S. federal EV tax credits

- Strong sales from new models in China

Yet Tesla faces mounting challenges ahead, including an aging product lineup, new lower-priced models with significantly reduced features, and weakening overall auto demand — all of which point to a difficult road ahead for vehicle growth.

Tesla is strategically shifting its business focus toward AI, robotics, and autonomous driving. While many institutions see potential in this transformation, the consensus analyst target price reflects caution about these highly uncertain drivers.

Investors will be watching closely for answers on key questions in the upcoming earnings report and guidance:

- Has the record Q3 delivery number already peaked?

- Are there tangible updates on Robotaxi services and related vehicles?

- When will the humanoid robot Optimus begin mass production and large-scale deployment?

- Will Musk’s proposed $1 trillion compensation package be approved — and can it motivate him to deliver on ambitious targets?

Record Deliveries — But Not Sustainable

In early October, Tesla reported record Q3 deliveries of 497,099 vehicles, up 7.4% year-over-year — far exceeding the expected 439,600 units.

Surprisingly, the stock fell over 5% that day, as investors recognized that much of the surge was driven by last-minute purchases before the EV tax credit expires — a temporary boost unlikely to repeat.

This dynamic is reflected in analysts’ outlooks for the quarter.

Beyond the expiring incentives, factors like geopolitical tensions, tariffs, and inflation have disrupted the U.S. auto industry. While tariff impacts have proven less severe than feared, consumer resilience is showing cracks.

Industry forecasts suggest Tesla may see lower deliveries in Q4. Three months ago, Musk warned that Tesla would face a few tough quarters as EV subsidies disappear.

Tesla’s Push Against Weakness

To counter softening demand, Tesla recently launched new versions of the Model Y and Model 3, priced $5,000 lower than previous models. The company is also expected to ramp up promotions to boost sales.

But in the view of Bloomberg columnist Liam Denning, these cheaper Teslas represent a flawed cost-cutting strategy. The stripped-down models — with shorter range, fewer speakers and manual steering adjustments — may not be enough to revive volume growth.

“The models — or rather, trims, since they aren’t new vehicles — unveiled Tuesday are about taking away, not adding. They reek of a company holding the line, not moving it forward,” Denning wrote.

Additionally, as highlighted in both Q2 results and Q3 expectations, Tesla’s profitability faces intense pressure. Shareholder Mahoney noted that the end of incentives will leave a demand gap in the U.S. during Q4, while price cuts and promotions will further squeeze margins.

Beyond the erosion from price wars, Musk is using car sales as a “cash engine” to fund investments in autonomous driving and robotics.

Can Tesla’s Transformation Succeed?

In July, Musk said that if Tesla succeeds in humanoid robots (Optimus) and self-driving technology, the company could be worth $25–30 trillion. In September, he added that Optimus alone could account for 80% of Tesla’s future value.

Tesla stated in Q3 that it is scaling up human-sized robot production, aiming to unveil the third-generation Optimus by year-end, with mass production starting in 2026. Musk projects 1 million units per year by 2030.

Longtime Tesla bull Dan Ives, Wedbush analyst, recently reiterated his “outperform” rating and $600 price target, emphasizing that Tesla’s future story centers on an AI-led transformation driven by autonomy and robotics.

Ives argued that under President Trump’s administration, regulatory barriers for Tesla

will accelerate, speeding up core projects like Full Self-Driving (FSD), potentially adding at least $1 trillion in market cap by next year.

Stifel also sees strong potential in Tesla’s autonomy push, expecting unsupervised full self-driving to launch in the U.S. by year-end.

Deutsche Bank noted that Musk’s clear focus on Tesla’s most critical initiatives — Robotaxi and Optimus — combined with the board’s compensation plan, removes major overhangs. The firm believes Tesla stands to benefit from leadership in embodied AI.

Where Is Tesla Stock Headed?

According to TipRanks, in the past eight quarters, Tesla has beaten EPS estimates only twice. After earnings, the stock has been equally likely to rise or fall on the first trading day.

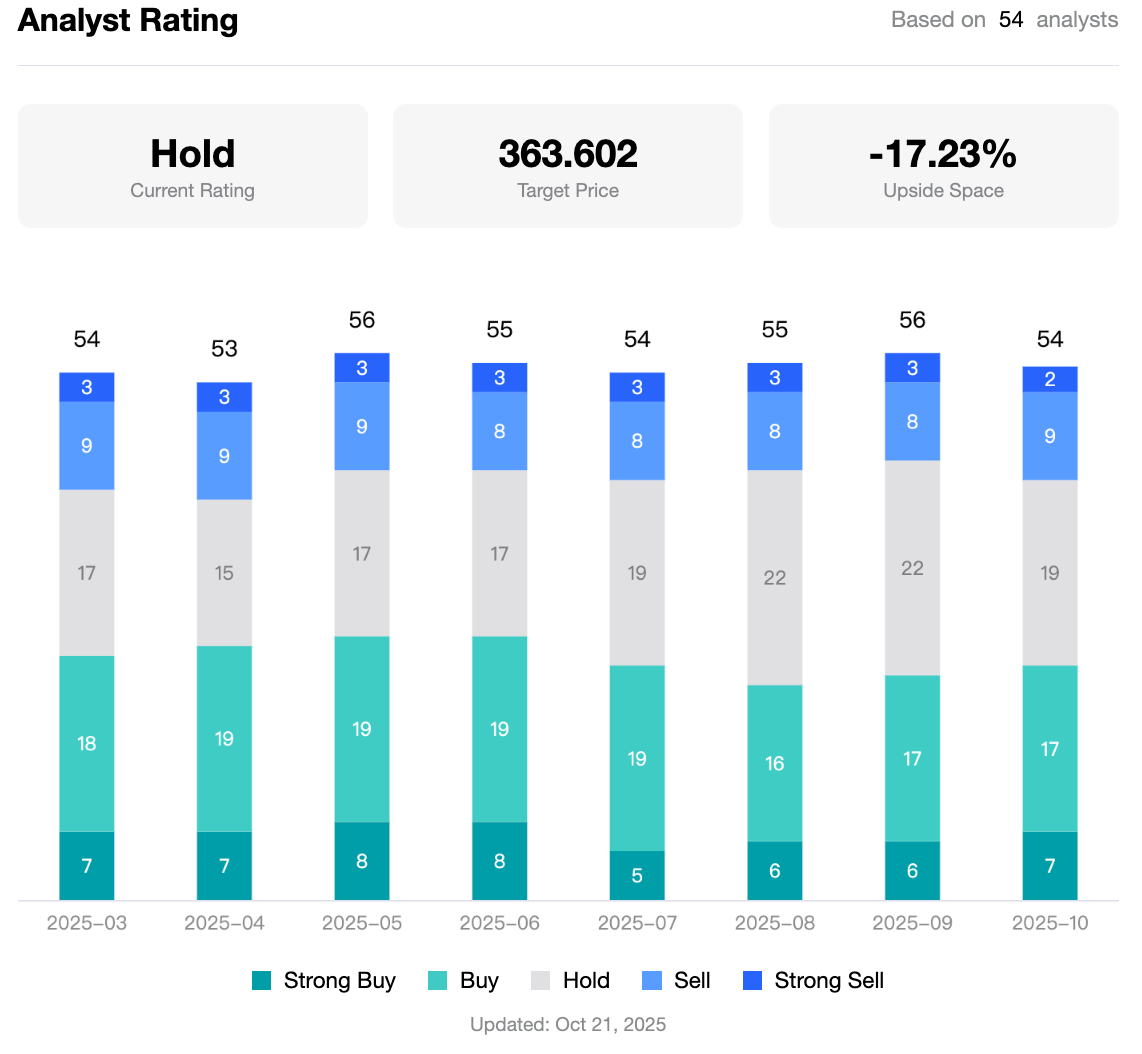

Per TradingKey, the analyst consensus target price for Tesla is $363.60 — about 17% below current levels — reflecting broad analyst caution.

Analyst Price Targets for Tesla Stock, Source: TradingKey

Morningstar argues that the market is overly optimistic about Tesla’s Robotaxi prospects, with much of the upside already priced in. It rates Tesla’s stock as overvalued based on earnings potential.

The firm assigns Tesla a "Very High Uncertainty" rating, citing risks such as:

- Cyclical auto demand collapse

- Intensifying competition

- Margin erosion from price cuts

- Uncertain returns on massive investments in FSD software and humanoid robots

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.