Lockheed Martin (LMT): Robust Backlog & Geopolitical Tailwinds Bolster Long-Term Outlook Despite Short-Term Project Setbacks

Investment Thesis

TradingKey - The U.S. is increasing defense spending significantly over the years due to rising global tensions and the need to modernize its military capabilities. The defense sector has outperformed broader markets fueled by reliable government contracts and innovation. This report launches our series on national defense stocks, starting with Lockheed Martin (NYSE: LMT), a leader in aerospace and defense.

Why Lockheed Martin?

l Diverse products: F-35 jets, hypersonic weapons, and NASA’s Artemis space program.

l Strong finances: $74 billion revenue expected in 2025, with a $160 billion backlog for stable future income.

l Attractive valuation: Trades at a forward P/E of 15x (below industry average of 20x) due to some cost and supply chain issues.

l Dividend Income: Offers a 3% yield for income.

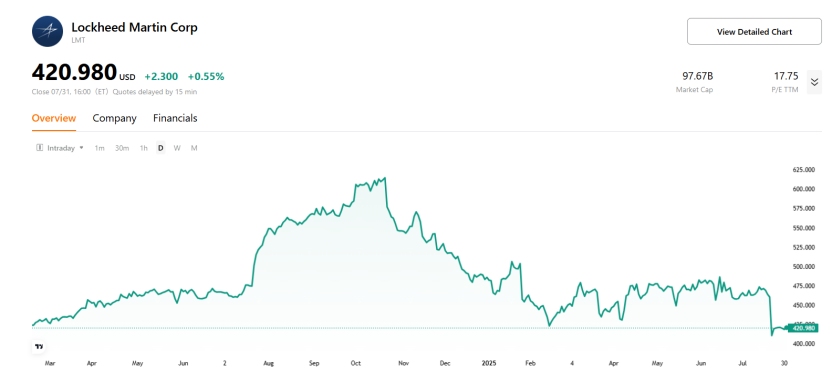

Upside Potential: If Lockheed overcomes operational challenges, its stock could reach $410–$550 per share (based on $27.6 EPS and relative valuations).

Strategy: Invest 3–5% of a portfolio in Lockheed for a 3–5 year horizon to gain defense exposure with growth and income. Watch quarterly earnings and global events to manage risks.

Source: TradingKey

Company Overview

Founded in 1995 through the merger of Lockheed Corporation and Martin Marietta, Lockheed Martin is headquartered in Bethesda, Maryland. The company designs and manufactures advanced defense and aerospace systems, including fighter jets, missile defense systems, and space technologies. Its primary customers include the U.S. Department of Defense (DoD), NASA, and allied international governments such as the UK, Australia, and Canada. Approximately 65% of its revenue is derived from the DoD.

Lockheed Martin's strength lies in securing multi-year DoD contracts and strategic partnerships with NASA and allied governments, ensuring long-term revenue stability. The company focuses on cutting-edge innovation, ranging from hypersonic weapons to AI-integrated defense systems, positions it well to meet evolving global security demands.

Financials — Quarterly Highlights (Q2 FY2025)

Lockheed Martin’s Q2 FY2025 results (ended June 2025) reflected ongoing challenges in a complex geopolitical environment, impacting profitability despite stable revenue.

l Revenue: $18.2 billion in Q2, essentially flat YoY and slightly below expectations of about $18.57 billion, driven by steady F-35 deliveries and missile system sales.

l EPS: $1.46 per share, a significant miss versus consensus near $6.5.

l Gross Margin: Down from 12.9% in Q1 to 4.4%.

l Operating Income: Non-GAAP operating income was roughly $570 million with a margin near 3.1–4.1%, down sharply from last year’s double-digit margins, driven by legacy program charges and cost overruns.

l Net Income: $342 million, down 79% YoY, pressured by program-related losses.

l Share Repurchases: About $1.3 billion returned through dividends and buybacks, reflecting confidence despite profit pressures.

l Cash Flow: Operating cash flow was $201 million, sharply down from $1.9 billion in Q2 2024. Free cash flow was negative $150 million compared to positive $1.5 billion a year earlier.

l Tax Risks: The company is facing a significant tax dispute with the U.S. Internal Revenue Service (IRS), which is seeking approximately $4.6 billion in additional income taxes. While not fully impacting the quarter’s reported results, this ongoing matter introduces substantial financial uncertainty and potential future cash outflows.

Lockheed Martin’s Q2 earnings were much lower than expected because the company faced about $1.6 billion in extra costs from certain projects that went over budget and other one-time expenses. These unexpected costs caused profits and earnings per share to fall sharply. As a result, investors became worried, and the stock price dropped around 10% soon after the earnings report. Even though sales stayed steady, profits and cash flow both took a big hit because the company struggled with managing costs and some older projects had problems, all while dealing with supply chain delays.

Q3 Guidance and Outlook:

Lockheed Martin’s forecast for the next quarter is a bit lower due to ongoing supply chain problems, especially shortages of small electronic parts used in missile systems. The company expects these supply issues to improve by the end of the year as suppliers catch up. Their strong backlog of orders, valued at around $166.5 billion, gives confidence that revenue will remain stable through 2028 and support long-term growth.

.jpg)

Source: Lockheed Martin

Revenue Breakdown (Q2 FY2025)

.jpg)

Source: Lockheed Martin, TradingKey

Aeronautics ($7.42 billion, 41%): The largest segment, producing the F-35 Lightning II, legacy fighters like the F-16, and transport aircraft including the C-130 Hercules. Revenue grew by about 2% YoY, supported by 14 F-35 deliveries in the quarter and ongoing sustainment contracts. The F-35 program remains key to Lockheed Martin’s growth, with management expecting to deliver between 170 and 190 F-35 aircraft in 2025. The segment backlog stands at around $52 billion. The segment reported an operating loss driven mainly by a $950 million charge related to a classified program.

Missiles and Fire Control ($3.43 billion, 19%): Focuses on precision weapons including Javelin missiles, PAC-3, and hypersonic systems. Sales rose approximately 11% YoY due to strong demand for tactical missiles amid global conflicts. Operating profit grew to about $479 million. The backlog for this segment is approximately $40 billion.

Rotary and Mission Systems ($3.99 billion, 22%): Encompasses helicopters (Sikorsky), radar, and cybersecurity solutions. Revenue declined by about 12% YoY, impacted by significant losses related to specific helicopter programs, notably a $570 million charge on the CMHP (Common Multi-Role Helicopter Program) and a $95 million charge on the TUHP (Tiltrotor Utility Helicopter Program). These program losses led the segment to report an operating loss of approximately $172 million for the quarter. Despite these setbacks, the segment maintains a robust backlog of approximately $38.6 billion, reflecting ongoing demand across its diverse product lines.

Space ($3.31 billion, 18%): Supports satellite systems, the Artemis lunar program, missile defense, and classified space projects. Revenue increased around 4% year-over-year, with operating profit improving by 5%. The segment’s backlog is approximately $35.5 billion.

.jpg)

Source: Lockheed Martin, TradingKey

Growth Potential

Lockheed Martin is positioned for strong growth driven by key global defense trends and strategic priorities. Rising geopolitical instability across Europe, Asia, and the Middle East is fueling a surge in worldwide military spending, with SIPRI projecting global defense expenditures to approach $2.5 trillion by 2030. Lockheed leverages this environment as the largest U.S. defense contractor, securing nearly 10% of the $849 billion U.S. Department of Defense budget for 2025, anchoring a core base of high-value, steady business. Central to its growth is the F-35 program, with over 1,000 jets delivered and plans for up to 2,500 more, ensuring stable production and a lucrative stream of high-margin sustainment contracts through 2040.

Lockheed is also expanding in rapidly growing sectors such as space and hypersonics. The company plays a vital role in NASA’s Artemis lunar program and leads in hypersonic weapon development, including the ARRW system. The space market alone is forecasted to grow by 7% annually through 2030, representing a significant opportunity. Its record backlog, exceeding $166 billion and covering more than two years of revenue, provides unmatched earnings visibility and reflects strong demand across all segments, especially from NATO and Indo-Pacific allies.

Strategically, Lockheed’s investments in advanced technologies like AI-enabled autonomy, next-generation drones, cyber solutions, and energy-efficient satellites align well with evolving U.S. and allied defense priorities. The company’s broad global footprint, new advanced manufacturing facilities in Alabama and Texas, and efforts to localize supply chains strengthen resilience to market shifts and operational disruptions.

Competitor Analysis

Lockheed Martin leads the U.S. defense sector with an estimated 14% market share, competing with companies like Boeing, Raytheon Technologies, Northrop Grumman, and General Dynamics.

(1).jpg)

Source: As of Q2 2025, Mordor Intelligence, ResearchAndMarkets, StockAnalysis, TradingKey

Valuation

Lockheed Martin currently trades at a forward P/E of about 15x, below peer. This discount reflects recent execution setbacks such as program cost overruns and supply chain disruptions that have weighed on investor sentiment. We assign 15-20x multiple to Lockheed Martin. 15x multiple captures this cautious market view, accounting for near-term risks and uncertainties. However, Lockheed’s strong backlog, stable market share, and consistent revenue growth provide solid earnings visibility, while its 3% dividend yield adds appeal for income investors. The 20x peer average represents more stable, higher-growth defense firms with fewer execution risks, like Raytheon and Northrop, and serves as an achievable valuation if Lockheed addresses current challenges. Based on a forward EPS of 27.6 for FY2025, this implies a target price range between $410 and $550 per share.

Risks

Investing in Lockheed Martin comes with challenges:

l Supply Chain Delays: Shortages in semiconductors and skilled labor may delay production of critical programs like the F-35 and missile systems, impacting revenue and margins.

l Geopolitical Shifts: Although unlikely before 2030, any reduction in global tensions or defense budgets could lead to decreased defense spending and fewer orders.

l Competition: Rivals such as Raytheon and Boeing are heavily investing in hypersonics and AI, which could erode Lockheed’s traditional technological lead. Boeing’s recent win of the 6th-generation fighter (F-47) contract exemplifies intensifying competition.

l Cost Management: Under fixed-price contracts, cost overruns, particularly on programs like the F-35, could pressure profitability if not effectively controlled.

l Regulatory Risks: Changes in U.S. export controls or trade policies could restrict Lockheed’s international sales and supply chains.

l Technological Obsolescence: The increasing emphasis by the U.S. Defense Department on AI-enabled, integrated technologies means traditional defense platforms risk becoming outdated unless Lockheed adapts successfully.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.