Meta 2Q25 Earnings Comment: We are yet to See the Effects of the Hiring Bonanza

Meta 2Q25 Earnings Comment

TradingKey -Meta released its earnings for the second quarter of the fiscal 2025 on July 30th after the market closed.

- 2Q25 Earnings per share: $7.14 vs $5.87 estimate (+38% y/y)

- 2Q25 Revenue: $47.52 vs $44.78bn estimate (+22% y/y)

Meta not just delivered, they over-delivered with earnings, and this can be explained with several key factors:

First things first, traffic remains strong with better-than-expected daily active people – 3.48 billion across all the platforms (vs previously expected 3.45 billion). Despite the mature stage of user penetration, we can still see people getting onboard into the Meta’s apps. Additionally, the company started testing ads on Threads, but the process will be rather gradual so they can further acquire more users before a full-scale monetization takes place

The 22% revenue growth can also be explained with the 11% increase in ad impressions, and this can be attributed to the strong AI-based ad targeting and optimization.

On the cost side, the progress is also quite remarkable as this helped expand margins once again – 43% operating profit margin vs 38% in 2Q2024.

What was surprising is the fact that they did not significantly revise the capex estimate (just the lower end of the estimate went from $64 billion to $66 billion). This, to some extent, can be seen as an answer to the criticisms about Meta’s excessive spending.

However, despite the very solid earnings, the exciting part for Meta has not even started yet. We are yet to see the effect of the recent mega hirings both in terms of contribution to the company’s AI capabilities and the reflection on the financial statements.

Even with 11% surge in the price pre-market, Meta is still cheap at around 30x PE.

Meta 2Q25 Earnings Preview

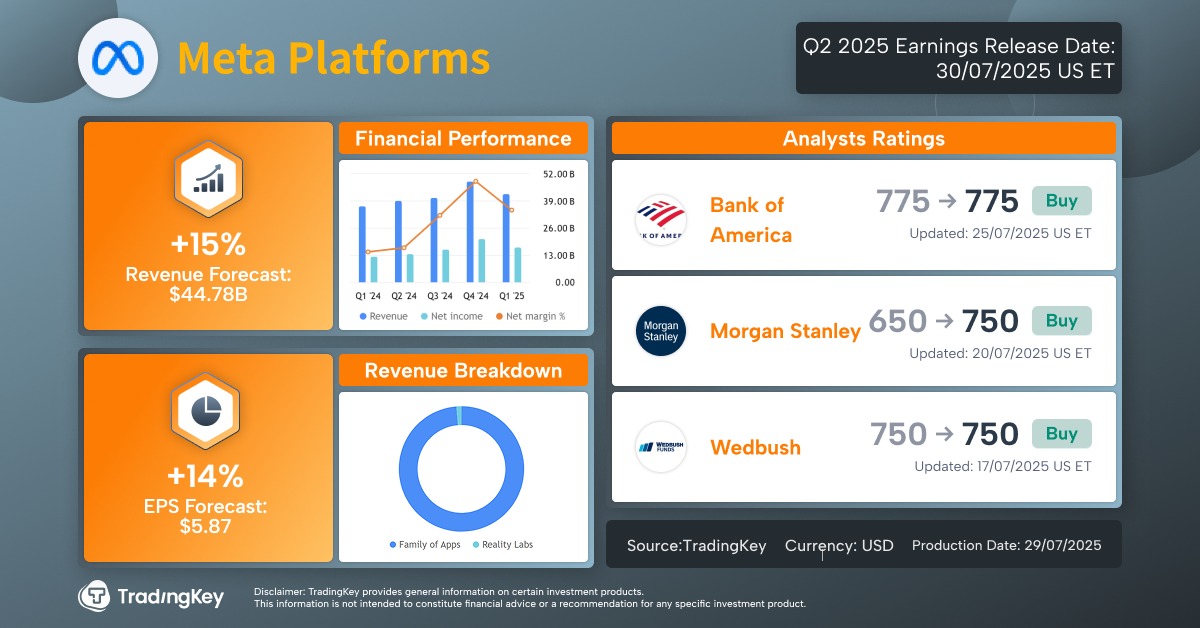

TradingKey -Meta will release its earnings for the second quarter of the fiscal 2025 on July 30th after the market closes:

- 2Q25 Earnings per share: $5.87 estimate vs. 2Q24 actual of $5.16 (+14% y/y)

- 2Q25 Revenue: $44.78bn estimate vs. 2Q24 actual of $39.07bn (+15% y/y)

Advertising business:

Before we get into AI, we should talk about Meta’s cash cow – the advertising business. Meta is the second largest advertising platform, just after Alphabet. The parent of Google already has reported revenue growth above expectations, making people feel upbeat about Meta as well. This will largely depend on the number of active users across all platforms for Meta – a number already quite mature and growing at just low-single digit. The main growth driver for the ad business will be how well the company is implementing its AI tools into its advertising products. Another area that we would look into is how and when the growing platforms like WhatsApp and Threads are going to monetize.

AI efforts:

As one of the major scalers, AI is already a centerpiece of the company’s future. First thing, people will ask about Meta is the capital spending. We already saw Alphabet revising upwards its estimates for capex for the year, and we don’t expect things to be different here. For reference, the current guidance stands at $64-72 billion, primarily going towards AI infrastructure.

Another aspect that Meta has been quite notable recently is the massive hiring of top-notch AI talent. During the earnings call, Zuckerberg will probably disclose more on where the company is currently standing with the hiring process. Cannot deny that, as of now, there is no consensus agreement on whether this hiring spree will be able deliver the desired result.

Finally, the company’s LLM model will also be in the spotlight, as investors are eager to see more concrete steps on cutting the gap between Meta’s Llama and the leaders – OpenAI and Grok.

Conclusion

Meta currently trades at just 27x PE as its current state of ad business is solid. However, investors want to see whether the large spending on both infrastructure and talent actually moves the needle for the AI initiatives.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.